Digital Accounting Innovation and Its Relationship with Perceived ESG Performance and Reporting Transparency: Evidence from the Financial Services Sector of the UK

PDF

PDF

1College of Business Administration, Imam Abdulrahman Bin Faisal University, Dammam, Saudi Arabia

Received: 27 November, 2025

Accepted: 25 April, 2026

Revised: 20 April, 2026

Published: 04 June, 2026

ABSTRACT:

Introduction: The study examined the role of digital accounting innovation and its association with Perceived ESG Performance and reporting transparency in the UK financial services sector.

Methods: The survey was carried out from a sample of 300 professionals who were the representatives of UK financial services firms. The collected data were analyzed using Partial Least Squares Structural Equation Modeling (PLS-SEM) on SmartPLS.

Results: Digital Accounting Innovation was found to be significantly and positively related to Perceived ESG Performance (β = 0.664, p = 0.001). Digital Accounting Innovation was also found to have a statistically and significantly predictive relationship with Reporting Transparency (β = 0.563, and p = 0.001), which indicated that accounting practices driven by technology, such as Blockchain and Machine Learning, substantially contribute towards enhancing disclosure transparency of Perceived ESG Performance within the UK financial services industry.

Conclusion: These findings offer practical insights for industry practitioners aimed at strengthening ESG reporting practices by means of digital accounting systems. The findings imply that digital accounting tools may provide enhanced transparency and consistent ESG disclosures in retort to regulatory and investor expectations.

Keywords: Digital innovation, accounting, ESG reporting transparency, Blockchain, machine learning, financial services sector.

1. INTRODUCTION

The digital accounting innovations, such as AI-based analytics, blockchain, and cloud account reporting systems, are changing the way financial information is collected, verified, and presented in digital form (Vărzaru, 2022). Accordingly, digital accounting innovation should be interpreted as part of a wider enterprise automation capability in which analytics, cloud systems, and platform integration improve information flows, managerial responsiveness, and strategic value creation across service organisations (Vărzaru, 2022; Kanaparthi, 2024; Nair et al., 2025; Wang & Wang, 2025; Patel & Patyrykin, 2025). The creation of regulatory frameworks in the UK, including the introduction of the Sustainability Disclosure Requirements (SDR), the use of ISSB standards (IFRS S1/S2), and more rigorous anti-greenwashing policies demand companies to incorporate ESG measures into their formal financial reporting systems (FCA, 2023; Ketterling and Germany, 2025). Internationally, assets focused on ESG have increased to USD 35 trillion in 2023, with the sustainable finance market of the UK boosted by Green Gilts, green pensions, and Special Drawing Rights (SDRs) reforms, which remain important in the leadership of the UK in sustainable accounting (Government of the UK, 2023). For instance, in the case of the UK, financial services firms encounter major issues that are comprised of regulatory complexity, data fragmentation, and legal systems that are incompatible with contemporary frameworks of ESG (Norton Rose Fulbright, 2022). (FCA, 2023) estimates that compliance with novel SDR and FCA labeling regulations costs almost £205 million in the first year to the UK’s financial services firms. On the other hand, another survey carried out by the Bank of (England, 2024) signified that 58% of financial companies in the UK are implementing digital accounting tools to enhance perceived ESG Performance; however, almost 45% still struggle with comparability as well as standardization (Ediagbonya & Tioluwani, 2023). This, together with the increase in compliance cost in the face of the SDR and assurance requirements pose a risk of non-uniform reporting and non-substantive compliance instead of substantive ESG integration, as implied by (Annakleinman, 2025). This concern is consistent with ESG-rating and financial-sector accountability debates showing that disclosure-centred systems can become symbolic when greenwashing risks, indirect emissions, and substantive environmental accountability gaps are not addressed (Patyrykin & Vasyukova, 2025).

In this perspective, current industry and academic literature accept the effectiveness of digitally AI-enabled accounting for predictive ESG insights. Nevertheless, the available literature lacks empirical findings regarding the relationship between digital accounting innovations and perceived ESG Performance and reporting transparency in a highly regulated financial services setting, especially in the UK setting. Therefore, this research targets the UK financial services sector to examine how the adoption of digital accounting innovation is related to perceived ESG Performance and reporting transparency. The findings of the study are significant for accounting professionals, including auditors, finance, and reporting managers, to refine their strategies to adopt digital accounting systems, improve perceived ESG Performance, disclosure quality, and transparency to comply with SDR and IAASB regulatory requirements.

This study holds three specific contributions. Empirically, it provides the evidence specific to the UK financial services sector on the relationship between digital accounting innovation and ESG-related outcomes. In theory, it combines digital accounting practices with ESG reporting using operationalized digital innovation as a quantifiable construct that is associated with the quality of disclosure. As a policy measure, the results provide policy implications to regulators and practitioners on how digital systems can be used to assist more reliable and transparent ESG reporting in the context of the changing UK regulatory frameworks.

The study is based on different and interconnected segments. For instance, in the introduction, the problem of the research, context, and objectives are described. The second section outlines the theoretical framework, which involves the combination of the appropriate perspectives that inform the study. A critical literature review analyses existing literature on the topic, identifies research gaps, and develops hypotheses, followed by a conceptual framework of the study. The methods section carries details about the research design, sampling method, data collection, and the methods of analysis are discussed in the methodology section. The findings of the empirical results are presented in the results section through PLS-SEM analysis. The findings are then discussed in terms of the previous literature and the UK financial services environment. Lastly, in the paper, the conclusion consists of major implications, limitations, and future research directions.

2. LITERATURE REVIEW

2.1. Theoretical Framework

The theoretical framework of the study is based on the Institutional Theory and the Technology-Organization-Environment (TOE) framework, but instead of their operationalization as quantifiable constructs, they were used as the perspectives for providing explanations to the relationship between digital accounting innovation and ESG-related outcomes. This is a significant difference, because the analysis is concerned with the results of relationships between outcomes, and not the direct modeling of determinants of adoption.

The reason why firms in the UK financial services sector are adopting digital accounting innovation in increasing numbers is explained by the Institutional Theory. According to (Hossain et al., 2025), organizations react to the coercive, normative, and mimetic pressures, which are the results of the regulatory bodies, industry standards, and the expectations of stakeholders. The UK context has frameworks like Sustainability Disclosure Requirements (SDR), IFRS 1/2 under the ISSB, and anti-greenwashing regulations that have expectations of sound, auditable, and similar ESG disclosures (Kumar et al., 2024). These institutional pressures are not the direct determinants of perceived ESG Performance or transparency but influence motivation and work direction of digital accounting adoption, which is reflected in this study in the construct of digital accounting innovation.

To complement this, the TOE framework describes the reason behind difference in the effectiveness of such innovation in different firms. As discussed by (Zhang & Wang, 2024; and Li et al., 2025), the digital system implementation is also affected by technological readiness, organizational capabilities, and environmental conditions. Practically, AI analytics, blockchain, and cloud platforms are only useful in the improvement of ESG reporting with adequate infrastructure, integration capacity, and human resources. Although these dimensions of TOE are not directly modeled, they provide a background to explain the differences in the relationship strengths seen in the analysis. Based on that, the conceptual model places the digital accounting innovation as the most important explanatory variable of the linkage between institutional pressures and organizational conditions, and perceived ESG Performance and reporting transparency. In this manner, there is a guarantee of theoretical consistency as well as consistency between the empirical design of the study and its analytical focus. However, TOE and Institutional Theory are used as boundary conditions to interpret relationships rather than model predictors.

Study Constructs

Digital Accounting Innovation (DAI) is a term used to describe the adoption and application of digital technologies, including AI-based analytics, blockchain, and cloud-based systems, to improve accounting operations (Huyen, 2024). It entails the application of technology to standardize, automate, and integrate ESG-related financial information, which is accurate, auditable, and traceable. Corporate Perceived ESG Performance assesses the perceived performance of organizational ESG based on (Jin & Kim, 2022), which is performance in the environment, social, and governance through accounting reports as realized and presented. As mentioned in (Wang & Yang, 2024), Reporting Transparency (RT) is the understandability and fullness of ESG communications that digital accounting practices make possible, which include real-time reporting, data integrity, comparability, and internal controls and controls that help stakeholders to have confidence.

2.3. Literature Review

An emerging literature is analyzing the relationship between digital accounting systems and perceived ESG Performance, though the evidence still seems context-specific and somewhat methodology-dispersed. (Li & Pang, 2023) reveal statistically significant evidence of Chinese firms showing that digital finance boosts the performance of ESG in the form of green innovation. In a similar vein, (Wu & Li, 2023) also verify this advantageous relationship, although adding the aspect of environmental uncertainty as a mediator, indicating that institutional pressures precondition the results. Although both studies complement Institutional Theory, the emphasis on the outside pressures does not consider the inner organizational preparedness, which restricts the scope of explanation. While (Suhardjo et al., 2024) support institutional arguments but do not include industry-specific information, especially in highly-regulated financial markets.

(Wang & Tang, 2024), on the other hand, extend this discussion by introducing the notions of substantive and symbolic digital innovation and the idea that ESG improvements require a genuine change in the actual technological integration. This is in line with the TOE framework with its focus on technological preparedness and organizational intent. Though due to the measures used to measure them (patent data), their construct validity is undermined as they do not reflect actual accounting processes. In addition, (Nair et al., 2025) provide more conceptual information about AI-enabled accounting based on a systematic review and Delphi, but it is not supported by empirical validation, which would allow drawing causal conclusions. Such methodological variations, which include, but are not limited to, panel regression and qualitative synthesis, are somewhat attributable to these mixed results, and underscore the lack of empirical research at a firm-level and sector-specific levels.

These studies propose that digital accounting innovation can affect perceived ESG Performance through underlying accounting processes, but not direct technological presence. In particular, the digital systems have a positive impact on ESG by improving data integration between departments, allowing audit trails and traceability, improving internal controls, and enhancing the comparability of reporting as well as reporting timeliness. They are the mechanisms that are under-explored empirically, even though they are at the center of the accounting practise. The Institutional Theory describes the external pressure of regulatory bodies and other stakeholders that cause organizations to disclose their environmental impacts, and the TOE framework explains how organizational and technological preparedness facilitates the process. When combined, it provides a logical account of why comparable technologies can act differently in terms of ESG results.

Hence, despite a general agreement on a positive relationship between digital innovation and perceived ESG Performance in previous research, the existing research has not synthesized accounting mechanisms and theory to the specific requirements of the sector. More specifically, it lacks empirical evidence with respect to controlled environments like the UK financial services industry, where the ESG reporting requirements are high. This gap drives the worth investigating the way digital accounting innovation can be translated into quantifiable Perceived ESG Performance enhancement in such a context. Therefore, these literature arguments lead to the formation of H1 of the study.

H1: There is a statistically significant and positive impact of digital accounting innovation on advancing Perceived ESG Performance in the financial services sector of the UK.

A positive relationship is generally indicated by the literature on the relationship between digital accounting systems and reporting transparency, though research in this area has given mixed results and ranges widely, which restricts the theoretical consistency. (Wang & Yang, 2024) offer compelling quantitative data regarding the fact that automation and real-time processing can improve the audit trail and data transparency, increasing the confidence of stakeholders. However, their attention to large firms limits generalisability, especially in industries that have varying regulatory pressures. Contrarily, (Huyen, 2024) provides qualitative evidence on the companies based in Vietnam, which indicates that cloud accounting enhances real-time transparency and decision-making. The study is contextually rich, but empirically validating underlying mechanisms, as the study relies on interviews and is focused on integration costs; thus, demonstration of the barriers to adoption is made, but the underlying constructs related to TOE are more speculative than empirically verified.

Contextual difference is also present in (Chimin, 2024), in which digital ledger uptake enhances the transparency within the Nigerian telecom companies, but the effectiveness is limited due to ineffective regulatory alignment and infrastructural constraints. This contradiction highlights the importance of institutional settings because the transparency results may be restrained by the partial compliance with coercive pressures (Cai, 2021). In a similar vein, (Ajayi-Nifise et al., 2024) revealed the possibility of blockchain to increase auditability and data integrity in accounting systems in the United States, though the study bases this possibility on the secondary review of the information, which does not allow for discerning the effectiveness of operations. In contrast, (Varzaru, 2022) further develops the argument by showing that more extensive digital ecosystems, such as AI and internet of Things, enhance national-level transparency, but differences in digital maturity across countries make comparisons less valid and undermine overall findings.

A synthesis of these studies implies that digital accounting technologies positively affect the transparency of the reporting process, particularly in accounting mechanisms, such as better integration of data, traceability, internal control, and promptness of disclosures. Institutional Theory describes a demand to be fulfilled by regulatory and stakeholder expectations of transparent reporting, and the TOE framework outlines how the organizational preparedness and technological aptitude influence the performance of implementation. Their combined application points to the fact that the results of transparency are not just a matter of technology adoption, but also of contextual fit of external pressure and internal capacity. Generally, the literature does not provide empirical evidence specific to the sector and the UK, and it is inconsistent in providing links between accounting mechanisms and transparency outcomes. It is this gap that warrants investigating the way digital accounting innovation can be converted into a quantifiable benefit in reporting transparency in a highly regulated financial services environment.

Although the previous research, such as (Nair et al., 2025; and Wang & Tang, 2024), acknowledges the beneficial impact of digital accounting innovation to improve the ESG outcomes, it tends to consider it as a single entity without taking into account the dissimilarity between the underlying technologies. It is indicated that AI, blockchain, and cloud systems are likely to affect reporting quality and accounting processes differently, as their functioning is related to different mechanisms. The lack of such a differentiation restricts the theoretical accuracy and can result in the lack of technology-specific effects. In this regard, despite the parsimonious approach of applying a composite measure of digital accounting innovation in the current study, it is clear that the composite measure does not allow the researcher to isolate the contribution of differences in technology, which means that a more detailed study in the future is necessary. Based on these literature arguments, the following hypothesis H2 is developed;

H2: There is a statistically significant and positive impact of digital accounting innovation on improving reporting transparency in the financial services sector of the UK.

2.4. Research Gap and Theorized Model

Although there is an increasing number of studies regarding digital accounting systems and their correlation with ESG and transparency, three gaps in the research appear. First, researchers (Li & Pang, 2023; and Wang & Tang, 2024) find a broad positive association between digital innovation and Perceived ESG Performance, but most of them remain country-specific to China or other emerging economies, and little is known about such dynamics in the highly regulated UK financial services sector. Second, past literature tends to address digital accounting as a homogeneous concept, despite the exploration of technologies on the topic, including blockchain, cloud, and AIS (Ajayi-Nifise et al., 2024; Li et al., 2025; Sastararuji et al., 2021). Third, little research considers the ESG outcomes on the one hand and reporting transparency on the other hand in the same study and within a common framework. This disintegration does not allow for the complete picture of how digital accounting systems can spur ESG and transparency goals in an integrated manner in the UK financial services sector.

Therefore, bridging these gaps is critical to inform policy on such areas, industry standards, and digital accounting approaches in the UK. In addition, in terms of theoretical gaps, a considerable gap exists in amalgamating Institutional Theory and TOE to elucidate ways that digital accounting innovations impact both Perceived ESG Performance and transparency in reporting, specifically within the UK’s highly regulated and controlled financial sector. While prior studies such as (Wang & Zhang, 2025; Xu et al., 2025) have integrated these theories in isolation or a non-financial setting, the current study uniquely integrates them to analyse ways that institutional pressures and environmental readiness formulate digital accounting innovation adoption, thus, it enriches theoretical comprehension about the adoption of digital accounting innovations and its impacts on Perceived ESG Performance and reporting transparency.

There are various research gaps in the current literature that this study fills. First, (Xu et al., 2025) analyze ESG reporting and digital accounting in the general corporate or manufacturing context without considering the financial services industry as one subject to strident regulation and scrutiny by ESG. Second, (Huyen, 2024) focuses on digital tools (AI, blockchain, cloud) without considering the compounded impact on Perceived ESG Performance and reporting transparency. Third, although the post-Brexit regulatory environment in the UK is unique (FCA, FRC, ISSB alignment), there is no empirical research on the sector. Fourth, the claims are dominated by theories, and empirical evidence on the connection between digital accounting and ESG outcomes is limited. Overall, prior studies show a consistent positive association, but differ in context, measurement, and theoretical grounding, highlighting the need for sector-specific and mechanism-focused analysis.

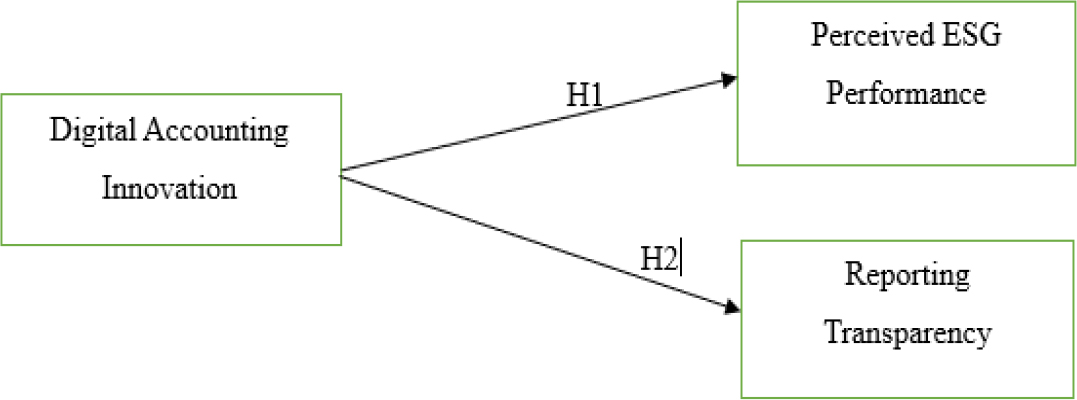

The conceptual model, (Fig. 1), shows a strategic link between digital accounting innovation and two different sustainability indicators: The model operationalizes DAI, ESG, and RT as measurable constructs, while TOE and Institutional Theory provide explanatory context rather than direct variables. Perceived ESG Performance and reporting transparency in the context of the highly regulated and digitally advanced financial services sector of the UK. Unlike prior investigations, (Dias et al., 2025; and Kawahara et al., 2024) treated ESG and digitalization as parallel and unrelated to digital accounting innovations. Therefore, in the current investigation, digital accounting innovations are integrated as a transformative force that forms the ways that ESG obligations are met by the financial services sector in the UK, along with improvements in reporting transparency.

These dimensions are captured in the current study by quantifying not just Perceived ESG Performance outcomes, but also transparency in disclosures and reporting, which, as per (Kumar et al., 2024), is a critical aspect of sustainability governance. In addition, the model’s novelty relied on a sector-specific and outcome-integrated model, which allows for bridging operational innovation in accounting processes with imperatives of ESG. It also provides actionable insights for ESG practitioners at both organizational and institutional levels, regulators, and corporate strategies to address the developing landscape of ESG disclosure and reporting.

Fig. (1). Theorized model.

3. METHODOLOGY

The data is collected using a primary data collection method where a structured survey questionnaire was used as a data collection instrument. The research instrument was based on closed-ended questions or items related to the constructs: Digital Accounting Innovation, Perceived ESG Performance, and Reporting Transparency. All the items of the constructs were measured on a likert scaling system from 1 to 5, where 1 indicated ‘Strongly Disagree,’ and 5 indicated ‘Strongly Agree’ as suggested by (Lionello et al., 2021). The likert scaling system is used as it allows for the collection of measurable and observable data related to the study topic, variables, and the research problem being investigated (Taherdoost, 2021).

The Perceived ESG Performance items were based on the adapted version of the validated scale to guarantee conceptual rigor by (Jin & Kim, 2022). The questionnaire items that have been employed in this study focus on perceived ESG outcomes as opposed to objective ESG metrics and measures. The effectiveness of digital accounting innovations in improving ESG performance and transparency in reporting was evaluated by the respondents according to the expert opinion and experience, that is, the managerial opinion, and not measured relative to the independent checked ESG data. The ESG scale was based on the (Jin & Kim, 2022) article, with only slight changes in wordings to fit the financial services environment of the UK. The items of Digital Accounting Innovation and Reporting Transparency were derived on the basis of the previous literature, (Jin & Kim, 2022; Suhardjo et al., 2024), because the validated scales were not available in this particular case. The expert evaluation was used to guarantee content validity, where the relevance, clarity, and appropriateness of the items to the context were evaluated by the academic and industry professionals prior to the questionnaire being finalized (n = 35).In terms of reliability and validity of the items, (Jin & Kim, 2022) reported that for all items, Cronbach’s Alpha was found to be 0.920, which established robust reliability, and AVE of 0.491 established convergent validity. Moreover, the digital accounting innovation and reporting transparency items were created after reviewing the literature broadly and being relevant to the UK financial services industry. Digital Accounting Innovation (DAI) is conceptualized and operationalized as a firm-level composite measure that measures the degree of uptake of AI, blockchain, and cloud-based accounting systems, as opposed to evaluating the technologies individually. This metric depicts the general digitization and the adoption of accounting innovations in the organization and gives a comprehensive assessment of the way in which digital solutions as a whole contribute to ESG performance and reporting transparency. Expert review and pilot testing were used to determine content validity. Cronbach’s Alpha was obtained as 0.838, and Average Variance Extracted (AVE) was obtained as 0.674, which established construct reliability and validity, and all the constructs were found to have adequate internal consistency and convergent validity.

The questionnaire is based on two different main sections, where the first section comprises a demographics section and the second section is based on constructs of the model framework. The constructs section is further divided into three sub-sections: Digital Accounting Innovation, an independent variable, and Perceived ESG Performance and Reporting Transparency, a dependent variable (Appendix A). The questionnaire in this study was designed to be specific to this study directing to match the aims of the research and the constructs of digital accounting innovation, Perceived ESG Performance, and reporting transparency identified. The questionnaire was assessed through pilot testing on 70 representatives of the UK financial services industry to make sure it was clear, relevant, and comprehensive. The pilot feedback was used to make changes, improving the wording and structure of items. The validity and reliability of the research instrument were tested using Cronbach’s Alpha and Composite reliability values against the threshold of 0.7 as highlighted by (Lionello et al., 2021). In addition, convergent validity of the model was tested using the Average Variance Extracted (AVE) approach against a threshold value of 0.5. The study’s participants are industry experts, comprised of finance and reporting managers, accounts officers, and auditors working in the financial services industry of the UK. The reason behind the selection of industry experts relevant to the study topic is justified by the arguments of (Taherdoost, 2021) that research participants possessing in-depth knowledge regarding the particular research problem or topic provide authentic opinions and responses, which adds to the reliability and validity of the collected data for further analysis.

In this study, as suggested by (Rahman et al., 2022) purposive sampling method was applied, where the target population consists of professionals who work in the UK financial services sector. They were approached on LinkedIn and ICAEW forums. This way, the data was collected from participants with the relevant expertise in accounting and ESG reporting, which guaranteed the credibility of the data. Though this approach offers no equal opportunity of selection, it limits generalization. G*Power 3.1 was used to determine the minimum sample size with a significance level of (a) = 0.05, power (1-b) = 0.95 and medium effect size (f2 = 0.15) to be used in multiple regression. The analysis recommended a minimum sample of 300 participants, which was attained, and offered sufficient statistical power for PLS-SEM analysis, as indicated by (Cseadm, 2025). The technique also makes the sample large enough to identify the hypothetical relationships, but it represents the purposive, expert-centered design of the study.

After approaching 500 participants, 350 completely filled and valid responses were received, yielding 70% response rate. After excluding incomplete responses, 300 valid responses were retained for analysis, resulting in an effective response rate of 60%. Such an attrition rate is in line with the online professional survey research, and it is mainly due to half-complete responses and not an automatic withdrawal, as adopted by (Dake et al., 2022) also. In order to determine the possibility of bias, tests of non-response bias were undertaken through early-late respondent comparisons, and this showed that there were no statistically significant differences. Hence, the end result is a sample that is said to be representative and can be analyzed statistically, and the inference can be made to be valid. Participants were approached on professional platforms such as LinkedIn and ICAEW forums with the help of informed consent, which informed them about the purpose of the study and its aim to ensure voluntary participation. The issue of selection bias was addressed by targeting participants from different roles, such as accountants, finance managers, ESG officers, and auditors across multiple sectors, such as banking, insurance, and investment. In addition, it was also essential to check for non-response bias. (Elston, 2021) indicated that non-respondents are similar to late respondents, and there is no statistically significant difference between late and early respondents, which indicates no concern for non-response bias. Therefore, following the approach specified by (Bareinboim et al., 2022), the study carried out an independent sample T-test to compare statistically significant differences between early (P1 = 30) and late (P2 = 30) respondents. None of the variables depicted any statistically significant difference between n1 and n2, which signified that the data collection technique was not affected by non-response bias. Further, in order to address the issue of common method bias (CMB), Harman Single factor testing was applied, which yielded less than 50% variance indicting no issue. As specified by (Kyriazos & Poga, 2023), confidentiality and anonymity were assured, and items’ wording was designed carefully to decrease social desirability. In terms of statistical approach, values of the variance inflation factor (VIF), which, according to (Afthanorhan et al., 2021), should be lower than 3.3. As the constructs in the model represented a VIF value of below 3.3, it signified that common method bias was not the concern in the study.

The analysis of the data was performed with the help of PLS-SEM in SmartPLS, and the bootstrapping procedure with 5,000 resamples was applied to estimate the importance of path coefficients and outer loadings. The outer loadings of the items were measured, making sure that each indicator made a significant contribution to its latent construct (p < 0.05). Bootstrapping allowed the effective estimation of standard errors and t-statistics, which confirmed the reliability and validity of constructs and gave assurance of confidence in the structural relationships that were being tested in the model. As suggested by (Fauzi, 2022), also. The measurement model assesses the validity and reliability of the constructs using Cronbach’s alpha and Composite reliability against the threshold value of 0.7 (Nawi et al., 2022). Further, factor loading higher than 0.6 depicted the validity of the indicators. In addition, Average Variance Extracted (AVE) values higher than 0.5 were considered to show high convergent validity, while the HTMT ratio below 0.85 depicted discriminant validity (Gorai et al., 2024). In the second stage, path coefficient analysis was carried out to analyse causality and its significance levels.

The study applied PLS-SEM due to the fact of its appropriateness for multifactored models with multiple constructs, with small to medium sample sizes, and a focus on identifying predictive relationships, which allows concurrent evaluation of measurement and structural models, as suggested by (Kanaparthi, 2024). The proposed methodology is used to investigate the relationship between digital accounting innovation, perceived ESG Performance, and reporting transparency within the UK financial services industry. Nonetheless, the same-source, cross-sectional survey data used has a possibility of common method bias and restricts causal inference. Although PLS-SEM addresses a few of the estimation problems, longitudinal/ multi-source data would enhance generalisability and decrease self-reporting biases.

4. RESULTS AND DISCUSSION

4.1. Demographic Profile

The results in Table 1 show demographic analysis of the participants of the study. It can be observed that out of the total (n = 300) participants, (54.67%) are male participants, while (45.33%) are female participants. In addition, the statistics also show that (51.66%) of the participants lie within the age group of 36-55 years, while (48.33%) of the participants lie within the age group of 18-35 years. In addition, with respect to the job position of the participants, (33%) of the participants were ESG officers, (24%) of the participants were finance managers, and (21.33%) were auditors, which signifies that data is collected from relevant participants. Moreover, in terms of industry experience of the participants, (30%) are 7-10 years experienced, where (26.67%) hold above 10 years of industry experience.

Table 1. Demographic analysis.

| Demographic Category | – | Frequency (n) | Percentage (%) |

| Gender | Male | 164 | 54.67% |

| Female | 136 | 45.33% | |

| Age Range | 18-25 | 70 | 23.33% |

| 26-35 | 75 | 25.00% | |

| 36-45 | 85 | 28.33% | |

| 46-55 | 70 | 23.33% | |

| Job Title/Position | Accountant | 65 | 21.67% |

| Finance Manager | 72 | 24.00% | |

| Auditor | 64 | 21.33% | |

| ESG Officer | 99 | 33.00% | |

| Department | Accounting | 72 | 24.00% |

| Finance | 80 | 26.67% | |

| Compliance | 65 | 21.67% | |

| ESG/Sustainability | 83 | 27.67% | |

| Experience in the Financial Industry | 1-3 years | 68 | 22.67% |

| 4-6 years | 62 | 20.67% | |

| 7-10 years | 90 | 30.00% | |

| Above 10 years | 80 | 26.67% |

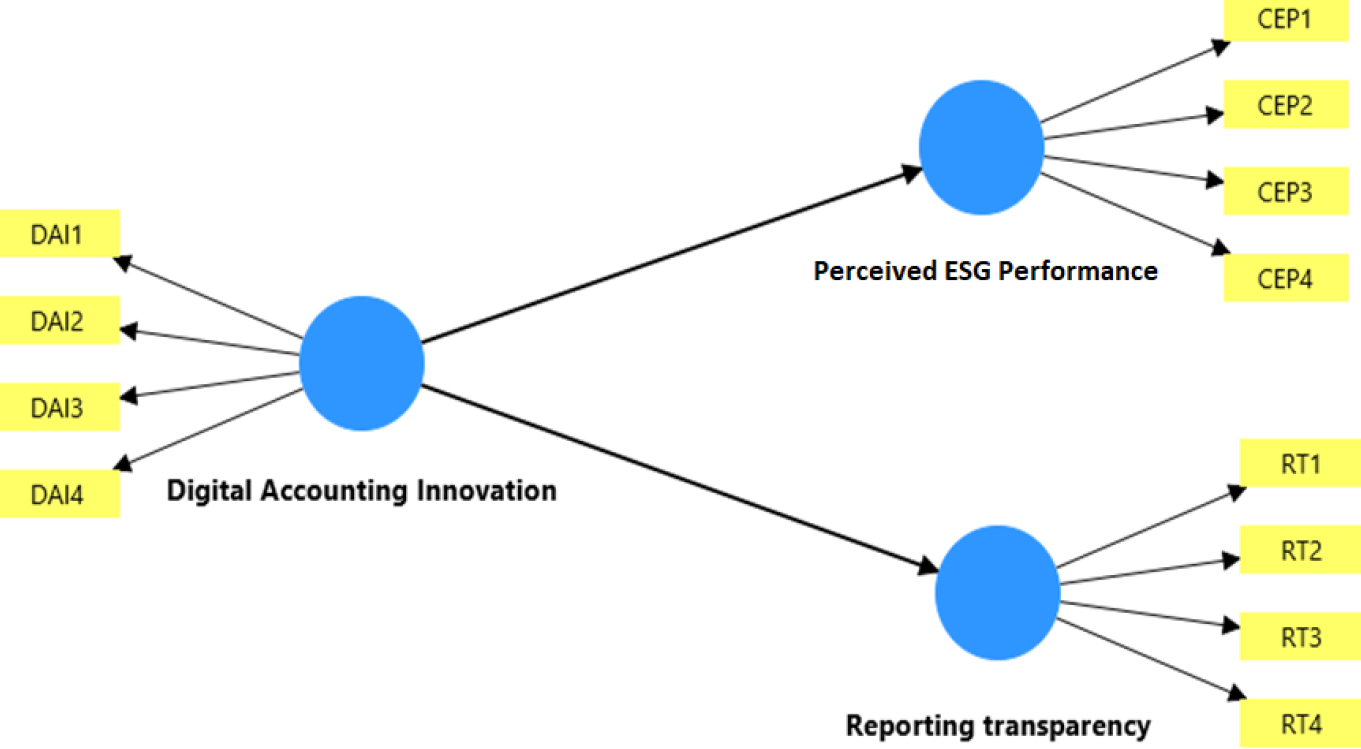

4.2. Measurement Model Using Confirmatory Factor Analysis (CFA)

The reliability and validity of the measurement model, as shown in Fig. (2), are assessed with several indicators, which are comprised of Cronbach’s Alpha, Composite Reliability against its threshold value of 0.7, and AVE against the threshold value of 0.5. Table 2 depicts findings of internal consistency and reliability, and validity of the constructs with all measures aligned with the pre-determined threshold values, thus indicating strength and internal consistency of the obscurement model. The results of CFA, shown in Table 2, validate the robust validity and reliability of each construct in the study. For instance, high factor loading was observed, ranging between 0.744 and 0.908. Also, all the constructs are found to have higher Cronbach ‘s Alpha value and AVE surpassing standard thresholds, which establishes the reliability and validity of the constructs.

Table 2. Measurement model.

| Latent Variables | Indicators | Factor Loadings | Cronbach’s Alpha | Composite Reliability | AVE |

| Perceived ESG Performance | CEP1 | 0.876 | 0.915 | 0.917 | 0.796 |

| CEP2 | 0.908 | ||||

| CEP3 | 0.896 | ||||

| CEP4 | 0.889 | ||||

| Digital Accounting Innovation | DAI1 | 0.814 | 0.838 | 0.841 | 0.674 |

| DAI2 | 0.879 | ||||

| DAI3 | 0.812 | ||||

| DAI4 | 0.776 | ||||

| Reporting Transparency | RT1 | 0.774 | 0.815 | 0.821 | 0.645 |

| RT2 | 0.861 | ||||

| RT3 | 0.828 | ||||

| RT4 | 0.744 |

Fig. (2). Measurement model of the study.

The analysis of discriminant validity is applied to confirm and validate whether each construct in the measurement model is separate and distinct from other constructs in the model framework, as shown in Table 3. To examine this, HTMT is used, which requires values to be below 0.85 (Nawi et al., 2022). As depicted in Table 3, the value of HTMT amid Corporate ESG Governance and Digital Accounting Innovation is 0.75, and amid Reporting Transparency and Digital Accounting Innovation is 0.679. As both values are observed to be less than the threshold of 0.85. The least value was found amid Reporting Transparency and Perceived ESG Performance at 0.659, which signifies high discriminant validity. Therefore, the results validate that the constructs in the model framework are distinct and separate from each other, which is ideal for analyzing causal relationships in structural model analysis.

Table 3. Discriminant validity.

| – | Perceived ESG Performance | Digital Accounting Innovation |

| Digital Accounting Innovation | 0.754 | – |

| Reporting transparency | 0.659 | 0.679 |

4.3. Path Analysis

The results of the path coefficient depicted in Table 4 exhibit statistically significant and positive relationships among constructs of the model framework, thus supporting the hypotheses of the current study. For instance, the Digital Accounting Innovation was found to be statistically significantly and positively related to Perceived ESG Performance (β = 0.664, and p = 0.001), which implies that with the implementation of digital accounting systems, UK financial services firms can gain improved ESG disclosure and performance. In similar terms, Digital Accounting Innovation is also found to be statistically significantly and positively associated with Reporting Transparency (β = 0.563, and p = 0.001), which indicates that accounting practices driven by technology, such as Blockchain Machine Learning contributes towards enhancing reporting transparency and Perceived ESG Performance within the UK financial services industry. The F-square values show the effect size of Digital Accounting Innovation on the Perceived ESG Performance and Reporting transparency. For Perceived ESG Performance, ƒ² = 0.787, a large effect, which depicts a substantial contribution to explained variance. In terms of Transparency, ƒ² = 0.464, also a large effect, which also shows substantial impact on the explanatory power of the model.

Table 4. Path coefficient analysis.

| – | Path Coefficients | T-Statistics | P-Values | f-Square |

| Digital Accounting Innovation -> Perceived ESG Performance | 0.663*** | 23.204 | 0.000 | 0.787 |

| Digital Accounting Innovation -> Reporting transparency | 0.562*** | 13.758 | 0.000 | 0.464 |

Note: *** indicates significance at 1%, ** indicates significance at 5%, * indicates significance at 10%

4.4. Model Explanatory Power

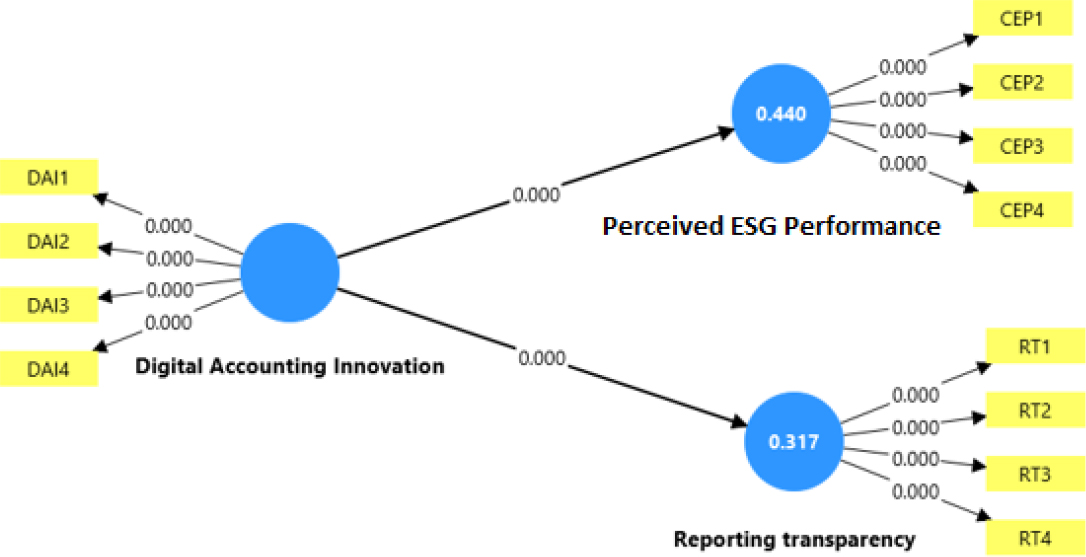

To assess the explanatory power of the model, R-squared and adjusted R-squared are analyzed for every dependent construct (Ozili, 2023). The values of R-squared show the percentage of variance in the target construct explained by its predictors, whereas adjusted R-squared explains the complexity of the model and sample size (Hayes, 2021). The values of R-squared depict moderate explanatory power of predictors for their target variable. Table 5 provides a summary of R-squared results, perceived ESG Performance, and reporting transparency predicted by digital accounting innovation. The value of R-squared exhibited in Fig. (3) and Table 5, which signifies that 31.7% of the variation in Reporting Transparency is elucidated by Digital Accounting Innovation. Table 5 also depicts that Digital Accounting Innovation explains (44%) of the variation in Perceived ESG Performance.

Table 5. Model explanatory power.

| R-Square | R-Square Adjusted | |

| Perceived ESG Performance | 0.440 | 0.439 |

| Reporting transparency | 0.317 | 0.315 |

Fig. (3). Model after bootstrapping.

5. DISCUSSION AND HYPOTHESES ASSESSMENT

The statistical results and findings of the current study unveiled a significant and strong positive relationship between digital accounting innovation and Perceived ESG Performance in the UK financial services sector; however, these findings reflect perceptual assessments rather than objective ESG outcomes. These results indicate that the adoption of technology is directly related to Perceived ESG Performance, which includes environmental programs, social responsibility programs, and compliance with governance, rather than the perceived transparency of reporting itself. These findings indicate actions on the enhancement of the quality of accounting information, internal controls, audit trails, and timeliness of ESG disclosures, as opposed to real quantifiable sustainability results, which are also unveiled by (Cai, 2021). Whereas the mature regulatory environment and culture of governance in the UK lead to adoption, other reasons that could have led to adoption are managerial optimism of respondents or their familiarity with the digital systems supported in the analysis of (Chimin, 2024) as well. The TOE model confirms this illustration, because organizational preparedness and technical structure allow effective incorporation of ESG data. Hence, it can be said that digital accounting tools can aid ESG reporting processes and auditability, and increase stakeholder trust, and the observed disparities in the effect sizes highlight the necessity to distinguish between operational perceived ESG Performance and perceived reporting transparency in future studies.

The findings support the previous studies not only but also indicate contextual differences. To illustrate, (Li & Pang, 2023; and Wang & Yang, 2024) claim that digital accounting technologies can improve the perceived ESG Performance due to the green innovation and governance processes. However, the findings mostly rely on the Chinese companies, where ESG models are centrally controlled, and the use of digital accounting is determined by the coercive institutional factors. On the other hand, the UK has a market-driven regulatory framework that is more likely to be affected by normative pressure because it can affect the introduction of digital accounting practices in different ways. It is necessary to mention that, despite the fact that in this study no distinction is made regarding the types of digital innovation, the findings are based on perceived improvement of the ESG performance, but not on objective results. Such perceptions can probably be attributed to good governance standards and strict compliance standards set by the FCA in the UK financial market. This implies that institutional settings and the industry standards of governance are crucial in the interpretation and assessment of digital accounting tools, and the necessity to be careful in the contextualization of the cross-country results, instead of the overgeneralization of the results.

In addition, the results of the current study are supported by the TOE Framework, as financial services firms in the UK are leveraged with advanced technological infrastructure. Effective adoption of digital accounting innovation is facilitated by both robust environmental regulation and mature organizational capabilities that authentically improve Perceived ESG Performance. Therefore, these findings imply that the UK financial services sector must amalgamate the strategic significance of integrating digital accounting innovation within agendas of ESG, now just for the purpose of compliance, but likewise for competitive advantage and developing stakeholder trust in the future, reinforcing the important role of technology in sustainable Perceived ESG Performance.

Moreover, the current study has also validated a statistically significant and positive relationship between digital innovation in accounting practices and the transparency of ESG reporting within the UK financial services sector. The findings suggest that the digital accounting innovation is positively related to improved reporting transparency in the UK financial services industry, which demonstrates the positive changes in the quality of accounting information, internal control, and auditability. It aligns with (Efunniyi et al., 2024), illustrating those digital technologies, including AI-powered Accounting Information Systems and blockchain, enhance financial reporting transparency and timeliness of ESG reporting, boosting the credibility of stakeholders in the information reported. These results are structurally supported by the increased regulatory and institutional climate in the UK, comprising FCA, IASSB, and SDR systems (Suhardjo et al., 2024). Other possible explanations are management optimism or knowledge of technology, which could affect the way respondents perceive it, instead of there being an improvement in reporting. In the context of the UK, compared to developing regions like Nigerian telecom companies, where regulating gaps and inadequate infrastructure lower the level of transparency (Chimin, 2024), the relationship of institutional pressure and organizational preparedness is evident. Therefore, the results indicate that digital accounting innovations have a significant beneficial effect on ESG reporting, and the results obtained should be viewed with reservations, separating perceptual links from the results of obtained operations. These results are in line with (Wang & Wang, 2025), who evidence that AIS can be improved through AI and Machine Learning to improve the transparency of the reporting process, allowing to detect errors in real-time, increasing the accuracy of the presented data, and improving the auditability of the process. Likewise, (Ajayi-Nifise et al., 2024) emphasize the ability of blockchain to enhance data integrity and traceability and indicate that digital accounting technologies can significantly enhance reporting transparency. Though these results are contextual, for instance, an example is that (Chimin, 2024) finds that in the Nigerian telecom industry, digital ledgers do not lead to improved reporting transparency because the institutional capacity is low, there is low investment, and regulatory maturity is underdeveloped. This comparison shows how important institutional and regulatory environments are in defining the effectiveness of digital accounting tools. The UK markets have an enabling environment, as the existence of strict ESG and reporting frameworks, such as FCA, ISSB, and SDR, allows digital innovations to have a significant impact on transparency. Such results indicate that the enhancement of reporting is not only technology-based but also depends on the governance of the sector, institutional maturity, and compliance infrastructure. Table 6 below shows the hypotheses assessment summary indicated the acceptance/rejection of the hypotheses proposed earlier in the research.

Table 6. Hypotheses assessment summary.

| S. No. | Hypotheses | Accepted/Rejected |

| 1 | H1: There is a statistically significant and positive impact of digital accounting innovation on advancing Perceived ESG Performance in the financial services sector of the UK. | Accepted |

| 2 | H2: There is a statistically significant and positive impact of digital accounting innovation on improving reporting transparency in the financial services sector of the UK. | Accepted |

CONCLUSION

The current study examined the relationship of digital accounting innovation with perceived ESG Performance and reporting transparency in the case of the financial services sector of the UK. The findings obtained from the structural model of the study verified statistically significant and positive associations, which exhibited that digital accounting innovation improves Perceived ESG Performance and boosts transparency in financial reporting. The findings of the study are also aligned with international evidence and reflect the unique regulatory and institutional context of the UK. Lastly, the findings of the current study contribute towards existing literature by demonstrating ways that digital innovations tend to be directly associated with Perceived ESG Performance and reporting transparency in the financial services sector of the UK. For practitioners, the evidence generated from the findings signifies the value of integrating AI and blockchain to streamline disclosures and enhance transparency in reporting by avoiding unnecessary perceived ESG Performance claims. The results also guide financial institutions to align the developing regulatory requirements while enhancing competitiveness, long-term sustainability, and accountability by means of credible practices of ESG reporting.

LIMITATIONS AND FUTURE IMPLICATIONS

At one end, valuable insights are provided by the study; on the other hand, it also holds several limitations. For instance, the study is emphasized on the financial services sector of the UK, which tends to limit the generalization of the findings to other regions or industrial sectors. Secondly, the capacity to infer long-term effects of the findings is restricted by the cross-sectional design of the study. The study’s cross-sectional nature and sectoral focus limit the ability to make relational inferences and generalisability. Also, purposive professional-network sampling is not without non-probability bias, and same-source, self-reporting could exaggerate correlations because of common method variance. Moreover, the use of perceptual indicators of perceived ESG Performance and reporting transparency, instead of real perceived ESG Performance, restricts the capability of evaluating operational or financial performance as a result. As DAI is modeled as a composite construct, the differential effects of AI, blockchain, and cloud systems cannot be isolated. This composite construct could hide the effects of technology on ESG performance and transparency in reporting. Further studies are also required to disaggregate DAI into different elements of technologies and to study their independent and comparative impacts in different organizational and regulatory settings.

In addition, the study did not distinguish among the kinds of digital accounting innovations in accounting systems, such as AI and blockchain, which could have provided different impacts. Therefore, in terms of future implications of the study, future researchers can implement longitudinal designs to carry out sectoral and industrial comparisons, and also integrate qualitative insights along with quantitative analysis. It will provide deeper analysis and evidence, and improved generalization of the findings. In addition, the inclusion of mediating variables such as organizational culture or regulatory pressure from external bodies can also provide an in-depth understanding of innovation outcomes.

POLICY IMPLICATIONS

The findings of the current study offer precise policy implications for policymakers, regulators, and financial reporting managers of the financial services sector of the UK. In terms of implications for policymakers, they are suggested to give priority to the integration of digital accounting systems through upgrading digital infrastructure in the financial services sector of the UK. In addition, regulatory bodies such as the Financial Conduct Authority (FCA) are suggested to mandate standardized frameworks of ESG disclosure to improve transparency, consistency, and auditability. Moreover, the findings also imply that capacity-building programs should be launched to upskill finance professionals with digital accounting tools, which can guarantee the finest practices related to the adoption of digital innovation in accounting systems, decrease the cost of compliance with international ESG reporting standards.

LIST OF ABBREVIATIONS

| AVE | = | Average Variance Extracted |

| CFA | = | Confirmatory Factor Analysis |

| CMB | = | Common Method Bias |

| DAI | = | Digital Accounting Innovation |

| FCA | = | Financial Conduct Authority |

| PLS-SEM | = | Partial Least Squares Structural Equation Modeling |

| RT | = | Reporting Transparency |

| SDR | = | Sustainability Disclosure Requirements |

| SDRs | = | Special Drawing Rights |

| TOE | = | Technology-Organization-Environment |

| VIF | = | Variance Inflation Factor |

AUTHOR’S CONTRIBUTION

F.A. has contributed to conceptualization, idea generation, problem statement, methodology, results analysis, results interpretation.

ETHICAL STATEMENT & INFORMED CONSENT

Not applicable.

AVAILABILITY OF DATA AND MATERIALS

The data will be made available on reasonable request by contacting the corresponding author [F.A.].

FUNDING

None.

CONFLICT OF INTEREST

The author declares no conflicts of interest, financial or otherwise.

ACKNOWLEDGEMENTS

Declared none.

DECLARATION OF AI

During the preparation of this manuscript, the author used ChatGPT for language polishing. After utilizing this tool, the author carefully reviewed and refined the content as necessary and accept full responsibility for the accuracy and integrity of the published work.

APPENDIX A

| Question | Response Options |

| Age | ☐ 18–25 ☐ 26–35 ☐ 36–45 ☐ 46–55 |

| Gender | ☐ Male ☐ Female |

| Job Position | ☐ Accountant ☐ Finance Manager ☐ Auditor ☐ ESG Officer |

| Department | ☐ Accounting ☐ Finance ☐ Compliance ☐ ESG/Sustainability |

| Experience in the Financial Industry | ☐ 1–3 years ☐ 4–6 years ☐ 7–10 years ☐ 10+ years |

Instruction: Please indicate your level of agreement with the following statements.

Scale: 1 = Strongly Disagree, 2 = Disagree, 3 = Neutral, 4 = Agree, 5 = Strongly Agree

| A. Independent Variable: Digital Accounting Innovation | |||||

| Statement | 1 | 2 | 3 | 4 | 5 |

| My organisation has adopted modern digital accounting systems (e.g., AI, blockchain). | |||||

| Digital accounting tools have streamlined financial processes in my department. | |||||

| Digital accounting innovation has improved the accuracy of financial data. | |||||

| Management supports the continuous adoption of new accounting technologies. | |||||

| B. Dependent Variable: Perceived ESG Performance. Adopted from (Jin & Kim, 2022). | |||||

| Statement | 1 | 2 | 3 | 4 | 5 |

| Our company propels carbon emission-reducing activities and is practicing environmental management. | |||||

| Our company carries out social donation and corporate social responsibility (CSR) activities for communities. | |||||

| Our company is implementing a policy for employees’ employment stability. | |||||

| Our company performs continuous disclosures (publishing sustainability management reports) externally on our board of directors and information. | |||||

| C. Dependent Variable: Reporting Transparency | |||||

| Statement | 1 | 2 | 3 | 4 | 5 |

| Our financial reports are generated with minimal manual intervention. | |||||

| Stakeholders can access real-time financial and ESG-related data. | |||||

| Our reporting practices are more transparent due to digital technologies. | |||||

| Digital accounting systems help reduce the risk of financial misstatements. |

REFERENCES

Afthanorhan, A., Awang, Z., Majid, N. A., Foziah, H., Ismail, I., Halbusi, H. A., & Tehseen, S. (2021). Gain more insight from common latent factor in structural equation modeling. Journal of Physics: Conference Series, 1793(1), 1-9.

https://doi.org/10.1088/1742-6596/1793/1/012030.

Ajayi-Nifise, A. O., Falaiye, T., Olubusola, O., Daraojimba, A. I., & Mhlongo, N. Z. (2024). Blockchain in US accounting: a review: assessing its transformative potential for enhancing transparency and integrity. Finance & Accounting Research Journal, 6(2), 159-182.

https://doi.org/10.51594/farj.v6i2.786.

Bank of England (2024). Artificial intelligence in UK financial services 2024. Available from: https://www.bankofengland.co.uk/report/2024/artificial-intelligence-in-uk-financial-services-2024.

Bareinboim, E., Tian, J., & Pearl, J. (2022). Recovering from selection bias in causal and statistical inference. Proceedings of the Twenty-Eighth AAAI Conference on Artificial Intelligence, 2410-2416.

https://doi.org/10.1609/aaai.v28i1.9074.

Cai, C. W. (2021). Triple‐entry accounting with blockchain: how far have we come? Accounting & Finance, 61(1), 71-93.

https://doi.org/10.1111/acfi.12556.

Chimin, I. S. (2024). Effect of Digital Ledger on Financial Reporting Transparency of Listed Telecommunications Companies in Nigeria. ANUK College of Private Sector Accounting Journal, 1(2), 177-182. Available from: https://www.anukpsaj.com/psaj/article/view/61/48.

Collis, R., & Zheng, Y. (2025). UK sustainability reporting standards S1 and S2 – exposure draft. Saffery. Available from: https://www.saffery.com/insights/articles/uk-sustainability-reporting-standards-s1-and-s2-exposure-draft/.

Dake, D. K., & Buabeng-Andoh, C. (2022). Using Machine Learning Techniques to Predict Learner Drop‐out Rate in Higher Educational Institutions. Mobile Information Systems, 2022(1), 2670562, 1-9.

https://doi.org/10.1155/2022/2670562.

Dias, S. N., Dewasiri, N. J., & Perera, K. L. (2025). Digitalisation and Its Impact on the Organisation Performance and Sustainability: A Systematic Literature Review. Sustainable Innovations and Digital Circular Economy, 165-188.

https://doi.org/10.1007/978-981-96-1064-8_9.

Ediagbonya, V., & Tioluwani, C. (2023). The role of fintech in driving financial inclusion in developing and emerging markets: issues, challenges and prospects. Technological Sustainability, 2(1), 100-119.

https://doi.org/10.1108/TECHS-10-2021-0017.

Efunniyi, C. P., Abhulimen, A. O., Obiki-Osafiele, A. N., Osundare, O. S., Agu, E. E., & Adeniran, I. A. (2024). Strengthening corporate governance and financial compliance: Enhancing accountability and transparency. Finance & Accounting Research Journal, 6(8), 1597-1616.

https://doi.org/10.51594/farj.v6i8.1509.

Elston, D. M. (2021). Participation bias, self-selection bias, and response bias. Journal of the American Academy of Dermatology.

https://doi.org/10.1016/j.jaad.2021.06.025.

Fauzi, M. A. (2022). Partial Least Square Structural Equation Modelling (PLS-SEM) in Knowledge Management Studies: Knowledge Sharing in Virtual Communities. Knowledge Management & E-Learning, 14(1), 103-124.

https://doi.org/10.34105/j.kmel.2022.14.007.

Financial Conduct Authority (FCA) (2023). Sustainability disclosure requirements (SDR) and investment labels (PS23/16). Available from: https://www.fca.org.uk/publication/policy/ps23-16.pdf.

Gorai, J., Kumar, A., & Angadi, G. R. (2024). Smart PLS-SEM modeling: Developing an administrators’ perception and attitude scale for apprenticeship programme. Multidisciplinary Science Journal, 6(12), e2024260.

https://doi.org/10.31893/multiscience.2024260.

Government of the UK (2023). Mobilising green investment: 2023 green finance strategy. Available from: https://www.gov.uk/government/publications/green-finance-strategy.

Hayes, T. (2021). R-squared change in structural equation models with latent variables and missing data. Behavior Research Methods, 53(5), 2127-2157.

https://doi.org/10.3758/s13428-020-01532-y.

Hossain, M. N., Hidayat-ur-Rehman, I., Bhuiyan, A. B., & Salleh, H. M. (2025). Evaluating the influence of IT governance, Fintech adoption, and financial literacy on sustainable performance. Studies in Economics and Finance.

https://doi.org/10.1108/SEF-10-2024-0672.

Huyen, G. T. T. (2024). The impact of cloud accounting on financial transparency and decision making in Vietnamese enterprises. Sciences of Conservation and Archaeology, 36(4), 227-242. Available from: https://sci-arch.org/index.php/wwbhen/article/view/107.

Jin, M., & Kim, B. (2022). The effects of ESG activity recognition of corporate employees on job performance: The case of South Korea. Journal of Risk and Financial Management, 15(7), 316.

https://doi.org/10.3390/jrfm15070316.

Kanaparthi, V. (2024). Exploring the impact of blockchain, AI, and ML on financial accounting efficiency and transformation. International Conference on Multi-Strategy Learning Environment, 353-370.

https://doi.org/10.1007/978-981-97-1488-9_27.

Kawahara, N., Fitriasari, D., & Irie, N. (2024). Debatable Nature of Environmental, Social, and Governance Information: Focusing on Mandatory Disclosures. Kindai Management Review, 12, 90-105. Available from: https://www.kindai.ac.jp/files/rd/research-center/management-innovation/kindai-management-review/vol12_5.pdf.

Ketterling, C. I. (2025). The Global Landscape of ESG Guidelines and Standards: Corporate Social Responsibility, Responsible Investment, and ESG Compliance. Available from: https://osf.io/preprints/osf/47efm_v4.

Kumar, A., Yadav, U. S., Mandal, M., & Yadav, S. K. (2024). Impact of Corporate Innovation, Technological Innovation and ESG on Environmental Performance: Moderation Test of Entrepreneurial Orientation and Technological Innovation as Mediator Using Sobel Test. International Journal of Sustainable Development & Planning, 19(7), 2635-2650.

https://doi.org/10.18280/ijsdp.190720.

Kyriazos, T., & Poga, M. (2023). Dealing with multicollinearity in factor analysis: the problem, detections, and solutions. Open Journal of Statistics, 13(3), 404-424.

https://doi.org/10.4236/ojs.2023.133020.

Li, S., Zhu, J., Chen, P., Li, Z., Liao, C., & Feng, W. (2025). Exploring high-performance green innovation in China’s logistics companies: a TOE framework based on fsQCA. Frontiers in Environmental Science, 12, 1511269.

https://doi.org/10.3389/fenvs.2024.1511269.

Li, W., & Pang, W. (2023). The impact of digital inclusive finance on Perceived ESG Performance: based on the perspective of corporate green technology innovation. Environmental Science and Pollution Research, 30(24), 65314-65327.

https://doi.org/10.1007/s11356-023-27057-3.

Lionello, M., Aletta, F., Mitchell, A., & Kang, J. (2021). Introducing a method for intervals correction on multiple Likert scales: A case study on an urban soundscape data collection instrument. Frontiers in Psychology, 11, 602831.

https://doi.org/10.3389/fpsyg.2020.602831.

Nair, A., Manohar, S., & Mittal, A. (2025). AI-enabled FinTech for innovative sustainability: Promoting organizational sustainability practices in digital accounting and finance. International Journal of Accounting & Information Management, 33(2), 287-312.

https://doi.org/10.1108/IJAIM-05-2024-0172.

Nawi, F. A. M., Mamat, M., Baistaman, J., Setapa, M., & Ramli, N. H. (2022). The SEM SmartPLS Model Assessment: Mediating Influence of Technology Infrastructure Support on Human Capital Determinants in TVET Institutions. Sciences, 12(11), 2724-2735.

https://doi.org/10.6007/IJARBSS/v12-i11/15410.

Norton Rose Fulbright (2022). ESG: Key regulatory risks for financial services firms in the UK and US and how to manage them. Available from: https://www.nortonrosefulbright.com/en/knowledge/publications/110bb2f1/esg-key-regulatory-risks-for-financial-services-firms-in-the-uk-and-us-and-how-to-manage-them.

Ozili, P. K. (2023). The Acceptable R-Square in Empirical Modelling for Social Science Research. Social Research Methodology and Publishing Results (pp 1-9).

http://doi.org/10.2139/ssrn.4128165.

Patel, S., & Patyrykin, K. (2025). Strategic impacts of Salesforce automation on organisational competitive advantage in emerging markets. Journal of Posthumanism, 5(12), 357-372.

https://doi.org/10.63332/joph.v5i12.3782.

Patyrykin, K., & Vasyukova, L. (2025). Environmental accountability or symbolic compliance? A critical review of ESG ratings, greenwashing, and indirect emissions in the global insurance sector. International Journal of Energy Economics and Policy, 15(6), 917-925.

https://doi.org/10.32479/ijeep.22770.

Rahman, M. M., Tabash, M. I., Salamzadeh, A., Abduli, S., & Rahaman, M. S. (2022). Sampling techniques (probability) for quantitative social science researchers: a conceptual guideline with examples. Seeu Review, 17(1), 42-51.

https://doi.org/10.2478/seeur-2022-0023.

Sastararuji, D., Hoonsopon, D., Pitchayadol, P., & Chiwamit, P. (2021). Cloud Accounting Adoption in Small and Medium Enterprises: An Integrated Conceptual Framework: Five factors of determinant were identified by integrated Technology-Organization-Environment framework, Diffusion of Innovation, Institutional Theory and extended factors. 2nd International Conference on Industrial Engineering and Industrial Management, 32-38.

https://doi.org/10.1145/3447432.3447439.

Suhardjo, S., Wati, Y., Renaldo, N., Musa, S., & Cecilia, C. (2024). Implementation of Digital Accounting on the Effectiveness of Corporate Social Responsibility and Environmental, Social, and Governance Reporting. Interconnection: An Economic Perspective Horizon, 2(1), 41-49.

https://doi.org/10.61230/interconnection.v2i1.90.

Taherdoost, H. (2021). Data collection methods and tools for research; a step-by-step guide to choose data collection technique for academic and business research projects. International Journal of Academic Research in Management (IJARM), 10(1), 10-38.

https://hal.science/Hal-03741847/.

Vărzaru, A. A. (2022). An empirical framework for assessment of the effects of digital technologies on sustainability accounting and reporting in the European Union. Electronics, 11(22), 3812.

https://doi.org/10.3390/electronics11223812.

Wang, L., & Yang, H. (2024). Digital technology innovation and Perceived ESG Performance: evidence from China. Economic Change and Restructuring, 57(6), 207.

https://doi.org/10.1007/s10644-024-09791-x.

Wang, S. and Zhang, H. (2025). How does digital supply chain transformation determine environmental, social, and governance (ESG) performance? Mediating role of firm integration and moderating effect of organizational digital culture. Operations Management Research, 18, 960-986.

https://doi.org/10.1007/s12063-025-00561-0.

Wang, Y., & Wang, D. D. (2025). The dual path of the impact of digital technology adoption on Perceived ESG Performance. Sustainability, 17(6), 2341.

https://doi.org/10.3390/su17062341.

Wang, Z., & Tang, P. (2024). Substantive digital innovation or symbolic digital innovation: Which type of digital innovation is more conducive to Perceived ESG Performance? International Review of Economics & Finance, 93, 1212-1228.

https://doi.org/10.1016/j.iref.2024.05.023.

Wu, S., & Li, Y. (2023). A study on the impact of digital transformation on Perceived ESG Performance: The mediating role of green innovation. Sustainability, 15(8), 6568.

https://doi.org/10.3390/su15086568.

Xu, D., Huang, B., Shi, S., & Zhang, X. (2025). A Configurational Analysis of Green Development in Forestry Enterprises Based on the Technology–Organization–Environment (TOE) Framework. Forests, 16(5), 744.

https://doi.org/10.3390/f16050744.

Zhang, D., & Wang, G. (2024). The Sustainability Journey of Chinese Ready-Meal Companies Going Global: Configurational Analysis Using the Technology-Organization-Environment Framework. Foods, 13(14), 2251.

https://doi.org/10.3390/foods13142251.