- ABSTRACT:

- 1. INTRODUCTION

- 2. LITERATURE REVIEW

- 2.1. Theoretical Framework

- 2.2. Hypotheses Development

- 2.2.1. Hypothesis 1: Blockchain Adoption and GST Compliance

- 2.2.2. Hypothesis 2: Blockchain Adoption and Tax Filing Time

- 2.2.3. Hypotheses 3 and 4: Transaction Volume Error Rate and Filing Time

- 2.2.4. Hypothesis 5: IT Infrastructure and Compliance Error Rate

- 2.2.5. Hypothesis 6: IT Infrastructure and Filing Time

- 2.2.6. Hypothesis 7: Regulatory Environment and Compliance Error Rate

- 2.2.7. Hypothesis 8: Regulatory Environment and Filing Time

- 3. METHODS

- 4. RESULTS

- 5. DISCUSSION

- CONCLUSION & LIMITATIONS

- IMPLICATIONS

- LIST OF ABBREVIATIONS

- AUTHOR'S CONTRIBUTION

- ETHICAL STATEMENT & INFORMED CONSENT

- AVAILABILITY OF DATA AND MATERIALS

- FUNDING

- CONFLICT OF INTEREST

- ACKNOWLEDGEMENTS

- DECLARATION OF AI

- APPENDIX A

- REFERENCES

Blockchain as the Future of GST/VAT Compliance: Integrating Technology in Tax Compliance: Study from South Asia

PDF

PDF

1College of Business Administration, Imam Abdulrahman Bin Faisal University, Dammam, Saudi Arabia

Received: 28 December, 2025

Accepted: 28 March, 2026

Revised: 24 March, 2026

Published: 07 May, 2026

ABSTRACT:

Introduction: This study aimed to analyse the future of blockchain for GST compliance in South Asia. It focused on how the blockchain adoption status, transaction volume, IT infrastructure, and the regulatory environment affected GST compliance error rates and filing time.

Methods: This study used a primary quantitative survey design. It collected data from 375 respondents with a 5-point Likert scale. Survey participants included tax officials, GST officers, compliance managers, and IT administrators from various industries in South Asia. The analysis used Structural Equation Modelling (SEM) in SmartPLS.

Results: The study found that Blockchain Adoption Status was insignificantly but negatively related to Filing Time. However, it had a significant predictive relationship with the GST Compliance Error Rate, reducing compliance errors. Findings also showed a significant negative predictive relationship between IT Infrastructure and reduction in both Filing Time and GST Compliance Error Rate. The Regulatory Environment was significantly, but negatively, associated with Filing Time and the GST Compliance Error Rate. Transaction Volume was significantly associated with Filing Time and GST Compliance Error Rate.

Conclusion: The findings suggest that South Asian policymakers should design blockchain and digital tax reforms tailored to specific country capabilities. They should focus on interoperable systems, gradually include SMEs, and simplify regulations. Enhancing audit-trail requirements, improving digital readiness, and aligning cross-border GST processes would boost compliance accuracy and reduce filing risks in various administrative and economic settings.

Keywords: Blockchain adoption, GST/VAT compliance, filing time, transaction volume, IT infrastructure, regulatory environment, likert scale.

1. INTRODUCTION

The South Asian region faces challenges in strengthening its consumption-based systems, such as VAT and GST. These taxes are crucial but difficult to manage for compliance purposes. The VAT proportion in total tax revenue in the Asia-Pacific region is about 25.8% (OECD, 2025). Many South Asian states still struggle with poor tax mobilization, narrow tax bases, and weak compliance. These issues are caused mainly by systemic inefficiencies (Khan, 2015). These problems increase firms’ administrative costs. For example, in Pakistan, an average company spends around 594 hours per year on tax compliance, mostly on VAT-related tasks (Reva, 2015). India, Bangladesh, and Sri Lanka also face challenges with complex regulations, frequent regulatory changes, and reduced-rate frameworks, as noted by (Ghosh, 2022; and Harishekar & Manoj, 2021).

These systemic constraints result in significant compliance gaps. Pakistan also records an estimated annual fiscal loss of 5.8 trillion, or about 6.9% of GDP, due to under-reporting, non-filing, and evasion in consumption tax sectors (Abubakar et al., 2024). The ineffectiveness of VAT/GST regimes is also fostered by similar issues throughout the region, such as inadequate auditing capabilities and a large informal sector, as reported by (Haq, 2025). These long-term failures suggest that gradual administrative reform might be insufficient, as technology-facilitated change is needed.

(Setyowati et al., 2020; and Yayman, 2021) see distributed ledger technology, especially blockchain, as a solution for modernising VAT/GST systems. (Ashfaq et al., 2022; and Belahouaoui & Attak, 2024) argue that blockchain can reduce filing time, reduce human error, and improve audit efficiency through real-time transaction capture and automated cross-verification. However, there is little empirical research on the impact of blockchain on compliance outcomes in South Asia. The literature, including (Adelakun, 2024; and Carter et al., 2025), offers limited insights into its impact on error rates, filing efficiency, complexity, or regulatory limits in this region.

Although the literature on blockchain and digital tax systems is growing, gaps remain in South Asian research on GST/VAT compliance. No T-O-E-based empirical SEM study tests operational compliance outcomes in heterogeneous South Asian GST systems. First, methodological gaps remain; for example, studies such as (Ariyibi, 2024; and Khati et al., 2025) use literature reviews or secondary analyses, limiting empirical validation of blockchain’s effects on compliance errors and filing timing. Similarly, (AbuAkel & Ibrahim, 2023; and Mallick, 2021) employ surveys or macro-level ICT evaluations but lack robust causal or structural modelling. Thus, the relations between the volume of transactions, IT infrastructure, and the regulatory environment are poorly studied. Second, there are still some contextual deviations: the majority of the researches concentrate on separate nations (India, Kenya, Jordan, Nigeria) and do very little to address the heterogeneous economies, informal sectors and GST systems of South Asia. This discourages generalizability. Third, an adoption gap can be observed. Although there are insights that can be obtained through TAM, few studies incorporate blockchain-based elements, transaction volume, and firm characteristics to predict compliance. In a bid to fill these gaps, this paper relies on multi-method empirical data and SEM in order to identify those effects that are subtle and region-specific. The latest literature, including (Garg et al., 2023; and Gitema et al., 2025) focus on conceptual gains or adoption intentions. Not many studies quantitatively examine the impact of blockchain adoption, transaction volume, IT infrastructure and regulatory environment on compliance rates, error rates, and filing time. The systematic empirical research based on an integrative theoretical framework is the best way to fill this gap. Thus, the study is a Technology-Organization-Environment (T-O-E) model that is used to interpret survey data obtained by the researcher with tax professionals and compliance stakeholders in the chosen economies of South Asia. Additionally, a new institutional innovation, blockchain technology, has been investigated to support transparency and traceability, as well as mitigate the failure in coordination in government administration. According to (Khati et al., 2025), it has enhanced audit trails, reduced information asymmetry, automated compliance using smart contracts, and enhanced confidence in the regulatory environment, especially tax collection and municipal funding. Despite the more general applications of blockchain, there is still a controversy regarding its scalability, institutional preparedness, regulatory flexibility, and nonhomogeneous distribution among the emerging economies, as confirmed by (Iqbal et al., 2025). Various institutional and technological settings under GST regimes in South Asia generate empirical gaps in the impacts of blockchain operation, which are disjointed and poorly theorised. The present study is valuable in two aspects. To start with, the findings contribute to the existing body of knowledge on blockchain by creating a connection between institutional environment and compliance effectiveness. It is hoped that the study will contribute both theoretical and empirical information to the discussion about digital tax administration in South Asia. It employs quantitative techniques, e.g., surveys and structural equation modelling. Second, the research empirically deals with discussions on how well digital governance can be effective in developing areas through the analysis of technological preparedness and institutional environment. The remainder of this study is organized in the following way. This is the next part of the paper that presents the theoretical background and sets out the hypotheses that are based on the Technology-Organization-Environment model. This is then followed by the methodology section which gives the research design, the sampling method, data collection method and the method of analysis that would be applied to come up with the findings of this research study. Results and findings can be discussed in the next section, which interprets the results of the statistical findings and gives the empirical findings of this study. The discussion section then explains the findings in light of the theoretical framework and the previous literature. Lastly, the study ends with the conclusions, policy implications, limitations and future research directions.

2. LITERATURE REVIEW

2.1. Theoretical Framework

This study applies the Technology–Organization–Environment (T-O-E) framework as the theoretical basis, as it directly adheres to the constructs assessed in the study, such as blockchain adoption status, IT infrastructure, transaction volume, and regulatory environment, and elucidates that these dimensions form GST compliance outcomes. T-O-E’s technological environment focuses on the capabilities of systems and perceived usefulness, which justify the view that blockchain adoption is a determinant of efficiency and error reduction. The Technology-Organization-Environment (T-O-E) framework is utilized to describe how technological and institutional circumstances influence the GST compliance results. According to (Dandona et al., 2024), in the technological environment, blockchain implementation minimizes compliance mistakes by automation, instant validation, and unchangeable records maintenance, which restricts human intervention and post-filing corrections.

This saves clerical errors and delays in the reconciliation process, especially in situations where digital systems are effectively integrated (Owens & Hodžić, 2022). However, their effectiveness will be determined by the ease of use and the compatibility of the systems with existing tax systems (Wulandari & Dasman, 2023). In addition, (Abubakar et al., 2024) says that organizational context is the variance in the time of filing and accuracy of filing among companies. The availability of adequate IT system, trained personnel, and workflow alignment can assist in the processing of data more rapidly and submit it in a hassle-free manner. On the other hand, limited digital capability or physical approval lines amplify processing constraints especially when transaction volumes are very high as postulated by (AbuAkel & Ibrahim, 2023). (Taherdoost, 2022), on the other hand, pays significant attention to the fact that the performance outcome of technological innovations is an issue of organizational preparedness, and that technology will not consistently bring efficiency gain. The environment also moderates these relationships. Transparency, reduce interpretive uncertainty and mitigates compliance error, regulators impose work-increasing work, and hierarchy in reporting, and increase cognitive load of reporting thereby enhancing work, as reported by (Olabanji, 2023). The magnification of these moderating effects is greater in heterogenous South Asian tax administrations because enforcement strength, institutional maturity and SME dominance are all different. Consequently, reporting time may increase following large amounts of transactions in which the deficiency in technological and organizational readiness makes the issue, and the reduction of errors is an incidental attribute of regulatory consistency. The study via such causal pathways determines T-O-E as a two-way accountability framework founded on the mechanisms which articulate the association among the circumstances of the institution and the measurable performance in the terms of conformance. The technological capability will reduce the processing errors and delays in filing through automation, system testing and interoperability under the Technology-Organization-Environment framework (Anomah, 2024). Nonetheless, (Sidik, 2022) concludes that high number of transactions in a situation where the organization is not ready may increase the mental burden, complexity of the processes and verification requirements, which further increases the filing duration and error rate. These tensions become particularly acute in heterogeneous South Asian tax regimes, whereby the digital infrastructure, labour capabilities and regulatory focus outcomes are specified. Therefore, performance impacts are not only a consequence of technology adoption but are also influenced by the technology’s compatibility, the organizational environment, and the broader environmental context.

2.2. Hypotheses Development

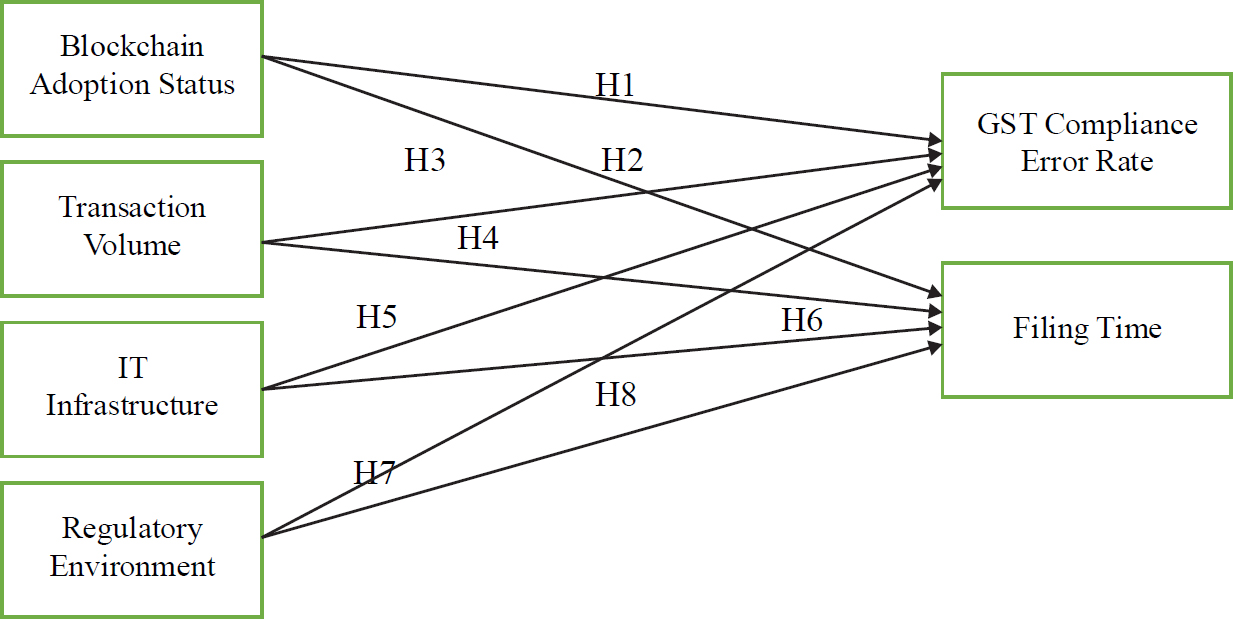

2.2.1. Hypothesis 1: Blockchain Adoption and GST Compliance

The immutable and traceable nature of blockchain data has been linked to fewer tax compliance errors since its adoption. According to (Ariyibi, 2024), blockchain can decrease the tax gap by 75-80% and compliance costs by 40-50%, demonstrating its high potential to reduce human-related filing errors. Nevertheless, their review-based approach is thorough but not empirically tested, which limits its capacity to attribute the decrease in error rates to the adoption of blockchains. Contrastingly, (Iqbal et al., 2025) provides a qualitative multiple-case study of five digitally advanced nations to offer a deeper contextual understanding of how blockchain can ensure transaction integrity and enhance timely, error-free reporting. Studies based on interviews provide valuable and detailed insights but are limited in their generalisability to larger sample populations. In the context of the T-O-E, the automation and transparency of blockchain technology enhance error-prevention measures, which validates the idea presented by (Adefunke & Mayowa, 2024) that the immutable structure of blockchain eliminates compliance misrepresentation. The technological and environmental aspects of T-O-E show why greater digital capacity and regulatory burdens jointly improve GST compliance in developing areas. These literature arguments lead to the formulation of the first hypothesis of the study, which is:

H1: Blockchain Adoption Status holds a statistically significant and negative relationship with the GST compliance error rate in South Asia.

2.2.2. Hypothesis 2: Blockchain Adoption and Tax Filing Time

The use of blockchain has been associated with reduced tax filing time through automated validation and real-time data synchronization. (Abubakar et al., 2024) emphasizes that tax systems that use blockchain technologies simplify reporting by automating record verification via smart contracts and shortening the filing process for SMEs. Nevertheless, their review design, although rich in concepts, lacks empirical evidence and therefore cannot accurately quantify time savings or draw causal conclusions. (Dagunduro et al., 2025), in turn, are more empirically grounded, having a large-scale survey and multivariate regression of the results that demonstrate that blockchain-based platforms would help increase the efficiency of filing and the entire revenue process by a significant margin. Even though such a practice may cause cross-country bias when using the self-reported data, the existing literature states that blockchain has the potential to streamline administrative processes. Efficiency of technologies and organizational readiness can be attributed to the decline in filing time in the T-O-E framework and the results of (Heinemann & Stiller, 2025; and Sidik, 2022) regarding the possibility of quickening compliance practices through automation and simplification of the workflow. These findings justify the assumption that the implementation of the blockchain will save a lot of time that is needed to submit the filing in new tax regimes. Therefore, based on these literature arguments, the following H2 of the study is formulated:

H2: Blockchain Adoption Status has a statistically significant and negative predictive association with the filing time in South Asia.

2.2.3. Hypotheses 3 and 4: Transaction Volume Error Rate and Filing Time

Recent research by (Kushwah et al., 2021) indicates that transaction volume has a substantial relationship with the rate of compliance errors and the time required for filing. Large volumes of transactions increase the burden of administrative and data-processing requirements, and this is more likely to lead to recording and reporting mistakes unless automated systems have been implemented, (Anomah, 2024). Moreover, (Kabwe & Van Zyl, 2021) observes that filing and positive revenue results are linked with the adoption of digital tax platforms, which are more efficient in managing large flows of transactions, which means that when the volume of transactions is high, it is the mediating roles of digitalization that facilitate a reduction in filing time as well as errors.

According to (Abubakar et al., 2024), increased volume of transactions in itself does not necessarily translate into a decreased number of compliance errors, and until organizations are ready, have technological infrastructure, and enforce it, more transactions can lead to greater inefficiencies. Correspondingly, (Iqbal et al., 2025) notes that the volume of transaction promote the adoption of e-filing by tax authorities, but the cross-sectional design does not allow one to infer causality. Similarly, with regards to the T-O-E viewpoint, the technological environment, including automation and system capacity, interacts with organizational ones, including process maturity and staffing, and the environmental one, including regulatory supervision and enforcement measures, determines the compliance outcomes. This model gives the reason why, in itself, transaction volume may not result in fewer errors in GST or shorter-filing time: without IT infrastructure, willing staff, and facilitating regulations, more volume may saturate systems and cause more error. The combination of the study’s results to H3 and H4 and the need to have region specific, empirical studies in South Asia.

H3: Transaction Volume is statistically significantly and positively related to the GST compliance error rate in South Asia

H4: Transaction Volume is statistically significantly and positively associated with the filing time in South Asia

2.2.4. Hypothesis 5: IT Infrastructure and Compliance Error Rate

IT infrastructure will be important in a digital-first tax regime to determine the accuracy of GST compliance. Technological obstacles that result in an inability to file, as (Kumar & Gokhru, 2025) demonstrate, are system downtime, slow portal, and the absence of digital support, which are also some of the reasons why Indian taxpayers tend to commit errors. Their behavioural analysis indicates that, despite simplified processes and transparency, poor IT backbones negate the benefits. Their sample of 100 taxpayers is, however, small, which limits generalisability and limits the study’s capacity to represent a variation between sectors or different intensities of transactions. (Khati et al., 2025) points out that blockchain-based IT infrastructures are able to optimize and increase compliance accuracy by means of real-time validation, traceability, and smooth data sharing. The fact that they use a secondary research design restricts their ability to validate empirically, however, weakening their confidence in their capacity to measure error reduction attributable to IT improvements. The T-O-E framework, technological dimension system capabilities, reliability, and automation interrelate with organizational preparedness, including staff competence and process integration, to affect the results of GST compliance. Regulatory oversight is another environmental pressure that also conditions the effectiveness of IT infrastructure, as suggested by (Anomah, 2024). Although previous research, including (Othman & Yusuff, 2022), argues that a well-developed IT infrastructure increases the system’s reliability and minimizes errors, these data are based mostly on conceptual or cross-sectional evidence. Different levels of digital maturity and regulatory enforcement in the South Asian context require an empirical study to prove these relationships. This study, therefore, guides and considers the influence of the IT infrastructure on the development of the GST compliance accuracy. Based on arguments merging from the review of studies, the fifth hypothesis of the study is formulated.

H5: IT Infrastructure is statistically significantly and negatively related to the GST compliance error rate in South Asia

2.2.5. Hypothesis 6: IT Infrastructure and Filing Time

IT infrastructure has generally been considered one of the determinants of tax filing efficiency, but its impact is context-dependent. (AbuAkel & Ibrahim, 2023) discovered that strong IT systems that are supported by management and the perceived relative advantages can greatly improve e-filing adoption and help to save time on filing in Jordan. Their analysis, based on the T-O-E framework and Smart PLS, with 315 respondents, provides a convincing argument that the mechanisms operate through trust in the system. Its focus on emerging economies and its survey-based design, however, restrict its generalisability to bigger and more heterogeneous taxpayer groups. Conversely, (Mallick, 2021) indicates that ICT infrastructure in India had a negligible effect on the tax collection, with informal economic activity or high transaction volume having the potential to reduce the effectiveness of ICT in accelerating the speed at which the tax is filed. Although the author’s longitudinal analysis gives a wider macro-level approach, it is incapable of isolating behavioural or organizational causes of adoption. In terms of the T-O-E framework, these results suggest that IT infrastructure can only lower the time spent in filing, when perceived as useful, reliable and easy to use, and it is important to note that complementary organizational and governance support is necessary to convert the increase capacity into an efficiency increment. Grounded on these literature arguments, the following hypotheses of the study H6 are developed;

H6: IT Infrastructure is statistically significantly and negatively associated with filing time in South Asia

2.2.6. Hypothesis 7: Regulatory Environment and Compliance Error Rate

The regulatory frameworks play a critical role in determining the level of compliance with GST and determining the errors, as well as how the taxpayer behaves. (Sureka & Bordoloi, 2024) emphasizes that the blocked input tax credit (ITC) and the complicated provisions in the GST regime of India make the operation of the MSMEs a burden and increase compliance failure. Their mixed-methods methodology, which surveys 400 MSMEs and supplements it with qualitative data, offers detailed insights into industry-specific problems, but the use of self-reported financial impacts may be biased and reduce extrapolability. (Gitema et al., 2025) also investigated the effects of the legislation reforms in turnover tax compliance among small traders in Kenya, and the researchers found that the regulatory clarity and compliance are strongly related. Their survey design, which is explanatory, offers good inferential evidence (β = 0.286, p = 0.000), but it is small in terms of geography and may not be able to explain the bigger institutional differences. Within the frames of the T-O-E framework, the findings of (Gitema et al., 2025) imply that the environment dimension, including legislative transparency, enforcement systems and systemic complexity influence the organizational and technological preparedness and adjusts the error rates. Development of well-structured regulations, the one (AbuAkel & Ibrahim, 2023) promotes in India and Kenya, makes cognitive load and errors in compliance less. Based on these arguments, H7 of the study was formed:

H7: Regulatory Environment is statistically significantly and negatively related to the GST compliance error rate in South Asia

2.2.7. Hypothesis 8: Regulatory Environment and Filing Time

The regulatory climate has a significant effect on efficiency in tax filing, and it predetermines the procedural clarity, the standards of reporting, and institutional support. On the one hand, because the GST provisions are challenging, and the input tax credit is withheld, the time spent in filling compliance with vague regulations is time-demanding in India (Sureka & Bordoloi, 2024). On the contrary, (Gitema et al., 2025) show that effective legislative changes in Kenya improve turnover tax filing delays by a significant margin, which indicates that regulatory simplicity and predictability result in efficiency. In line with this, (Mallick, 2021) concludes that ICT integration and the quality of governance can moderate procedural delays, but their effect is weakened in the case of inconsistent regulatory frameworks. (AbuAkel & Ibrahim, 2023) demonstrates that adoption of e-filing depends on the presence of adequate IT infrastructure and support from the top management, as it is clear that technological and organizational preparedness mitigates the impact of regulatory design to decrease filing time. It is also supported by the T-O-E framework that the model, the environmental aspect, transparent rules and institutional support determine the manner in which organizations use technology to gain effective compliance. Supported by the arguments of these studies, the following hypothesis, H8, of the study is formulated. Further, based on these literature arguments and identified literature gaps, the conceptual framework of this study is proposed in Fig. (1).

H8: Regulatory Environment holds a statistically significant and negative predictive relationship with the filing time in South Asia.

Fig. (1). Conceptual model.

3. METHODS

The data for the current study were gathered through a structured survey questionnaire, which included close ended questions aimed at scoring the research constructs of blockchain adoption status, volume of transactions, IT infrastructure, regulatory environment, GST compliance error rate and time of filing, as shown in Appendix A. All the constructs were operationalized using a variety of items that were measured using a five-point Likert scale, which is standard practice in behavioural and technology-oriented research, as advised by (Russo et al., 2021). The research population comprised mostly tax officials, GST officers, compliance managers and financial administrators in South Asia, which was in line with the study topic, which emphasized technology-based tax compliance.

Blockchain Adoption Status has been conceptualized as implementation intensity, which is a measure of organizational integration as opposed to binary adoption. The construct operationalizes the degree of operationally embedded blockchain systems based on active utilization, staff training and or workflow alignment. The strategy redefines adoption as maturity, as performance impacts are found in the depth of integration rather than in the presence of technology. Introduction of implementation intensity, therefore, is a better measure of organizational digital transformation in tax administration situations.

Moreover, Regulatory Environment is a reflective, higher-level construct that encompasses perceived regulatory clarity, policy stability, and institutional support as dimensions of perceived regulatory quality, all of which are interrelated. These indicators are expected to covary, as they are manifestations of a regulatory context rather than separate elements. The construct as a reflective guarantee that change in regulatory perception is always reflected across the items without compromising measurement in the structural model.

G*Power 3.1 was used to estimate the sample size, small-to-medium effect size (f2 = 0.05), the significance level of 0.05, desirable statistical power of 0.95, and several predictors in the regression model. The analysis showed a minimum required sample size of 375 respondents. The resulting sample size of 375 is larger than the standard 10-times rule in PLS-SEM, which states that a minimum of 10 times the maximum number of structural paths to a latent construct is needed. The maximum number of predictors in this model is four, which means the minimum requirement is considerably lower than the achieved sample size. Also, the results of power analysis indicate that the sample size meets the minimum statistical power at a level of 0.80 with a medium effect size, which represents a sufficient statistical power to estimate the structural model. In order to attain this, 600 respondents were reached out to using LinkedIn, official social media pages of tax-related agencies and professional networks. It had a response rate of 65% (390 responses), which was satisfactory for an online professional survey. Furthermore, data cleaning was performed by identifying multivariate outliers using the Mahalanobis distance method proposed by (Ariyibi, 2024). The critical chi-square cutoff was determined based on the number of observed variables at the significance level of p = 0.001. Reactions exceeding this threshold were classified as outliers, and 9 cases were eliminated. After the exclusion, the data that remained valid was 375 responses. To ensure that it is robust, the major model estimates were re-estimated with outliers indicated by the results and no significant changes in levels of significance or path coefficients were found and thus it guaranteed the stability and reliability of the result to conduct PLS-SEM. The non-probability purposive sampling technique was used in using professional networks because the study was targeting those people who had a first-hand experience on tax administration and compliance to GST. This method facilitated the deliberate hiring of efficient professionals who could offer context-specific information that is based on knowledge. (Garg et al., 2023) suggests that purposive sampling is appropriate when the objective of the study is to come up with expertise-based evidence instead of an effort to represent the whole population. Along similar lines, according to (Tajik et al., 2024), research involving professional views ought to use structured sampling of knowledgeable respondents rather than general population sampling. This strategy, therefore, meant that the respondents had the pertinent institutional and operational knowledge to investigate the effects of blockchain adoption and compliance. Further, the respondent pool diversification was also ensured through various countries, sectors, and institutional positions to further enhance reliability and external validity of the results, whereby the outcomes represent a holistic approach to GST/VAT compliance practises in South Asia. Purposive sampling was used to focus on professionals interested in GST/VAT compliance across several countries, sectors, and institutional positions. Since the South Asian region is large and heterogeneous, the sample provides representative professional information in the context of the survey, including participants’ practices and views. Consequently, the results are considered adequate representations of the professional experiences documented in the research, although they are not applicable to all firms and tax authorities across the region. Moreover, the survey data collection process also leads to the issue of non-response bias. Hence, the assessment of non-response bias was conducted by comparing early and late respondents (n1 = 75 and n2 = 75, respectively) using (AboAlsamh, 2025) approach, as no significant differences in the key variables were identified.

The study identified the following ethical considerations for primary data collection involving external respondents. For instance, the study was voluntary, and the respondents were free to withdraw at any point without repercussions. De-identification of all survey responses and data storage were employed to ensure that the concepts of confidentiality and anonymity were upheld. The study received ethical approval from the respective institutional review board and guaranteed that the research conducted was both professionally ethical and that the rights, privacy and well-being of all the respondents in the survey were not violated.

Partial Least Squares Structural Equation Modelling (PLS-SEM) was analysed as it is suitable when conducting a predictive investigation and a complex model with both formative and reflective constructs. As suggested by (Haji-Othman & Yusuff, 2022) a Measurement Model Assessment was conducted in the first instance to determine reliability and validity. Cronbach’s alpha (Composite Reliability, CR) was used to assess internal consistency, and Average Variance Extracted (AVE) was used to assess convergent validity, per the thresholds recommended by (Mohd Dzin & Lay, 2021). The measurement model was proved to be valid and reliable, path analysis of PLS-SEM was performed in order to test the hypothesised relationships between variables in a causal way, which is universally supported in the research of technology adoption and taxes compliance.

4. RESULTS

4.1. Demographics Analysis

The statistical results indicated in Table 1 signifies the demographic characteristics of participants of the study. The results show that among (n = 375) participants, 56% were males and 44% and 32% were between 35-40 years old and 28% were 40-45 years old. While minimal percentage that is 18.67% represented age groups 35-35 years. Moreover, among these participants, 27.20% were tax managers, 22.40% were compliance officers, 22.67% were IT system administrators, and 27.73% were business owners. Also, 21.33% and 34.67% of these participants represented the retail and technology industries, respectively, while 17.33% represented the manufacturing industry and 26.67% represented the services industry. Lastly, 18.67% among entire study population, worked in finance departments, 32% in accounting departments, 25.53% in IT and, 24.80% worked in operations departments.

Table 1. Demographic analysis.

| Demographic Category | Frequency (n) | Percentage (%) | |

| Gender | Male | 210 | 56.00% |

| Female | 165 | 44.00% | |

| Age Range | 30-35 | 70 | 18.67% |

| 35-40 | 120 | 32.00% | |

| 40-45 | 108 | 28.80% | |

| 45-50 | 77 | 20.53% | |

| Participant Role / Occupation | Tax Manager | 102 | 27.20% |

| Compliance Officer | 84 | 22.40% | |

| IT systems Administrators | 85 | 22.67% | |

| Business Owners | 104 | 27.73% | |

| Department | Finance | 70 | 18.67% |

| Accounting | 120 | 32.00% | |

| IT | 92 | 24.53% | |

| Operations | 93 | 24.80% | |

| Industry Type | Manufacturing | 65 | 17.33% |

| Retail/Wholesale | 80 | 21.33% | |

| IT/Technology | 130 | 34.67% | |

| Services | 100 | 26.67% | |

4.2. Measurement Model Assessment

The measurement model is analysed for validity and reliability using Cronbach’s alpha and Composite Reliability against threshold value of 0.7 and average variance extracted (AVE) with 0.5 threshold as suggested by (Mohd Dzin & Lay, 2021). The results of measurement model are labelled in Table 2.

Table 2. Measurement model assessment.

| Latent Variables | Indicators | Factor Loadings | Cronbach’s Alpha | Composite Reliability | Average Variance Extracted |

| Blockchain Adoption Status | BAS1 | 0.883 | 0.852 | 0.857 | 0.771 |

| BAS2 | 0.905 | ||||

| BAS3 | 0.846 | ||||

| Filing Time | FT1 | 0.862 | 0.857 | 0.857 | 0.777 |

| FT2 | 0.903 | ||||

| FT3 | 0.880 | ||||

| GST Compliance Error Rate | GSTCER1 | 0.910 | 0.894 | 0.904 | 0.824 |

| GSTCER2 | 0.933 | ||||

| GSTCER3 | 0.881 | ||||

| IT Infrastructure | ITI1 | 0.894 | 0.885 | 0.885 | 0.813 |

| ITI2 | 0.926 | ||||

| ITI3 | 0.885 | ||||

| Regulatory Environment | RE1 | 0.907 | 0.902 | 0.904 | 0.836 |

| RE2 | 0.935 | ||||

| RE3 | 0.900 | ||||

| Transaction Volume | TV1 | 0.821 | 0.815 | 0.822 | 0.730 |

| TV2 | 0.904 | ||||

| TV3 | 0.837 |

As results depicted in Table 2, all constructs exhibited adequate psychometric properties. Blockchain Adoption Status demonstrated loadings ranging between 0.846 and 0.905, Cronbach alpha (0.852) and CR (0.857) with values that are greater than 0.70 established a high level of convergent validity, whereas its AVE (0.771) affirmed high convergent validity. There were also strong loadings observed in Filing Time (0.862-0.903), with an = of 0.857 and an AVE of 0.777, relative to the threshold of 0.5, indicating appropriate internal consistency. A high convergence (0.881-0.933), a = 0.894 and AVE = 0.824 were appropriate indicators that GST Compliance Error Rate had high item reliability. Similarly, there were high loadings of IT Infrastructure (0.885-0.926) with = 0.885 and AVE = 0.813. The Regulatory Environment had high reliability (a = 0.902), loadings of 0.900-0.935, and an AVE of 0.836. Finally, the reliability of Transaction volume was acceptable (a = 0.815) and AVE = 0.73. Altogether, all constructs satisfied the recommended criteria, thereby demonstrating a valid and reliable measurement model.

4.3. Collinearity Diagnostics-Variance Inflation Factor

To address the common method bias, Variance Inflation Factor (VIF) is used to assess multicollinearity. The VIF values were analysed and results in Table 3 exhibits the values range between 1.426 and 2.190 which is lower than threshold value of 5. It indicates there is no multicollinearity in the model which validates that common method bias is improbable to meaningfully misrepresent the findings.

Table 3. Variance inflation factor.

| – | VIF |

| Blockchain Adoption Status -> Filing Time | 1.887 |

| Blockchain Adoption Status -> GST Compliance Error Rate | 1.887 |

| IT Infrastructure -> Filing Time | 2.190 |

| IT Infrastructure -> GST Compliance Error Rate | 2.190 |

| Regulatory Environment -> Filing Time | 1.831 |

| Regulatory Environment -> GST Compliance Error Rate | 1.831 |

| Transaction Volume -> Filing Time | 1.426 |

| Transaction Volume -> GST Compliance Error Rate | 1.426 |

4.4. Discriminant Validity

The results of discriminant validity are examined using Heterotrait-Monotrait Ratio (HTMT) ratio which allows to analyse conceptual overlapping, and distinctiveness among variables of the study to avoid issues of multicollinearity against the threshold value of 0.8, supported by (Haji-Othman & Yusuff, 2022) as well. The results of HTMT ratio are specified in Table 4.

Table 4. Discriminant validity.

| – | HTMT |

| Filing Time <-> Blockchain Adoption Status | 0.320 |

| GST Compliance Error Rate <-> Blockchain Adoption Status | 0.285 |

| GST Compliance Error Rate <-> Filing Time | 0.432 |

| IT Infrastructure <-> Blockchain Adoption Status | 0.534 |

| IT Infrastructure <-> Filing Time | 0.512 |

| IT Infrastructure <-> GST Compliance Error Rate | 0.499 |

| Regulatory Environment <-> Blockchain Adoption Status | 0.607 |

| Regulatory Environment <-> Filing Time | 0.529 |

| Regulatory Environment <-> GST Compliance Error Rate | 0.482 |

| Regulatory Environment <-> IT Infrastructure | 0.351 |

| Transaction Volume <-> Blockchain Adoption Status | 0.542 |

| Transaction Volume <-> Filing Time | 0.415 |

| Transaction Volume <-> GST Compliance Error Rate | 0.347 |

| Transaction Volume <-> IT Infrastructure | 0.546 |

| Transaction Volume <-> Regulatory Environment | 0.464 |

The findings of the discriminant validity, determined with the help of the criterion of HTMT, show that all the constructs within the model are conceptually different with no overlapping, Table 4. All HTMT values were below the conservative value of 0.85 which confirms that there is adequate discriminant validity with no conceptual overlapping among the constructs an validates distinctiveness among them.

4.5. Path Coefficient

Table 5 show the path coefficient results which indicate a combination of significant and insignificant relationships. Blockchain Adoption Status has a negative but marginally significant predictive association with Filing Time (β = -0.134, p = 0.057) at 10% CI. Nevertheless, its association with GST Compliance Error Rate is significant (β = -0.150, p = 0.048), indicating that increasing blockchain adoption will lead to a substantial decrease in compliance errors, even though it will not result in a significant reduction in filing time.

Table 5. Path coefficient.

| – | Path Coefficients | T Statistics | P Values |

| Blockchain Adoption Status -> Filing Time | -0.134* | 1.900 | 0.057 |

| Blockchain Adoption Status -> GST Compliance Error Rate | -0.150** | 1.974 | 0.048 |

| IT Infrastructure -> Filing Time | -0.251*** | 3.325 | 0.001 |

| IT Infrastructure -> GST Compliance Error Rate | -0.309*** | 3.785 | 0.000 |

| Regulatory Environment -> Filing Time | -0.301*** | 3.514 | 0.000 |

| Regulatory Environment -> GST Compliance Error Rate | -0.265*** | 3.045 | 0.002 |

| Transaction Volume -> Filing Time | 0.180*** | 2.755 | 0.006 |

| Transaction Volume -> GST Compliance Error Rate | 0.127* | 1.775 | 0.076 |

Note: *: Significance at 10%; **: Significance at 5%; ***: Significance at 1%

There are significant negative results of IT Infrastructure on Filing Time (β = -0.251, p = 0.001) and GST Compliance Error Rate (β = -0.309, p = 0.000). These findings validate that strong technological capability improves the filing efficiency and minimises the errors caused by compliance.

Likewise, the Regulatory Environment has a notable relationship with filing time in terms of on reducing the it (β = -0.301, p = 0.000) and GST Compliance Error Rate (β = -0.265, p = 0.002) with the implication that more supportive and understandable regulatory environments speed up and decrease the error rate of the GST-related processes.

Transaction Volume has a significant predictive relationship with Filing Time (β = 0.180, p = 0.006) but marginally significant association with GST Compliance Error Rate (β = 0.127, p = 0.076) at 10% CI. This shows that an increase in transaction loads improves the rate of filing activities but it does not have a systematic effect on compliance error. On the whole, IT infrastructure and the regulatory environment are the most significant predictors of efficiency and accuracy, and the reduction in errors is also associated with the adoption of blockchain.

4.6. Model Explanatory Power

The model’s explanatory power is examined using R-square and adjusted R-square values, which indicate the predictive power of the independent variables for variation in the target variables. The results are specified in Table 6.

Table 6. Explanatory power.

| – | R-Square | R-Square Adjusted |

| Filing Time | 0.278 | 0.271 |

| GST Compliance Error Rate | 0.255 | 0.247 |

The results of explanatory power in Table 6, indicates that 27.8% variation in filing time and 25.5% variation in GST compliance in error rate can be predicted by blockchain adoption status, transaction volume, IT infrastructure, and regulatory environment.

5. DISCUSSION

The study’s findings show that adopting blockchain reduces GST compliance errors to a large extent, thereby supporting H1. This indicates that the accuracy of transactions is enhanced by the transparency, immutability, and automated validation inherent in blockchain among South Asian firms. The results highlight the fact that technological benefits are contingent on organisational preparedness and institutional fit as opposed to the infrastructural factor. In the T-O-E model, technological capability is influenced by the system reliability and automation, and effective utilisation depends on the skills of the workforce, clarity of the procedures, and the support of the managers argued by (AboAlsamh, 2025) also. Other conditions that condition outcomes include the clarity of regulations and industry customs indicated by (Adelakun, 2024) also. Theoretically, this highlights interaction effects between T-O-E dimensions, and practically, coordinated capacity building towards successful implementation. Inequality in institutional backing and culture based on manual countercheck may qualify the effect of blockchain on reduction of errors in South Asia. Therefore, T-O-E does not only describe the adoption but enablers, contextual to blockchain so that it works well in enhancing compliance outcomes.

The results also exhibit marginally significant relationship between Blockchain adoption status and tax filing time which marginally accepts H2 of this study. The fact that there is no significant correlation between the application of blockchain and the timing of filing implies that the use of blockchain is not necessarily the driver of the changes in efficiency in the South Asian GST systems. Based on the T-O-E, this inference means that the potential of the technological aspect should be enabled by the organisational dispensability and standardisation with environment to be translated into the operational shifts. However, automation and interoperability are benefits of blockchain, which are limited to time-saving by the fragmented administrative systems and verification. According to (Ariyibi, 2024), the efficiency gains need to be systemic redesigned and not just switched to digital. The effective utilisation is mediated by organisational factors like firm size; optimisation of workflow and digital competence of employees (Wulandari & Dasman, 2023) and institutional preparedness affects the success of the implementation. Additional outcomes are determined by environmental conditions, such as regulatory clarity. According to (AboAlsamh, 2025), perceived usefulness and system simplicity increase engagement, yet these components are absent in heterogeneous South Asian contexts. Therefore, blockchain in itself cannot take place without structure and institutional harmonisation.

The findings reveal that the level of transaction volume is marginally significant factor influencing the level of GST compliance errors, which constitutes that H3 is accepted marginally. The insignificant predictive association amid transaction volume and compliance error rate reveals that workload is not the sole factor that defines the presence of the error in the South Asian GST systems. T-O-E perspective shows that transaction intensity could be countered with technological reliability and automation coupled with organisational capacity to reduce the accuracy of compliance. In this perspective (Dagunduro et al., 2025; Khati et al., 2025) also indicates that automated systems can lessen volume-related mistakes in case sufficient infrastructure and training are in place but may be undermined by the lack of resources. (Iqbal et al., 2025) also affirm that the operational pressures of moderates are moderated by the integration of the system. Facts presented by (Wulandari & Dasman, 2023) demonstrate that better-prepared companies can remain accurate even as their transaction rates rise. Therefore, theory posits that results are determined by structure preparedness, and not volume, meaning that policy emphasis needs to be redirected to solidifying technological and organisational capacity instead of limiting the size of transactions.

The results affirm that H4 is also accepted, the transaction volume can considerably increase the filing time. A higher volume of transactions leads to a processing bottleneck, requiring more verification and approvals, especially in companies with limited IT capacity. As noted by (Mallick, 2021), strict reporting requirements is a slowing factor in filing in emerging economies, and (AbuAkel & Ibrahim, 2023) also found that automation might not have a full counteracting effect. Within the framework of T-O-E, the technological environment system ease of use and reliability influences the perceived ease of filing (PEOU), organisational environment IT infrastructure, workflow design, firm size influences behavioural intention (BI) to file on time and the environmental environment; regulatory demands, hierarchical approvals also influence compliance behaviour proposed by (Khati et al., 2025). For practice, these findings imply that the integration of the technological capacity, organisational preparedness, and favourable institutional environments over volume is a determinant of filing efficiency in South Asia with high transaction volumes.

The research results in that IT infrastructure can greatly minimise GST compliance errors, and H5 is confirmed. Human error is reduced through reliable IT systems to enhance validation and tracking as well as transparency. (Kumar & Gokhru, 2025) also focused on the fact that the compliance can be more precise due to the use of the digital infrastructure, and (Khati et al., 2025) also pointed out the fact that the use of blockchain-based platforms ensures the traceability and minimises the errors. The benefits in South Asia are tamed by the shortage of IT resources and uneven digital literacy patterns especially among the SMEs. The results demonstrate that compliance performance is determined by technological, organisational and environmental dimensions in T-O-E model. The enabling factors to apply the technological capability efficiently that reduces the vulnerability to making errors are the technological capability gained via system stability and usability, and organisational preparedness, in terms of skills, infrastructure and support management. The environmental conditions (regulatory practices) moderate these effects. Manufacturing and energy are industries with a higher degree of structural maturity, so they can be more efficient in compliance, which contributes to the contextual interaction of the theoretical assumptions made by (Olabanji, 2023; and Wulandari & Dasman, 2023).

The results show that IT infrastructure substantially reduced filing time, supporting H6. Effective systems facilitate data entry, verification, and submission. (AbuAkel & Ibrahim, 2023) stated that integrated platforms improve e-filing adoption and efficiency, whereas (Dagunduro et al., 2025) highlighted the importance of automation for timely reporting. South Asia is characterised by the lack of homogenous infrastructure and uneven adoption of efficiency gains, especially in the case of SMEs. The perception of technologies as intuitive and effective increases behavioural intention to adopt blockchain-enabled systems in South Asia and is a reflection of the technological and organisational environment of the T-O-E framework argued by (Kumar & Gokhru, 2025) as well. The complexity of the workflow is also industry-specific, with (Taherdoost, 2022) indicating that hierarchical approvals and the requirement of manual checks moderate the speed and efficiency of filing, which is further influenced by technological, organisational, and environmental determinants in terms of compliance. The results imply that the use of scalable IT systems, along with employee education and workflow standardisation, is required to achieve the highest level of files in South Asian companies, which proves the interaction of IT preparedness with the users and the specific environment of the company to define the speed of compliance.

The findings confirm the acceptance of H7 by showing that a conducive regulatory environment greatly minimises the loss of compliance through errors in GST. Correct reporting is achieved through clear, consistent rules and enforcement. (Sureka & Bordoloi, 2024) noted that simplified GST provisions increase compliance among MSMEs, and (Gitema et al., 2025) also highlighted the significance of legislative clarity for the tax compliance of the small. South Asians face numerous regulatory changes, lax oversight, and complex reporting requirements, all of which pose significant compliance challenges. According to the T-O-E framework, clarity and ability to understand rules can increase the perceived usefulness of digital GST filing systems and promote interaction with these systems, which is why compliance errors become less frequent suggested by (Olabanji, 2023) also. For theory and practice, the findings imply that companies that have internal compliance departments can more easily overcome the requirements, but SMEs with less technological and organisational capacity must struggle more, and the impact of technological, organisational, and environmental factors is pivotal in defining the outcome of compliance.

Supportive and transparent regulations have a significant effect on reducing filing time, according to the results, which supports H8. Clear policies and standardised application of these policies minimise submission delays. (Gitema et al., 2025) observed that efficiency is boosted by clarity, and (Sureka & Bordoloi, 2024) noted that simplified procedures enhance MSME filing performance. These findings are frequent, but not uniform across the region; and the requirements of the reporting system in South Asia are cumbersome and slow down the filing process of small companies argued by (Khati et al., 2025). The clarity and usability of regulations in the T-O-E framework improve the technological and organisational readiness to advance behavioural involvement with GST systems. The regulatory requirements intersect with firm-level variables, including IT infrastructure and transaction volume, to determine filing efficiency. For practical application, this implies that successful implementation and saving time depends not only on the usability of the system but also on the conducive organisational systems and control environments. Hierarchical approvals are also culturally dependent on the speed of filing. These findings suggest that cohesive regulations, unified digital services, and learning programmes would be needed to enhance the efficiency of submissions, ensuring compliance and suitability rates comparable to those of South Asian businesses in terms of accuracy and usability.

CONCLUSION & LIMITATIONS

The study has revealed that blockchain, IT infrastructure, GST transaction management, and a friendly regulatory environment will change GST compliance reasonably in South Asia. The impact of the blockchain on the time of filing is not as substantial as the compliance errors are reduced to the minimum however, the effect of the blockchain is constrained by the procedures and the infrastructural limitations, meaning that the technology is not a sufficient requirement. Organisational readiness and digital literacy in its effect makes transaction volume the key in establishing weaknesses in errors and effectiveness of filing particularly when the smaller role of organisational readiness and digital literacy is considered. IT infrastructure turns out to be a facilitator with a centre stage as it sharpens precision and frequency and regulatory clarity defines behavioural participation and uptake among companies. This research fits perfectly well with the T-O-E framework, as it empirically establishes the interaction of three environments, including technological, organisational, and environmental to stipulate the influence of three on the GST compliance in South Asia. The findings indicate that blockchain application and IT infrastructure have the potential to enhance the reduction of errors and filing efficiency. Having added industry specific variables like regulatory environment and IT infrastructure, contextual contingencies of technology adoption is identified in the study whereby T-O-E will dynamically construct to affect compliance behaviour thereby adding to the improved usefulness of the framework to practical use. Moreover, the limitation of this study is that the study is a cross-sectional survey study, and thus it does not allow us to make time-related causal inferences and it also does not represent the trends of technology adoption in South Asia. This may result in response bias when using self-reported information on taxes authorities and make generalisation to the rest of the economy difficult through focus on a few industries. Based on the cross-sectional research design and the reliance on self-reported Likert-scale measures of the independent and dependent variables, this research is vulnerable to the problems, including concerns of simultaneous nature. The contextual factors such as the culture of the firm, digital literacy, and regional regulations differences were also not properly investigated. The future research can employ longitudinal designs, address the multiple perspectives of the stakeholders, and address sector- or nation-specificities. The hybrid technologies, AI integration and behavioural interventions can be introduced to provide further opportunity to optimize the efficiency and effectiveness of the GST compliance. Furthermore, despite the rigidity of the structural model, the study relies on cross-sectional self-reported information, also rendering it vulnerable to the common method bias and simultaneity concerns. Although statistical checks such as full collinearity evaluation have been done to reduce bias. The research in the future is thus proposed to use longitudinal or multi-source data to help strengthen extrapolation validity.

IMPLICATIONS

The paper notes that policymakers and regulators in South Asia can concentrate on the integration of blockchain and effective IT infrastructure in enhancing the accuracy and efficiency of GST compliance. The ambiguity shall be minimised in order to ensure simplicity, harmony and consistency in execution of regulatory systems, and they shall be filed as soon as possible. The capacity-building aspect should be taken into account to maximise the utilisation of the technology, which entails training on digital literacy and dedicated assistance of the SMEs. The policymakers should also promote scalable user-friendly digital platforms that have the capacity to facilitate high volumes of transactions. Also, concerning the theoretical implications, the study makes certain contributions to the T-O-E framework because it has been empirically established that the interaction of technological preparedness, organisational readiness and regulatory settings not only affect the results of compliance with GST in heterogeneous settings but also in South Asia. It focuses on the fact that the consequences of digital adoption are not automatic. In practice, organisations are recommended to work on improving IT infrastructure, personnel digital competence, and getting workflow reconciliation to derive as much out of blockchain systems. The policymakers must develop regulatory sceneries that would augment the technological investments by being simple, unified, and digitally interoperable.

LIST OF ABBREVIATIONS

AVE | = | Average Variance Extracted |

BI | = | Behavioural Intention |

CR |

| Composite Reliability |

HTMT | = | Heterotrait-Monotrait Ratio |

PEOU | = | Perceived Ease Of Filing |

PLS-SEM |

| Partial Least Squares Structural Equation Modelling |

SEM | = | Structural Equation Modelling |

T-O-E | = | Technology-Organization-Environment |

VIF | = | Variance Inflation Factor |

AUTHOR’S CONTRIBUTION

I.M. has contributed to conceptualization, idea generation, problem statement, methodology, results analysis, results interpretation.

ETHICAL STATEMENT & INFORMED CONSENT

The study identified the following ethical considerations for primary data collection involving external respondents. For instance, the study was voluntary, and the respondents were free to withdraw at any point without repercussions. De-identification of all survey responses and data storage were employed to ensure that the concepts of confidentiality and anonymity were upheld. The study received ethical approval from the respective institutional review board and guaranteed that the research conducted was both professionally ethical and that the rights, privacy and well-being of all the respondents in the survey were not violated.

AVAILABILITY OF DATA AND MATERIALS

The data will be made available on reasonable request by contacting the corresponding author [I.M.].

FUNDING

None.

CONFLICT OF INTEREST

The author declares no conflicts of interest, financial or otherwise.

ACKNOWLEDGEMENTS

Declared none.

DECLARATION OF AI

During the preparation of this manuscript, the author used ChatGPT for language polishing. After utilizing this tool, the author carefully reviewed and refined the content as necessary and accept full responsibility for the accuracy and integrity of the published work.

APPENDIX A

Demographic

| Demographic Factor | Options |

| Age | ☐ 30-35 |

| ☐ 35-40 | |

| ☐ 40-45 | |

| ☐ 45-50 | |

| Gender | ☐ Male |

| ☐ Female | |

| Participant Role / Occupation | ☐ Tax Manager |

| ☐ Compliance Officer | |

| ☐ IT Systems Administrator | |

| ☐ Business Owner | |

| Industry Type | ☐ Manufacturing |

| ☐ Retail/Wholesale | |

| ☐ IT/Technology | |

| ☐ Services |

Survey Questionnaire

| Construct | Survey Items | SD | D | N | A | SA |

| Blockchain Adoption Status | Our organisation has implemented blockchain technology for recording and verifying GST/VAT transactions. | |||||

| Blockchain systems are actively used in our transaction verification processes. | ||||||

| Employees are trained and familiar with blockchain-based tax compliance systems. | ||||||

| Transaction Volume | The number of GST/VAT transactions processed by our organisation has significantly increased over the past year. | |||||

| High transaction volume requires additional time and effort for accurate GST/VAT reporting. | ||||||

| The frequency and complexity of transactions impact our ability to comply efficiently with GST/VAT regulations. | ||||||

| IT Infrastructure | Our organisation has reliable IT systems to support GST/VAT filing and reporting. | |||||

| Technical resources (software, hardware, internet connectivity) are sufficient to manage GST/VAT compliance. | ||||||

| IT infrastructure enables smooth and timely preparation of GST/VAT submissions. | ||||||

| Regulatory Environment | GST/VAT rules and regulations in our country are clear and easy to understand. | |||||

| Frequent changes in tax regulations affect our ability to file accurately and on time. | ||||||

| Government guidance and support facilitate compliance with GST/VAT requirements. | ||||||

| GST Compliance Error Rate | Our organisation frequently encounters errors in GST/VAT reporting. | |||||

| Manual interventions in tax processes often lead to discrepancies in compliance. | ||||||

| Errors in GST/VAT filings are primarily due to system or process inefficiencies. | ||||||

| Filing Time | Preparing and submitting GST/VAT returns takes a considerable amount of time in our organisation. | |||||

| The complexity of tax regulations significantly prolongs filing time. | ||||||

| Automated systems (if any) help reduce the time required for GST/VAT filing. |

REFERENCES

AboAlsamh, H. (2025). The dark side of international talent management: Exploring the negative effect of talent repatriation on multinational enterprises’ performance with the meditating role of reverse culture shock. AJBMSS-Advance Journal of Business Management and Social Sciences. https://doi.org/10.65080/942npc70.

AbuAkel, S. A., & Ibrahim, M. (2023). The effect of relative advantage, top management support and IT infrastructure on E-filing adoption. Journal of Risk and Financial Management, 16(6), 295. https://doi.org/10.3390/jrfm16060295.

Abubakar, J., Yusuf, S. O., Ocran, G., Owusu, P., Yusuf, P. O., & Paul-Adeleye, A. H. (2024). Exploring the impact of AI-driven and blockchain-enabled tax filing systems on smes in the era of technological innovation: A review of benefits, challenges, and adoption barriers. World Journal of Advanced Research and Reviews, 23(03), 1867-1878. https://doi.org/10.30574/wjarr.2024.23.3.2754.

Adefunke, A. B. & Mayowa, I. O. (2024). Effect of e-taxation system on government tax revenue in Nigeria. Journal of Academic Research in Economics. 16(2), 221-238. Available from: https://www.jare-sh.com/downloads/jul_2024/adefunke.pdf.

Adelakun, B. O. (2024). Legal frameworks and tax compliance in the digital economy: a finance perspective. International Journal of Advanced Economics. 6(3), 26-35. https://doi.org/10.51594/ijae.v6i3.900.

Anomah, S. (2024). Blockchain technology integration in tax policy: Navigating challenges and unlocking opportunities for improving the taxation of Ghana’s digital economy. Scientific African, 24, e02210. https://doi.org/10.1016/j.sciaf.2024.e02210.

Ariyibi, K. O. (2024). The application of blockchain technology to improve tax compliance and ensure transparency in global transactions. International Journal of Science and Research Archive, 13(02), 1516-1527. https://doi.org/10.30574/ijsra.2024.13.2.2286.

Ashfaq, K., Riaz, A., & Iftikhar, F. (2022). Does Blockchain Technology Facilitate the Tax System in the Era of Industry 4.0?. Global Economics Review, 7(2), 33-44. http://dx.doi.org/10.31703/ger.2022(VII-II).04.

Belahouaoui, R., & Attak, E. H. (2024). Digital taxation, artificial intelligence and Tax Administration 3.0: improving tax compliance behavior–a systematic literature review using textometry (2016–2023). Accounting Research Journal, 37(2), 172-191. https://doi.org/10.1108/ARJ-12-2023-0372.

Carter, L., Simmons, C., Hayes, K., Palmer, M., Price, L., Brooks, Z., Scott, A., & Richardson, E. (2025). Integrating Block chain with Cloud Tax Compliance Systems. Available from: https://www.researchgate.net/profile/Olatunji-Isreal/publication/396559006_Integrating_Block_chain_with_Cloud_Tax_Compliance_Systems/links/68f21fefe7f5f867e6e04689/Integrating-Block-chain-with-Cloud-Tax-Compliance-Systems.pdf.

Dagunduro, M. E., Falana, G. A., Akinadewo, I. S., Oluwagbade, O. I., & Akinboboye, G. O. (2025). Role of digital tax platforms adoption in enhancing revenue generation and capital projects funding in emerging markets. Economy, 12(2), 26-39. https://doi.org/10.20448/economy.v12i2.6778.

Dandona, I., Tomar, P. K., & Verma, S. K. (2024). Goods And Services Tax in India: A Long-Term Trend and Growth Analysis. Library of Progress-Library Science, Information Technology & Computer, 44(3), 1647. Available from: https://openurl.ebsco.com/EPDB%3Agcd%3A12%3A33092972/detailv2?sid=ebsco%3Aplink%3Ascholar&id=ebsco%3Agcd%3A180917381&crl=c&link_origin=scholar.google.com.

Garg, S., Priyanka, Narwal, K. P., & Kumar, S. (2023). Goods and Service Tax and its implications on revenue efficiency of sub-national governments in India: an empirical analysis. American Journal of Business, 38(4), 193-210. https://doi.org/10.1108/AJB-09-2022-0144.

Ghosh, S. (2022). Formalising the Informal through GST: Evidence from a Survey of MSMEs. Review of Development and Change, 27(2), 150-169. https://doi.org/10.1177/09722661221130138.

Gitema, R., Ogaga, D., & Kimwolo, D. (2025). Effect of Legislative Reforms on Turnover Tax Compliance among Small-Scale Traders in Ruaraka Nairobi, Kenya. Journal of Finance and Accounting, 5(2), 11-23. https://doi.org/10.70619/vol5iss2pp11-23.

Haq, I. (2025). FBR’s persistent failures and the urgent need for comprehensive tax reforms in Pakistan. The Friday Times. Available from: https://www.thefridaytimes.com/04-Jan-2025/fbr-s-persistent-failures-and-the-urgent-need-for-comprehensive-tax-reforms-in-pakistan.

Haji-Othman, Y., & Yusuff, M. S. S. (2022). Assessing reliability and validity of attitude construct using partial least squares structural equation modeling. International Journal of Academic Research in Business and Social Sciences, 12(5), 378-385. http://doi.org/10.6007/IJARBSS/v12-i5/13289.

Harishekar, L., & Manoj, G. (2021). GST and its impact on small and medium scale enterprises-a study of peenya industrial area in Bangalore, Karnataka. Studies in Business and Economics, 16(1), 81-94. http://doi.org/10.2478/sbe-2021-0007.

Heinemann, M., & Stiller, W. (2025). Digitalization and cross-border tax fraud: evidence from e-invoicing in Italy. International Tax and Public Finance, 32(1), 195-237. https://doi.org/10.1007/s10797-023-09820-x.

Iqbal, M. M., Ali, M., Hina, U., & Shaikh, T. A. (2025). The future of smart tax systems: Integrating artificial intelligence, blockchain, and autonomous compliance technologies for transparent and efficient tax administration. Journal of Social Sciences and Economics, 4(1), 99-108. https://doi.org/10.61363/hhnkcz03.

Kabwe, R., & Van Zyl, S. P. (2021). Value-added tax in the digital economy: A fresh look at the South African dispensation. Obiter, 42(3), 499-528. Available from: https://journals.co.za/doi/epdf/10.10520/ejc-obiter_v42_n3_a4.

Khan, T. S. (2015). Why are tax revenues so low in South Asia? World Economic Forum. Available from: https://www.weforum.org/stories/2015/02/why-are-tax-revenues-so-low-in-south-asia/.

Khati, K., Khan, F., Pande, L., Joshi, G., & Mishra, A. (2024). Block chain-based solutions for enhancing goods and services tax (GST) compliance and transparency. In Challenges in Information, Communication and Computing Technology (pp. 155-161). CRC Press. Available from: https://www.taylorfrancis.com/chapters/oa-edit/10.1201/9781003559092-27/block-chain-based-solutions-enhancing-goods-services-tax-gst-compliance-transparency-khati-khan-pande-geetanjali-joshi-abhishek-mishra.

Kumar, M., & Gokhru, A. (2025). Factors influencing taxpayer compliance in India post-GST implementation: a behavioral analysis. Future-Ready Management Adapting to Industry 5.0, 27-34. Available from: https://www.academia.edu/144019310/Future_Ready_Management.

Kushwah, S. V., Nathani, N., & Vigg, M. (2021). Impact of tax knowledge, tax penalties, and E-filing on tax compliance in India. Indian Journal of Finance, 15 (5-7), 61-74. https://doi.org/10.17010/ijf/2021/v15i5-7/164493.

Mallick, H. (2021). Do governance quality and ICT infrastructure influence the tax revenue mobilisation? An empirical analysis for India. Economic Change and Restructuring, 54, 371-415. https://doi.org/10.1007/s10644-020-09282-9.

Mohd Dzin, N. H., & Lay, Y. F. (2021). Validity and reliability of adapted self-efficacy scales in Malaysian context using PLS-SEM approach. Education Sciences, 11(11), 676. https://doi.org/10.3390/educsci11110676.

OECD (2025), Revenue Statistics in Asia and the Pacific 2025: Personal Income Taxation in Asia and the Pacific, OECD Publishing, Paris, https://doi.org/10.1787/6c04402f-en.

Olabanji, S. O. (2023). Technological tools in facilitating cryptocurrency tax compliance: An exploration of software and platforms supporting individual and business adherence to tax norms. https://dx.doi.org/10.2139/ssrn.4600838.

Owens, J., & Hodžić, S. (2022). Policy note: Blockchain technology: Potential for digital tax administration. Intertax, 50(11), 813 – 823. https://doi.org/10.54648/taxi2022087.

Reva, A. (2015). Toward a more business friendly tax regime: Key challenges in South Asia. World Bank Policy Research Working Paper, (7513). Available from: https://documents1.worldbank.org/curated/en/345891467987893736/pdf/WPS7513.pdf.

Russo, G. M., Tomei, P. A., Serra, B., & Mello, S. (2021). Differences in the use of 5-or 7-point likert scale: an application in food safety culture. Organizational Cultures, 21(2), 1-17. https://doi.org/10.18848/2327-8013/CGP/v21i02/1-17.

Setyowati, M. S., Utami, N. D., Saragih, A. H., & Hendrawan, A. (2020). Blockchain technology application for value-added tax systems. Journal of open innovation: technology, market, and complexity, 6(4), 156. https://doi.org/10.3390/joitmc6040156.

Sidik, M. (2022). Digital services tax: Challenge of international cooperation for harmonization. Journal of Tax and Business, 3(1), 56-64. https://doi.org/10.55336/jpb.v3i1.46.

Sureka, A., & Bordoloi, N. (2024). The Impact of Blocked Credit and Unavailability of Input Tax Credit on MSMEs in India: An Empirical Study. Journal of Tax Reform, 10(3), 572-590. https://doi.org/10.15826/jtr.2024.10.3.185.

Taherdoost, H. (2022). A critical review of blockchain acceptance models—blockchain technology adoption frameworks and applications. Computers, 11(2), 24. https://doi.org/10.3390/computers11020024.

Tajik, O., Golzar, J., & Noor, S. (2025). Purposive sampling. International Journal of Education & Language Studies, 2(2), 1-9. Available from:https://www.ijels.net/article_220924_e5fa33c4c61f5d8e2844c56441ef1687.pdf.

Wulandari, D. S., & Dasman, S. (2023). Taxpayer compliance: The role of taxation digitalization system and technology acceptance model (TAM) with internet understanding as a mediating variable. East Asian Journal of Multidisciplinary Research, 2(6), 2385-2396. https://doi.org/10.55927/eajmr.v2i6.4653.

Yayman, D. (2021). Blockchain in taxation. Journal of Accounting and Finance, 21(4), 140-155. https://doi.org/10.33423/jaf.v21i4.4530.