- ABSTRACT:

- 1. INTRODUCTION

- 2. LITERATURE REVIEW

- 3. METHODS

- 4. RESULTS

- 5. DISCUSSION

- CONCLUSION

- LIMITATIONS & FUTURE DIRECTION

- IMPLICATIONS

- LIST OF ABBREVIATIONS

- AUTHOR'S CONTRIBUTION

- ETHICAL STATEMENT & INFORMED CONSENT

- AVAILABILITY OF DATA AND MATERIALS

- FUNDING

- CONFLICT OF INTEREST

- ACKNOWLEDGEMENTS

- DECLARATION OF AI

- APPENDIX A

- REFERENCES

Evaluating the Effectiveness of Robo-Advisory in Retail Investments: A Case of Malaysia

PDF

PDF

1Department of Finance and Accounting, Al-Yammamh University, Riyadh, Saudi Arabia

Received: 01 January, 2026

Accepted: 28 March, 2026

Revised: 26 March, 2026

Published: 28 April, 2026

ABSTRACT:

Introduction: This study assessed the efficiency of robo-advisory in improving portfolio returns and diversification for Malaysian retail investors. It also investigated the role of trust in algorithms, perceived usefulness, perceived fairness, and investor digital literacy in influencing the use and customization of robo-advisory services.

Methods: This study followed an experimental, simulation-based research design using a prototype robo-advisory model with a sample size of 300. The results of portfolios’ return post-advisory were compared with returns generated by traditional static advisory recommendations over a simulated 30-day horizon.

Results: The findings indicated a significant increase in portfolio returns and diversification scores due to the provision of robo-advisory and portfolio management services. For instance, this study’s findings showed that robo-advisory improved simulated returns and diversification. In addition, fairness and trust significantly predicted adoption, and lastly, the findings also showed that digital literacy mediated selected effects.

Conclusion: Findings implied that it is necessary to improve transparency, fairness, and digital literacy programmes to build on the acceptance of robo-advisory and maximise the performance of algorithms in portfolios in the Malaysian retail investment market.

Keywords: Robo-advisory, Portfolio management, retail investment, digital literacy, Malaysia.

1. INTRODUCTION

Retail investment in Malaysia is rapidly digitising, and there is increased concern about algorithm-based portfolio management and expanded involvement in the capital markets. This study discusses the potential to improve retail investors’ performance in Malaysia through personalised robo-advisory. As reported by (Derbali & Lamouchi, 2020), investment in Malaysia is in terms of stocks, bonds, and sukuk, and portfolio design remains an issue that has baffled many of the retail investors who are exposed to market volatility, a lack of sufficient financial literacy, and access to professional advice that does not evenly apply to all. The report of the (Securities Commission Malaysia, 2025) indicates that the capital market in Malaysia reached a record RM4.2 trillion in 2024; however, local retail investors were net sellers of equities, totalling RM5.83 billion, and there was no relationship between market growth and retail performance.

As indicated by (Ahn et al., 2020; Puspaningtyas, 2022) also automated, personalised advice Digital investment management (DIM) platforms have been developed at an expedited rate; total DIM had increased significantly to RM163.6 billion by end-2024, with more robo-advisory services available in Malaysia highlighted by (MDEC, 2025; Jailani & Adenan, 2023) also.

Securities Commission Malaysia Surveys and financial literacy tests also show that investors and shareholders are uncertain about their levels of digital and financial literacy skills, which can be translated into poor portfolio decisions and unnecessary losses, as stressed by (Muganda & Kasamani, 2023; and Mahdzn, 2020) consequently, the effectiveness of robo-advisors should be assessed and is policy-relevant. As per (Capponi et al., 2022; and Syed & Janamolla, 2024), robo-advisors are expected to provide scalable, cost-effective customization of risk profiles and asset allocation, and automated rebalancing solutions that have the potential to address behavioural biases, reduce the cost of information, and enhance execution among retail investors. In practical settings, the empirical evidence from this study can be used to determine that personalised robo-based algorithmic financial advice increases realised returns by substantial amounts compared to traditional static advice. Significant research gaps drive this experimental study; for instance, limited evidence of the individualised robo-advisory effect on investment returns in the Malaysian retail environment, and an apparent lack of experimental comparisons between fixed traditional advice and automated personalised advice. Recent developments in financial technology and artificial intelligence have sparked academic and commercial controversies over the purpose of robo-advisory systems in managing retail investments. As specified by (Boreiko & Massarotti, 2020; and Khosroavi, 2024), digital portfolio optimisation tools are claimed to be cost-effective, scalable, and less behaviourally biased. However, there is still concern about algorithmic transparency, fairness, and the extent of real performance improvements.

The existing literature, such as (Ajouz et al., 2025; and Singh & Kumar, 2025), shows that perceived usefulness, trust, and system personalisation play a significant role in the adoption of technology in the financial sphere. Nonetheless, empirical evidence has been fragmentary, especially regarding whether personalised robo-advisory systems can convert perceptual acceptance into quantifiable portfolio gains.

Although there is increasing academic interest and debate, critical gaps remain in understanding the functioning of algorithmic personalisation in emerging markets like Malaysia, as well as in the interactions between behavioural constructs and portfolio outcomes under the Modern Portfolio Theory (MPT), as (Puspaningtyas, 2022) indicates. The current literature is largely based on adoption models derived from surveys, without experimental testing of a portfolio’s performance under controlled conditions.

The reviewed literature creates several methodological and contextual gaps. First, (Ajouz et al., 2025) focus their study on survey-based perceived usefulness, trust, and social influence, measured using PLS-SEM. They therefore cannot use this metric to infer causality, and they neglect the portfolio’s actual performance, which is why the success of robo-advisory in enhancing returns is not examined. Second, (Singh & Kumar, 2025) examine user attitudes using an extended TAM framework in India with a finding on the mediating effect of demographic factors, including gender. Nevertheless, their research fails to investigate the factors of investor digital literacy. It limits their applicability to other markets, such as the Malaysian market, where differences in culture and regulation could affect adoption and personalisation.

Third, (Chen et al., 2025) examine the concept of personalisation in ESG-oriented portfolios in China and its influence on perceived usefulness and intention to adopt. However, the analysis is based solely on perceptual grounds, rather than on whether individualised advice will translate into better portfolio construction or risk-adjusted returns, which limits the empirical evidence supporting the effectiveness of robo-advisory adoption and personalisation in retail investment decisions.

To fill these gaps, it is necessary to conduct experimental and contextual studies in Malaysia that simultaneously measured perceptual, behavioural, and performance-related indicators to assess the adoption of robo-advisory and portfolio performance. To address these gaps, this research employs a quasi-experimental design with structural equation modelling to compare simulated short-term portfolio returns in a personalised robo-advisory with those in traditional advice.

The contributions of the study are considerable in the perspective of policy guidance, empirical evidence, and implications for investors, while recognising the short-term, simulated nature of the experiment.

Theoretically, it combines the ideas of behavioural finance and fintech to examine the impact of robo-advisory recommendations on investor decision-making.

Empirically, it presents experimental evidence on the effects of simulated short-term portfolio returns under personalised robo-advisory versus traditional fixed advice in Malaysia.

In practice, the research provides initial recommendations to investors, asset managers, and shareholders to embrace robo-based investment advisory technologies to enhance the performance of their short-term portfolios and their participation in Malaysia’s emerging capital markets.

The remainder of this paper comprised of literature review, methods, results, discussion, conclusion and implications.

2. LITERATURE REVIEW

2.1. Theoretical Framework

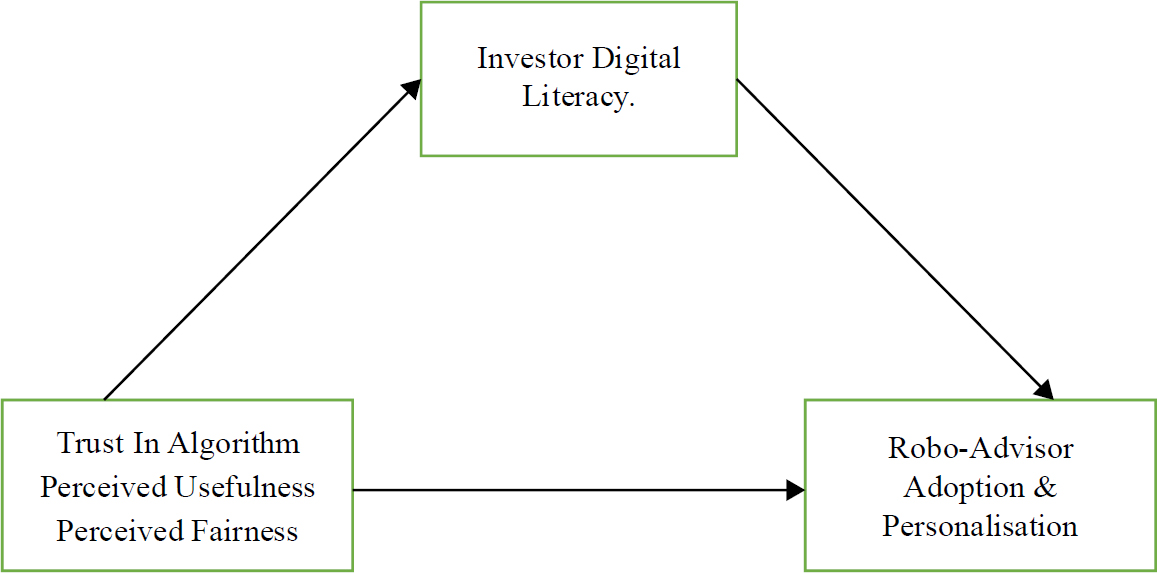

The research’s theoretical framework is based on the Modern Portfolio Theory (MPT), with the addition of behavioural finance and the Technology Acceptance Model (TAM), a consistent set of theoretical constructs to investigate the outcomes of personalised robo-advisory adoption and portfolio performance. MPT offers a direct normal standard, which implies that a system of diversification and systematic allocation allows investors to reach the ideal level of risk-return efficiency as suggested by (Dias, 2025; and Kumar et al., 2024). The MPT model, however, presupposes completely rational decision-making, which is not always true in reality due to behavioural biases such as loss aversion, overconfidence, and heuristics, as argued by (Mathur & Sharma, 2024; and Akhtar et al., 2025). Moreover, this study conceives of personalisation at the user level, rather than as a technical system feature. Robo-advisory systems can offer algorithmically based portfolio customization; however, in this context, personalisation is the degree to which investors accept, use, and trust the customised suggestions in their decision-making. Consequently, the operationalisation of personalisation is associated with adoption as a behavioural outcome, which reflects the perceived relevance, fit, and usability of customised advice, based on trust, usefulness, fairness, and investor digital literacy.

The constructs of TAM, namely perceived usefulness and trust in the algorithm, are defined as the conviction that investors have in the practical usefulness of the robo-advisor and in its reliability and impartial recommendations, respectively, as suggested by (Abbas, 2024; and Ajouz et al., 2025). These constructs influence intentions to embrace personalised advice, which, in turn, can indirectly affect the portfolio’s short-term performance. Perceived fairness is operationalised as procedural and algorithmic fairness, which entail transparency, consistency, and objectivity in decision-making. Investors who perceive greater fairness tend to engage with personalised recommendations that address the discrepancies between normative optimisation and behavioural acceptance of MPT. Taken together, these theories support the study’s variables and provide a logical account of the effects of personalised robo-advisory on adoption and simulated portfolio performance in the Malaysian environment.

The model builds on the classic TAM by introducing algorithmic fairness as a major credibility cue in case of technological uncertainty. Even though usefulness and ease of use are among the key drivers in TAM, the findings show that perceptions of fairness are more influential in the context of investments guided by an algorithm. It implies that the saliency of the ethical transparency and procedural consistency of financial decisions, rather than functional efficiency, increases when they are left to automated systems. The insignificant impact of perceived usefulness could indicate that investors base their expectations on the baseline level of performance and that fairness signals legitimacy and minimises the perceived algorithmic risk.

2.2. Hypotheses Development

2.2.1. Personalised Robo-Advisory and Investment Returns

The ability of robo-advisory to optimise portfolio return in retail investing has been scrutinised progressively. (Adegbenro et al., 2022; and Khosravi, 2024) focus on AI-based advisory systems, emphasizing high-level machine learning, stochastic optimization, and real-time data processing. There is strong evidence consistent with MPT, showing better risk-adjusted returns and lower risk drawdown, but it cannot be generalized to the real world because it relies on high-frequency data. In comparison, (Boreiko & Massarotti, 2020) examines 53 platforms in the US and Germany to determine how robo-advisors segment investor risk profiles. Their empirical cross-sectional study shows considerable heterogeneity in asset allocation across similar risk areas, indicating that MPT is not consistently applied in practical advisory practice; their study does not provide a performance evaluation. (Tahvildari, 2025) also explores profiling mechanisms in 45 German RAs and finds fragmented questionnaires, the growing complexity of portfolios, and integration across different asset types. Although the studies are detailed in descriptive terms, they lack performance testing and constrain causal inference about returns. Taken together, these experiments point to the need to conduct controlled experiments comparing advisory models, which leads to the formulation of the first hypothesis (H1) of the study.

H1: Personalised robo-advisory produces superior portfolio construction and higher returns than traditional static investment advice.

2.2.2. Trust in Algorithms, Perceived Usefulness and Adoption of Robo-Advisory

The adoption and personalisation of robo-advisory are robustly driven by perceived usefulness and trust in AI algorithms’ investment decisions. Recent studies by (Kulkarni et al., 2025; and Roh et al., 2023) examine how these psychological factors affect investors’ willingness to rely on automated portfolio solutions. (Ajouz et al., 2025) examine the drivers of adoption using PLS-SEM with 130 potential users, and the results indicate that perceived usefulness leads to significant improvements in trust and adoption intentions. They found that there is a trust-mediated mechanism in this case, with the social influence influencing adoption through belief in the effectiveness of the algorithms, which then strengthens adoption. They are, however, relatively small, which makes their findings difficult to generalise, and the paper does not test the impact of robo-advisors on real portfolio performance, making the correspondence to the Modern Portfolio Theory (MPT) rather abstract.

(Singh & Kumar, 2025) expand on TAM 454 fintech users in India, providing more empirical support. They discover that trust, perceived usefulness, and perceived risk have a strong influence on user attitudes, but no statistical impact on ease of use and social influence. This is contrary to (Ajouz et al., 2025), which assumes that contextual differences in the adoption of advisors exist. Including gender as a mediator provides a finer nuance, but, as in the earlier research paper, it relies solely on perceptual data. It does not conduct performance validation, as stressed by (Yi et al., 2023; and George, 2024). Regarding MPT, (Adewale, 2025; and Dias, 2025) argue that when users believe algorithms can rationally optimise portfolios, they use robo-advisors, yet no portfolio-level testing is conducted.

(Chen et al., 2025) focus on ESG-oriented robo-advisory, based on responses from 393 Chinese investors, and find that trust in the robo-advisory’s algorithms significantly impacts perceived usefulness, ease of use, and intention to adopt the robo-advisory. Unlike (Singh & Kumar, 2025; Chen et al., 2025) directly associate personalisation with intention, providing the most substantial evidence of the relevance of personalised advisory, but do not evaluate its returns. Together, these papers confirm that trust and perceived usefulness are at the heart of fintech adoption. Still, they are based on self-reported perceptions rather than objective portfolio performance, which limits their alignment with the MPT’s outcome-based orientation. Based on these literature arguments, following H2 and H3 of the study are developed;

H2: Trust in algorithms significantly affects the adoption and personalisation of robo-advisory in Malaysian retail investments.

H3: Perceived usefulness significantly affects the adoption and personalisation of robo-advisory in Malaysian retail investments.

2.2.3. Perceived Fairness and The Adoption of Robo-Advisory

Perceived fairness has quickly become an important predictor of robo-advisory adoption, as investors view algorithmic advice as equitable and unbiased decision-making. In their study of conversational AI in NCR, India, (Kapur & Srivastava, 2025) adopt a mixed-methods approach, which reveals issues related to bias, transparency, and accountability that directly influence judgments of fairness. Although their studies combine behavioural finance and AI governance models, the constructs of fairness are not quantitatively tested, which limits causal understanding. Unlike MPT, which presupposes rational, revealed by (Aw et al., 2023; Singh & Kumar, 2025) unbiased optimisation, fairness perceptions appeal to the socio-psychological aspect of algorithmic trust and are closer to the Algorithmic Fairness Theory, which states that adoption increases when users perceive that systems make unbiased decisions. In contrast to TAM-based research that focuses on usefulness and trust, (Kapur & Srivastava, 2025) note that fairness is a neglected obstacle that influences the intention to personalise portfolios. However, the study relies solely on secondary survey data, which undermines the robustness of the evidence. Building on these insights, this study hypothesised that;

H4: Perceived fairness significantly affects the adoption and personalisation of robo-advisory in Malaysian retail investments.

2.2.4. Mediating Effect of Investor Digital Literacy

Digital literacy among retail investors is a critical factor affecting the implementation of a robo-advisory platform, as it mediates the impact of trust, usefulness, and fairness on adoption and personalisation, as suggested by (Yang & Lee, 2024; and Bhattacharjee et al., 2025). As shown by (Ajouz et al., 2025), perceived usefulness and trust show statistically significant short-term improvements in a controlled simulation. Still, their model lacks the power to explain why investors could be more effective in using algorithmic insights to optimise portfolios, given their ability to understand digital tools. In the same vein, (Singh & Kumar, 2025) demonstrate that demographic mediators influence attitudes towards robo-advisors, meaning that digital literacy reinforces or weakens the relationship between perceptions of algorithms and intentions to adopt them. In their research, however, they do not explicitly consider users’ competence, which limits the explanatory depth.

According to (Chen et al., 2025), the adoption and personalisation of robo-advisory services are positively affected by perceived usefulness, fairness, and trust. Still, the effects are limited by investors’ ability to understand the adjustments to their portfolios. Hence, the lower the digital literacy, the poorer the adoption and personalisation is likely to be. Similarly, (Kapur & Shrivastava, 2025) also find that issues of fairness and transparency are more pronounced among less digitally fluent investors, suggesting that literacy influences the impact of perceived fairness on adoption. In theory, this mediating role is facilitated by the extensions of the Technology Acceptance Model and Algorithmic Fairness Theory. In contrast, MPT presupposes the rational consideration of portfolio optimisation, which is enabled by digital literacy. Consequently, these literature arguments lead to formulation of H5 of the study:

H5: Investor digital literacy mediates the impact of trust in algorithms, perceived usefulness, and perceived fairness on the adoption and personalisation of robo-advisory in Malaysian retail investments.

We have depicted all the hypothesised relationships in Fig. (1).

Fig. (1). Conceptual framework.

3. METHODS

The study follows an experimental design by applying a scenario-based (algorithmic) robo-advisory simulation rather than an automated online system. The robo-advisory intervention was described by a formal model that generated maximum-return portfolios under the assumptions of Modern Portfolio Theory, subject to decision risk constraints. To remove market-related variations, market data were fixed between the two groups using an identical historical price series. The participants did not trade manually; rather, the robo-advisory group received portfolio allocations via algorithmic method. Portfolio returns were simulated over a 30-day horizon, using the same return assumptions and rebalancing frequency. The design guarantees internal consistency and prevents real-time market execution. The research, therefore, analyses simulated short-term portfolio performance rather than actual performance, which makes the approach experimental and well-suited to controlled comparative research. After that, perceptual constructs of the research, such as trust in algorithms, perceived usefulness, perceived fairness, and robo-advisory adoption and personalisation were surveyed in a structured way, (see Appendix A), using a 5-point Likert scale as proposed by (Russo et al., 2021) also.

The prototype of the robo-advisory built portfolios in accordance with Maximum Return optimization constraints within the context of a predetermined Modern Portfolio Theory choice. The asset universe was comprised of 6 companies. The risk-constrained and full-investment conditions (with weights summing to 1) were optimised. Rebalancing was performed at the start of the simulated 30-day period and did not involve intra-period trading. The transaction costs were omitted to isolate allocation efficiency. Both the intervention and the control portfolios had the same historical market price path to compare them. In this way, the difference in performance is due solely to differences in allocation, rather than to external market variation. The score of diversifications was calculated as a normalised portfolio concentration index related to the dispersion of weights of the asset’s holdings. In particular, the score is calculated as Diversification Score = 1 − Σ(wᵢ²), where wᵢ is the weight of asset in the portfolio. A high value signified a low concentration risk and a high level of diversification. The score ranges between 0 and 1.

The sample for the study’s survey was increased to 300 participants, who were also comprised of retail investors and shareholders of retail companies in Malaysia. The survey was aimed at a final sample of 300 investors, of whom 100 were randomly selected from the total respondents. The random sampling technique was used to ensure that each retail investor in the sampling frame had an equal chance of being selected, thereby eliminating selection bias and strengthening causal inference in the experimental design, as (Ballance, 2024) also suggested. Sample size was calculated using the z-probability formula as suggested by (Qing & Valliant, 2025) also:

![]()

where represents the z-value at a 95% confidence level (1.96), is the estimated proportion of the population (0.5), and is the margin of error (0.05). According to this formula, the lowest sample size was 384, which was determined by the expected response and exclusion criteria. The number of people approached was 600, and 360 responded, for a response rate of approximately 60%. The final sample consisted of 300 participants, after excluding 60 incomplete responses and outliers.

The professional sites used to recruit participants included LinkedIn and the official social media accounts of Malaysian-based retail companies, which could lead to self-selection bias. To counter this, random assignment was used at the experimental level, and eligibility screening was conducted to ensure similar investment experience among participants. Furthermore, non-response bias was overcome by comparing the results of early respondents (n1 = 30) and late respondents (n2 = 30) and ensuring that no statistically significant differences existed, recommended by (Fantazy & Tipu, 2024) as well.

To ensure transparency across the survey and experimental components, the 300 respondents used in the analysis of the structural model were used to obtain the study results. Of this overall sample, 100 were selected at random for the quasi-experimental simulation. The pre- and post-intervention portfolio assessments were carried out on the same participants who participated in the experiment and were analysed using a paired-samples t-test. Therefore, the sample (n = 100) under the experiment is a part of the total survey sample (n = 300). Participants were randomly assigned to the intervention and received traditional static advice, rather than a robo-advisory maximum-return simulation. This design provides internal consistency and a clear separation between survey inference and the analysis of the experiment’s performance. Common method bias (CMB) was estimated, as the perceptual constructs were collected from the same respondents using a single survey instrument suggested by (Ballance, 2024). During data collection, anonymity and the separation of measures for constructs were ensured in accordance with the procedure guidelines. As recommended by (Fantazy & Tipu, 2024), the Harman single-factor test and variance inflation factor (VIF) analysis were statistically applied to investigate the possibility of bias. The findings showed that no individual factor accounted for most of the variance, and VIFs were below the critical value of 5, suggesting that common method bias is not a major threat to the model’s validity.

To analyse the data collated from the initial experiment, a paired-samples T-test was applied to assess the significance of differences between the mean returns and the mean portfolio diversification score, as suggested by (Afifah et al., 2022), and to answer the first hypothesis of the study. It was followed by an analysis of survey data using PLS-SEM, as suggested by (Memon et al., 2021), to test the hypotheses from H2 to H5. Reliability and validity were assessed using confirmatory factor analysis (CFA) and AVEs, including Cronbach’s alpha, composite reliability, and convergent validity. Then, path analysis using PLS-SEM was conducted to examine causal relationships among constructs, thereby allowing testing all hypotheses proposed in the study, as indicated by (Mohd Dzin & Lay, 2021) as well. The combined approach guaranteed both performance-based and perceptual analysis of robo-advisory adoption and personalisation in the case of retail investments. The complete workflow diagram of the study is provided in Fig. (2).

Fig. (2). Workflow diagram.

4. RESULTS

4.1. Demographics Analysis

The statistical results in Table 1 shows demographic profile of the survey population (n = 300). It is observed that among total surveyed participants, 57% were males and 43% were females with average ages 26-35 years (27.33%), 36-45 years (27%), 46-55 years (24%), and 56+ years (21.67%). Besides, regarding familiarity with robo-advisory, 21.67% were slightly familiar, 33.33% were moderately familiar, 28.33% were generally familiar, and 16.67% were extremely familiar. Moreover, with respect to income level, 25% of the participants earn RM10,000-15,000 per month, 37.33% earn RM15,000-20,000, and 37.67% earn RM20,000-30,000 per month. Moreover, with respect to occupation, 21.67% of the participants were investment advisors, 38.33% were mutual funds and wealth managers, and 40% were stockholders and retail investors. Lastly, in terms of investment size, 21.67% invested RM 75, 000-100,000 and 28.33% invested RM 150,000-275,000 in investment assets.

Table 1. Demographic profile.

| Demographic Category | Frequency (n) | Percentage (%) | |

| Gender | Male | 171 | 57.00% |

| Female | 129 | 43.00% | |

| Age Range | 26-35 | 82 | 27.33% |

| 36-45 | 81 | 27.00% | |

| 46-55 | 72 | 24.00% | |

| 56+ | 65 | 21.67% | |

| Income Level | RM 10,000-15,000 | 75 | 25.00% |

| RM 15,000-20,000 | 112 | 37.33% | |

| RM 20,000-30,0000 | 113 | 37.67% | |

| Occupation | Investment Advisors | 65 | 21.67% |

| Mutual Funds and Wealth Managers | 115 | 38.33% | |

| Stockholders and Retail Investors | 120 | 40.00% | |

| Investment Size | RM 75, 000-100,000 | 110 | 36.67% |

| RM 100,000-150,000 | 105 | 35.00% | |

| RM 150,000-275,000 | 85 | 28.33% | |

| Familiarity with Robo-Advisory for Investment Decisions | Slightly familiar | 65 | 21.67% |

| Moderately familiar | 100 | 33.33% | |

| Familiar | 85 | 28.33% | |

| Extremely familiar | 50 | 16.67% | |

4.2. Frequency Analysis

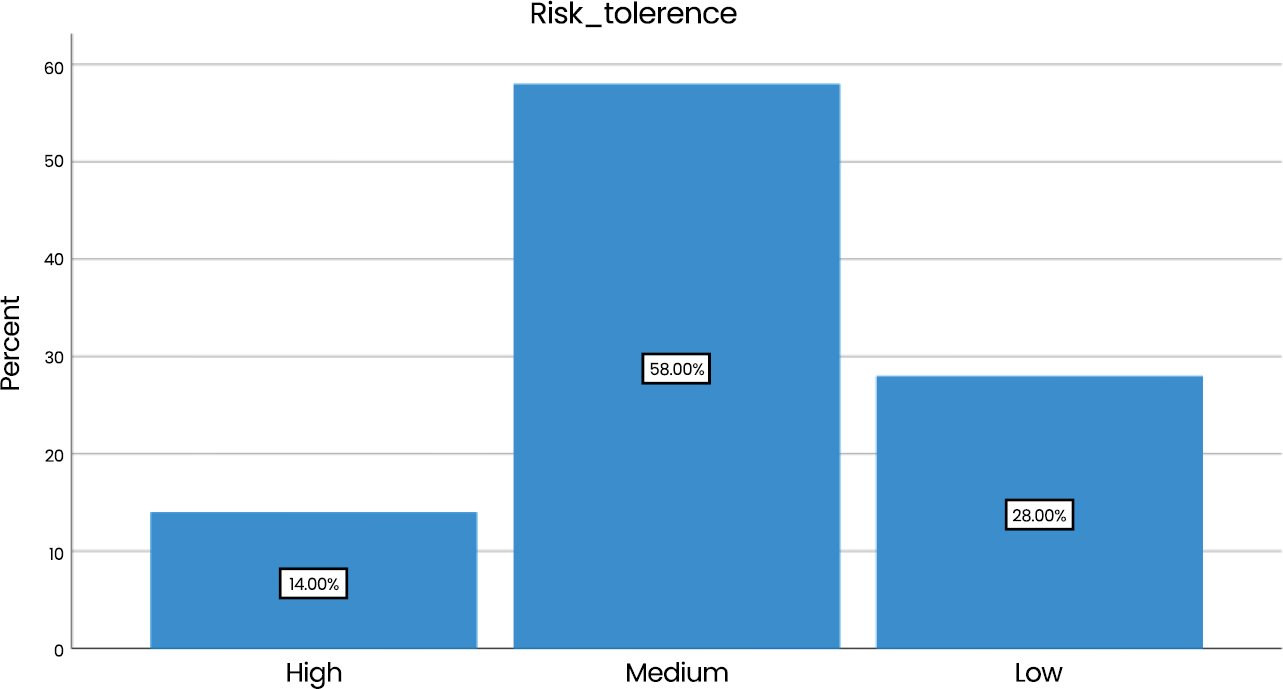

The statistical results in Fig. (3) indicate that among the total (n = 100) participants in the experiment, 28% displayed low risk tolerance, 58% displayed medium risk tolerance, and 14% displayed high risk tolerance.

Fig. (3). Risk tolerance.

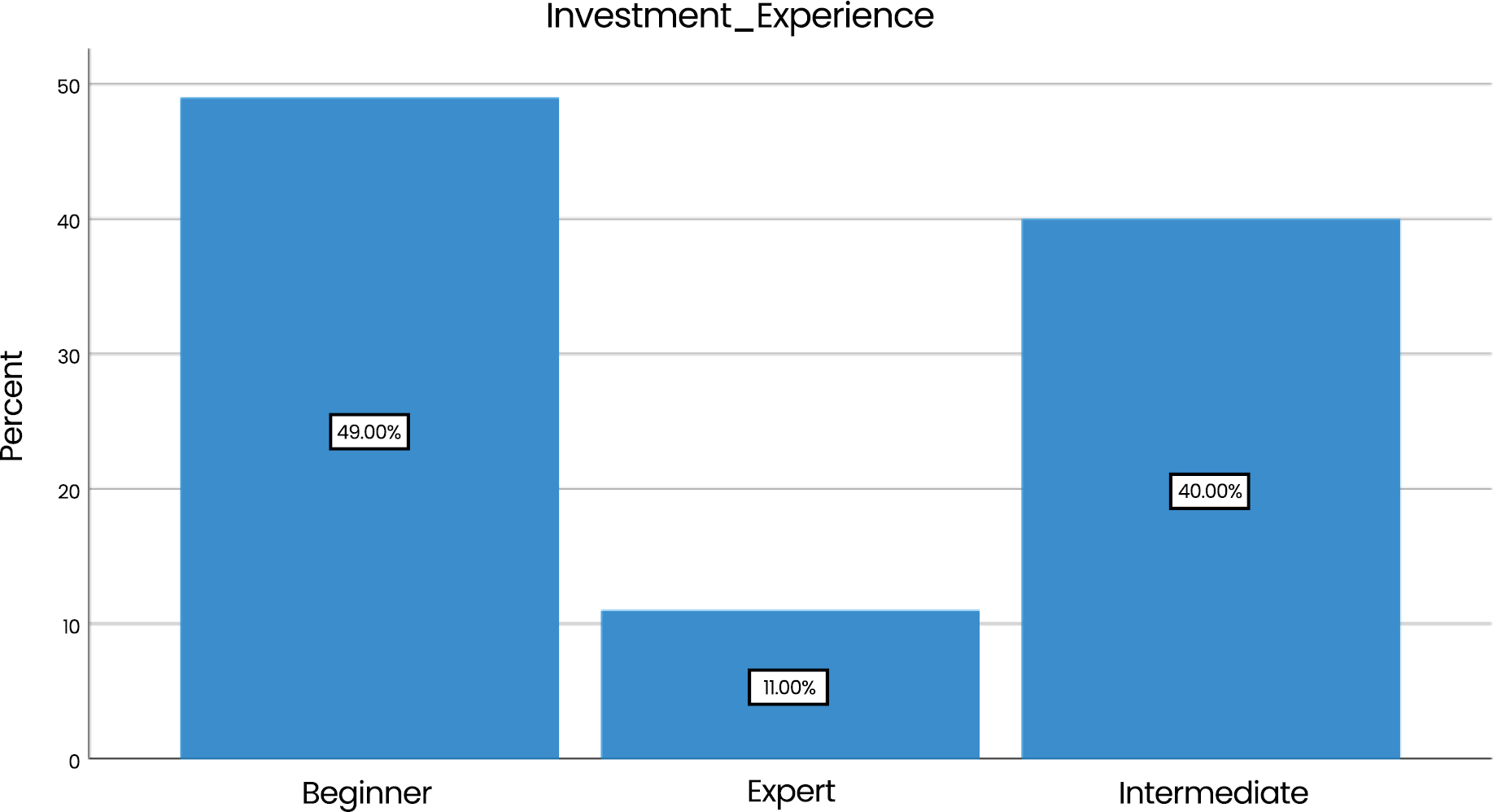

Based on the results in Fig. (4), it can be observed that, among the total participants in the experiment, 40% had intermediate investment experience, 11% were identified as experts, and 49% were beginners.

Fig. (4). Investment experience.

4.3. Paired Sample T-test

A paired-samples t-test was conducted to examine whether portfolio returns and portfolio diversification score increased when the group of investors was exposed to robo-advisory services. The results are specified in Table 2.

Table 2. Paired sample T-test.

| t-Test: Paired Two Sample for Means | ||

| – | Pre-Advisory Portfolio Return | Post-Advisory Portfolio Return |

| Mean | 4% | 7% |

| Variance | 0.033% | 0.046% |

| Observations | 100 | 100 |

| Pearson Correlation | 0.753 | – |

| Hypothesized Mean Difference | 0 | – |

| df | 99 | – |

| t Stat | -21.205 | – |

| P(T<=t) one-tail | 0.000 | – |

| t Critical one-tail | 1.660 | – |

| P(T<=t) two-tail | 0.00 | – |

| t Critical two-tail | 1.984 | – |

The results of the paired-samples T-test indicate a statistically significant increase in portfolio returns after the robo-advisory. The thirty-day simulated portfolio returns were surged from 4% to nearly 7% following the intervention of robo-advisory. The difference was also statistically significant at (t = –21.21; p < 0.001). As the magnitude of surges is found to be modest in absolute terms, its economic pertinence must be interpreted within the short simulation horizon and regulated or controlled conditions. Such increments in the returns can be transformed into materially greater cumulative returns. The t-test value is negative because the paired difference (Pre – Post) is negative when post-intervention returns exceed pre-intervention returns. The negative sign therefore indicates improvement, not deterioration. To further assess practical importance, Cohen’s d was calculated to estimate the size of the pre-post change, indicating a large effect size consistent with the statistical significance of the findings. In addition, when taken into account alongside the observed portfolio diversification, the results indicate meaningful optimisation rather than just numerical gain. However, the simulated setting limits direct inference about long-run wealth accumulation, warranting careful interpretation of its economic significance. These findings suggest that post-advisory returns are considerably higher than pre-advisory returns. In general, the results clearly show that a robo-advisory intervention significantly improved investment performance over the simulated 30-day period.

From the results in Table 3, related to the mean diversification score pre- and post-robo-advisory intervention, it can be observed that the pre-experiment mean (0.367, SD: 0.081) was significantly increased to 0.603 (SD: 0.191). This indicates that robo-advisory services significantly increased portfolio diversification scores. The Maximum score was also increased from 0.52 to 0.894. The diversification score was computed by applying a normalised index that captures asset class dispersion and weight balance within the portfolio holdings, where higher values indicate greater diversification. The score, which is closer to zero, mimics concentrated portfolios, whereas values above 0.60 are usually taken to indicate portfolios that are effectively diversified. From a theoretical perspective, this enhancement is consistent with MPT, which posits that diversification reduces unsystematic risk without proportionately decreasing expected returns. The post-intervention indicates that assets were reallocated systematically through a robo-based investment advisory to achieve a more even risk distribution than in participants’ initial portfolios. Considering that retail investors in Malaysia usually exhibit concentration tendencies and home bias, the observed shifts towards greater diversification suggest a return-maximising portfolio optimisation rather than random variation. However, as the score is based on a simulated setting, it indicates structural improvements in asset allocation quality rather than guaranteed long-term risk reduction.

Table 3. Mean diversification score.

| Pre-Advisory Diversification Score | Post Advisory Portfolio Diversification Score | ||

| Mean | 0.367 | Mean | 0.603 |

| Standard Deviation | 0.081 | Standard Deviation | 0.191 |

| Minimum | 0.154 | Minimum | 0.307 |

| Maximum | 0.527 | Maximum | 0.894 |

4.4. Measurement Model Confirmatory Factor Analysis (CFA)

The reliability, internal consistency, and convergent validity of the study’s measurement model are analysed using CFA approaches, including Cronbach’s Alpha, Composite reliability, and convergent validity, as indicated by (Haji-Othman & Yusuff, 2022) as well. The results of CFA are provided in Table 4.

Table 4. Measurement model.

| Latent Variables | Indicators | Factor Loadings | Cronbach’s Alpha | Composite Reliability (rho_a) | Average Variance Extracted (AVE) |

| Investor Digital Literacy | IDL1 | 0.906 | 0.901 | 0.901 | 0.835 |

| IDL2 | 0.934 | ||||

| IDL3 | 0.901 | ||||

| Perceived Fairness | PF1 | 0.887 | 0.884 | 0.886 | 0.812 |

| PF2 | 0.928 | ||||

| PF3 | 0.888 | ||||

| Perceived Usefulness | PU1 | 0.843 | 0.818 | 0.831 | 0.733 |

| PU2 | 0.910 | ||||

| PU3 | 0.814 | ||||

| Robo-Advisor Adoption & Personalisation | RAAP1 | 0.905 | 0.894 | 0.889 | 0.824 |

| RAAP2 | 0.930 | ||||

| RAAP3 | 0.889 | ||||

| Trust In Algorithm | TA1 | 0.878 | 0.837 | 0.842 | 0.754 |

| TA2 | 0.888 | ||||

| TA3 | 0.840 |

Results of the CFA indicate valid and reliable measurement model. The factor loadings for all constructs are high, ranging from 0.814 to 0.934, which exceeds the acceptable minimum of 0.60 and suggests that all items represent the latent variable to a high degree. Cronbach’s alpha and composite reliability are also high, above the threshold of 0.70, indicating high internal consistency and reliability. Convergent validity is also supported, with all AVEs exceeding 0.50 and values ranging from 0.733 to 0.835, indicating that each construct accounts for a significant percentage of the variance in its indicators. The measurement model, in general, has high psychometric properties, indicating that the Investor Digital Literacy, Perceived Fairness, Perceived Usefulness, Trust in Algorithm, and Robo-Advisor Adoption and Personalisation are measured reliably and validly.

4.5. Discriminant Validity

The discriminant validity explains the separability and distinctiveness among the constructs of the study and also allows analyse of whether variables do not possess conceptual overlap. It is analyse using HTMT ratio against the threshold of 0.85. The results of discriminant validity are provided in Table 5.

Table 5. Discriminant validity.

| – | Investor Digital Literacy | Perceived Fairness | Perceived Usefulness | Rob-Advisory Adoption and Personalisation |

| Perceived Fairness | 0.401 | – | – | – |

| Perceived Usefulness | 0.406 | 0.460 | – | – |

| Rob-Advisory Adoption and Personalisation | 0.454 | 0.471 | 0.305 | – |

| Trust in Algorithm | 0.531 | 0.585 | 0.577 | 0.235 |

The HTMT scores indicate that discriminant validity is generally achieved across all constructs. All HTMT ratios range between 0.235 and 0.585, well below the 0.85 threshold, confirming discriminant validity. For instance, the HTMT value is found between Perceived Usefulness and Robo-Advisory Adoption and Personalisation (0.305) which shows no conceptual overlapping and distinctiveness among variables. Similarly, the HTMT value between Investor Digital Literacy and Perceived Fairness (0.401) is lower than the desired value of 0.85, indicating no conceptual overlap. The remaining HTMT ratios (0.235-0.585) also confirm that both constructs are conceptually distinct. Generally, the model meets the conditions for discriminant validity, providing evidence of the structural integrity and separability of the constructs.

4.6. Path Coefficient

The path coefficient outcomes shown in Table 6, indicate multifaceted behavioural dynamics that go beyond the traditional Technology Acceptance Model (TAM) anticipations. The positive and statistically significant predictors are Perceived Fairness, which has strong effects on Investor Digital Literacy (β = 0.479; p < 0.001) and Robo-Advisory Adoption and Personalisation (β = 0.317; p < 0.001). This observation shows that the perception of transparency, procedural uniformity, and algorithmic impartiality are outliers in determining how investors would engage in robo-advisory systems. The environment of the retail investment in Malaysia where the elements of advisory conflict of interest and non-transparent fee frameworks still remain central issues: fairness seems to be a precondition of digital communication, rather than a secondary ethical factor.

Table 6. Path coefficients.

| – | Path Coefficients | T-Statistics (|O/STDEV|) | P-Values |

| Investor Digital Literacy -> Rob-advisory Adoption and Personalisation | 0.266*** | 2.714 | 0.007 |

| Perceived Fairness -> Investor Digital Literacy | 0.479*** | 7.402 | 0.000 |

| Perceived Fairness -> Rob-advisory Adoption and Personalisation | 0.317*** | 3.569 | 0.000 |

| Perceived Usefulness -> Investor Digital Literacy | 0.065 | 1.054 | 0.292 |

| Perceived Usefulness -> Rob-advisory Adoption and Personalisation | 0.144* | 1.792 | 0.073 |

| Trust in Algorithm -> Investor Digital Literacy | 0.208*** | 2.942 | 0.003 |

| Trust in Algorithm -> Rob-advisory Adoption and Personalisation | 0.197*** | 2.283 | 0.022 |

| Specific Indirect Effects | |||

| Perceived Fairness -> Investor Digital Literacy -> Rob-advisory Adoption and Personalisation | 0.127*** | 2.424 | 0.015 |

| Perceived Usefulness -> Investor Digital Literacy -> Rob-advisory Adoption and Personalisation | 0.017 | 0.893 | 0.372 |

| Trust in Algorithm -> Investor Digital Literacy -> Rob-advisory adoption and Personalisation | 0.055** | 2.175 | 0.030 |

Note: ***Significance at 1%; **Significance at 5%; *Significance at 10%;

On the one hand, despite the classical assumptions about TAM, Perceived Usefulness does not significantly affect Investor Digital Literacy (β = 0.065; p = 0.292) and has a small impact at the 10% level of significance only (β = 0.144; p = 0.073). This paradox implies that the efficient operation or performance expectation by Malaysian investors do not necessarily transfer to behavioural acceptance. The statistically significant and positive impact of Trust in Algorithm on adoption (β = 0.197; p = 0.022). Instead of making adoption instant, increased trust can reduce the sensitivity of the investors to the authority of algorithms and the non-existence of downside risk, resulting in increased adoption of robo-advisory among investors. It is also interesting to note that trust has a positive relationship with Investor Digital Literacy (β = 0.208; p = 0.003), implying that trust inspires investors to read and investigate robo-advisory systems and determine whether to use it or not.

The mediating analysis results signify the relationship between fairness perceptions and adoption is greatly enhanced by investor Digital Literacy (β = 0.127; p = 0.015) meaning that the perceptions of fairness are converted to adoption only when investors are technologically well-endowed with the ability to adopt. Similarly, the mediating effect of Trust in Algorithm (β = 0.055; p = 0.030) indicates that trust holds mediating effects on the adoption through facilitating the capacity of investors to comprehend and consider the algorithmic advice. Conversely, the insignificant mediating effect for Perceived Usefulness validates its restricted role, strengthening that functional value alone is inadequate to determine the adoption of robo-advisory in the Malaysian context.

4.7. Model Explanatory Power

The model explanatory power is analysed through R-square and Adjusted R-square values which explains the percentage of variance in dependent that can be predicted by independent variables. The results of explanatory power are provided in Table 7.

Table 7. Explanatory power.

| – | R-Square | R-Square Adjusted |

| Investor Digital Literacy | 0.435 | 0.430 |

| Rob-advisory Adoption and Personalisation | 0.240 | 0.230 |

The results in Table 7 shows that 43.5% variation in investors digital literacy and 24% variation in rob-advisory adoption and personalisation can be predicted by trust in algorithms, perceived usefulness, and perceived fairness.

5. DISCUSSION

The H1 results leads to acceptance of the hypothesis and validates that the portfolio returns and the diversification scores significantly improved after being advised through robots. These findings are line with the Modern Portfolio Theory (MPT) that speculates that structured diversification, as opposed to single stock selection, is the cause of the best risk-return results suggested by (Ahn et al., 2020) also. The robo-advisory framework was found to adhere to MPT allocation guidelines more uniformly than the conventional static advice, which concurs with previous findings that algorithms reduce behavioural biases including home bias and familiarity bias suggested by (Boreiko & Massarotti, 2020; Khosravi, 2024) also. Nevertheless, the given enhancement can also be explained by the fact that robo-based investment suggestions make the process of making complex allocations easier and quicker than manual portfolio creation and encourage the participants to engage in the process even more, which is also suggested by (Kapur & Shrivastava, 2025) also. Also, the participants of experiment were responsive to more in the simulated environment due to the knowledge of assessment, which may have exaggerated short-term effects. In line with (Singh & Kumar, 2025), these findings are viewed as a demonstration of the potential of robo-advisory to enhance the quality of short-run allocations and diversification and not evidence of the enduring superiority of returns. To guarantee that these effects are continuing, longer-horizon and real-market applications are desirable.

The improvement in Malaysia is however more evident than other research done in technologically advanced markets where investors already have fairly diversified portfolios. By comparison, Malaysian retail investors tend to have concentrated holdings and domestic stocks or stocks familiar with the sector, which increases the effect of automatic diversification suggested by (Ajouz et al., 2025) also. Risk-aversion and low exposure to quantitative methods of portfolio management are further aspects of culture that explain why robo-advisory solutions provide better portfolio diversification score in Malaysia. Therefore, the findings substantiated the fact that algorithmic optimisation can be an effective way to improve returns and diversification, confirmed MPT, as well as emphasising significant returns to Malaysian retail investors.

The acceptance of H2 means that the level of trust in algorithms is a major factor in determining robo-advisory adoption and personalisation among the Malaysian retail investors. In line with (Ajouz et al., 2025), trust is a key antecedent of utilisation of automated financial services. Also, similar, to the consistent beneficial outcomes that were found by (Singh & Kumar, 2025) in the Indian setting, the findings in Malaysia also show a path where trust has a direct significant and positive impact on the adoption and indirectly enhances adoption through investor digital literacy. This implies that in the presence of adequate knowledge on how an algorithm works, trust will tend to increase adoption of robo-advisory, and strengthen the view of robo-advisors as an effective investment advisory tool. The investors in a risk averse culture like Malaysia are cautious about investment decisions, and financial risks, though, trust in algorithmic investment advisories with the digital literacy and expertise to assess and analyse digital advice enhance adoption and personalisation. Such findings thus, suggest that trust is also facilitated by both cognitive and digital competencies, which characterises the fact that algorithmic credibility should be augmented by investor capability and literacy also in order to achieve its practical adoption potential.

In relation to theory, trust acts as behavioural supplement to the MPT assumption on rational diversification. Whereas MPT focuses on risk-return optimisation, real investor behaviour is based on belief in the mechanism that creates portfolio recommendations. Malaysian investors will have confidence in algorithmic risk modelling and be suspicious over automated decision-making, which yield mixed outcomes. Therefore, despite the impact of trust, the impact is more significant when it is adjusted by investor literacy, that is, both cultural risk aversion and the phase of transition of the Malaysian digital finance ecosystem.

The results of H3 suggest that the perceived usefulness has a significant, though, small positive impact on the adoption and personalisation of robo-advisor in Malaysia, not as strong as those seen in other related studies. For instance, (Tahvildari, 2025) also established a further close relationship between the perceptions of usefulness and adoption of robo-advisory as the more the investors perceive that robo-advice can help increase their performance, the more they are likely to adopt it as part of an investment routine. Similarly, (Singh & Kumar, 2025) documented that the attitude and intention of the user towards the perceived usefulness have a direct impact and that it is an underlying aspect of the Technology Acceptance Model (TAM). Contrasting, the Malaysian scores indicate that usefulness has a peripheral direct impact indicating that perceived functional value alone cannot be used to ascertain behavioural uptake.

This deviation may be due to cultural and behavioural factors. For instance, in Malaysian retail investor tends to use a human financial adviser or peer network, and inter-personal validation is more important than functional benefits of the system (Chen et al., 2025). As a result, usefulness cannot be understood as a driver as it would only be meaningful when combined with trust and literacy. Relative to MPT, usefulness is consistent with the rational optimisation of risk-reward portfolio by investors; nonetheless, unless the benefits of algorithmic optimisation are made clear to them, Malaysian investors might not consider algorithmic optimisation useful. Consequently, usefulness is important, but its effects are conditional, and not so decisive as trust and fairness.

The findings of H4 are also accepted and support the claim that the perceived fairness is a significant predictor of robo-advisory adoption and personalisation, which is in line with (Kapur & Shrivastava, 2025) who highlighted that the perceived transparency of algorithms and unbiased advice lie at the centre of investor-related confidence towards conversational AI and robo-advisors. Fairness seems to be even more of a determinant than usefulness in Malaysia implying that ethical and distributional issues play a significant role in decision-making in investments. It is in contrast with the Chinese setting in (Chen et al., 2025) where the driving forces of adoption and personalisation and ESG characteristics prevailed, whereas the issues of fairness were secondary. The more sensitive nature of Malaysians to fairness can be explained by the cultural focus on procedural justice, the increased sensitivity to financial misconduct scandals, and the worries about the lack of transparency in algorithms.

In the MPT perspective, fairness does not affect directly on the optimisation of risk-return, it determines the willingness to trust such risk-return optimisation systems. Malaysian investors appear to be unwilling to pass the control of the portfolio to algorithms unless they believe that the recommendations provided are not biased, conflict-free, and do not have any hidden commercial objectives revealed by (Muganda & Kasamani, 2023; Rossi & Utkus, 2020) also. This implies that there is mediation of rational adoption by MPT in terms of behavioural norms. Thus, the perceived fairness serves as both a psychological protective mechanism and a behaviour change agent, which confirms that transparent algorithms are significant to enhancing adoption and personalisation for diversification of portfolios within the new robo-advisory environment in Malaysia.

The validation of H5 evidently signifies investor digital literacy as a significant mediating factor to transform behavioural insights such as trust, perceived usefulness, and fairness into robo-advisory adoption and personalisation. (Chen et al., 2025) also defines digital literacy as a flexible phenomenon, though the concept is typically viewed as an exogenous capacity that determines the use of technology, whereas the study describes it as such that can transform during the interaction with algorithmic systems suggested in the findings of (Ajouz et al., 2025) as well. In the experimental setting, exposure to personalised robo-advisory recommendations has the potential to promote the knowledge of system logic in participants and thus, perceived digital competence. This rationale corresponds to the literacy as a post-exposure cognitive adaptation and not a trait. Instead of being a direct performance driver, literacy mediates the process of cognition of trust, perceived usefulness, and perceived fairness in processing and acting, which is consistent with (Ajouz et al., 2025), who opines that algorithmic awareness can only reduce uncertainty when investors can meaningfully interpret system outputs. The same is reflected by (Singh & Kumar, 2025) who demonstrate that the attitudinal effects are enhanced by digital familiarity, but the Malaysian data indicates a steeper learning curve whereby exposure to AI finance is limited at the outset which limits the uptake of behaviour. The difference with (Chen et al., 2025), who use mediation, could also be due to the differences in the context, such as, in Malaysia, the digital competencies are heterogeneous, so trust or fairness signals cannot be used on their own without the competencies to assess them.

Another specification could position digital literacy as an antecedent instead of an outcome of personalised exposure to robo-advisory, which raises the possibility of endogeneity concerns in a single-wave structural equation model. It is probable that more digitally literate investors in the past are more inclined to gain, accept or even make sense of robo-advisory advice which was unveiled in the discussion of (Singh & Kumar, 2025) as well. In this study, though, digital literacy was assessed as perceived competence after experimental exposure to personalised robo-advisory situations. The directional specification was temporally plausible since the quasi-experimental design guaranteed that the participants were exposed to the robo-advisory simulation first and then surveyed using the survey instrument. Literacy is, therefore, a post exposure evaluative competence and not pre-existing ability which is indicated by (Kapur & Shrivastava, 2025) also. However, the prospective studies are suggested to investigate bidirectional or longitudinal models because the prospective study could test the potential of bidirectional relationships that might exist between digital literacy, adoption behaviour, and portfolio performance in the long-term.

The effects of learning-curve can be also exacerbated by short-term experimental exposure, in which case digitally skilled individuals are advantaged by the learning-curve, and less literate investors are either wary or do as expect. This means that the results cannot be viewed as evidence of the improved robo-advisory results. In terms of MPT, literacy increases the capacity of an investor to be aware of diversification algorithms and risk-optimised allocations in the gap between theoretical optimisation and behavioural acceptance. Therefore, digital literacy is the means of converting abstract trust and subjective beliefs of fairness into the adoption intentions. The findings highlight the importance of improving digital capacities of Malaysian investors to enable maximum attainment of the benefits of robo-advisory.

CONCLUSION

The study demonstrates that the adoption of robo-advisory in Malaysia is not influenced by the technology but a multifaceted interaction of behavioural, ethical, and capability-based characteristics. Although algorithmic models have been promised to ensure optimisation in line with MPT, the implied tools are only used by Malaysian investors when trust, fairness, and literacy factors are satisfied- a continued disconnecting the gap between the theoretical and actual efficiency. The experiment also demonstrates that the returns and diversification are improved using algorithmic advice, but the behavioural constraints restrict its implementation on a broad basis. This shows that an increase in technological development does not necessarily lead to empowerment of investors’ return and investment decisions, unless they rely equally on literacy and governance. Generally, the study states that the potential of robo-advisory in Malaysia is depended on algorithmic transparency, trust, investor digital literacy, and culture-sensitive trust-building processes will follow the technology.

LIMITATIONS & FUTURE DIRECTION

The study while holds valuable empirical and theoretical contributions, it also holds certain limitations as well. For instance, at first, the study relied on 30-days simulated investment period which possible does not capture market volatility over the long-run period or behavioural adaptation of investors towards robo-advisory tools. Furthermore, the sample is sufficient but there are geographical and demographical limitation and this limits generalisability of the sample to the wider investor population in Malaysia. Bias also be brought about by self-reported survey responses. Future studies need to include longitudinal real-market data, increase diversity of participants and also incorporate aspects of qualitative research to explore the nuances of behaviour in a deeper way. The comparison of studies between ASEAN markets and the experiment with various robo-advisory services can be helpful to better figure out the contextual factors and enhance the external validity of investment advice provided by algorithms. Lastly, the major limitation of the research is that it utilises short-term, simulated portfolio returns, thus limiting the ability to make inferences on the long- term performance, risk behaviour, and market-cycle effects. The short run returns can be due to short-term adjustments or learning as opposed to value creation. To determine the persistence, drawdowns and behavioural adjustment to robo-advisory systems over time, future studies need to utilise longitudinal designs with real accounts of investments or protracted simulators across different market conditions.

IMPLICATIONS

The results provide tentative policy suggestions to the changing digital investment environment in Malaysia as opposed to prescriptive ones. Investigators like the Securities Commission Malaysia can view these findings as the initial evidence pointing to the significance of usefulness, algorithmic trust, and communication and transparency for retail investors to guarantee enhanced robo investment advisory services and its adoption. The insights can be used by financial institutions and fintech providers to enhance pilot-level adoption of robo-advisory services especially among digitally literate retail investors. Moreover, the investor education agencies can consider that digital literacy as a facilitating provision that contributes to informed usage of automated advisory tools. In general, the research feeds the current policy discussion of responsible fintech experimentation, though it does not suggest immediate massive regulation and market reorganization. The implications of the present study also comprise theoretical and practical implications. Hypothetically, the results broaden the perspectives of technology acceptance and behavioural finance by underscoring the ascendancy of perceived fairness as well as the situational role of digital literacy in the algorithm-driven investment contexts. In practise, the findings guide fintech developers and financial institutions to increase the level of transparency, credibility, and interaction with users in robo-advisory systems. Policymakers are also suggested to look to encourage algorithmic disclosure and investor education as a way of adopting them responsibly. All these implications collectively show that personalised robo-advisory systems are driving investment behaviour, portfolio optimisation, and participation of investors in emerging digital finance ecosystems.

LIST OF ABBREVIATIONS

| CFA | = | Confirmatory Factor Analysis |

| CMB | = | Common Method Bias |

| MPT | = | Modern Portfolio Theory |

| TAM | = | Technology Acceptance Model |

| VIF | = | Variance Inflation Factor |

AUTHOR’S CONTRIBUTION

I.A.B. has contributed to conceptualization, idea generation, problem statement, methodology, results analysis, results interpretation.

ETHICAL STATEMENT & INFORMED CONSENT

All procedures were conducted in compliance with the guidelines of the institutional research ethics committee and adhered to the principles outlined in the Declaration of Helsinki. Informed consent was obtained from all participants prior to their inclusion in the study. To protect participant confidentiality, all data were anonymized at the time of collection, and no personally identifiable information was recorded.

AVAILABILITY OF DATA AND MATERIALS

The data will be made available on reasonable request by contacting the corresponding author [I.A.B.].

FUNDING

None.

CONFLICT OF INTEREST

The author declares no conflicts of interest, financial or otherwise.

ACKNOWLEDGEMENTS

Declared none.

DECLARATION OF AI

During the preparation of this manuscript, the author used ChatGPT for language polishing. After utilizing this tool, the author carefully reviewed and refined the content as necessary and accept full responsibility for the accuracy and integrity of the published work.

APPENDIX A

Demographic Factors

| Item | Response Options (Tick ✓ One) |

| Gender | ☐ Male ☐ Female |

| Age Group | ☐ 26–35 ☐ 36–45 ☐ 46–55 ☐ 56+ |

| Income Level | ☐ RM 10,000-15,000, ☐ RM 15,000-20,000 ☐ RM 20,000-30,0000 |

| Occupation | ☐ Investment Advisors ☐ Mutual Funds and Wealth Managers ☐ Stockholders and Retail Investors |

| Investment Size | ☐ RM 75, 000-100,000 ☐ RM 100,000-150,000 ☐ RM 150,000-275,000 |

| Familiarity with Robo-Advisory Personalisation for Investment Decisions | ☐ Slightly familiar ☐ Moderately familiar ☐ Familiar ☐ Extremely familiar |

Survey Questionnaire

| Construct | Item Code | Items | SD | D | N | A | SA |

| Trust in Algorithm | TA1 | I trust the recommendations provided by algorithm-based robo-advisors. | |||||

| TA2 | I believe algorithm-driven investment decisions are reliable. | ||||||

| TA3 | I feel confident that robo-advisory algorithms operate in my best interest. | ||||||

| Perceived Usefulness | PU1 | Using a robo-advisor would improve my investment decision-making. | |||||

| PU2 | Robo-advisory tools help me make more efficient investment choices. | ||||||

| PU3 | Robo-advisors enhance the overall performance of my investment portfolio. | ||||||

| Perceived Fairness | PF1 | I believe robo-advisors provide unbiased investment recommendations. | |||||

| PF2 | The robo-advisory system treats all investors fairly and consistently. | ||||||

| PF3 | I feel that the algorithms used in robo-advisors operate transparently and ethically. | ||||||

| Investor Digital Literacy | DL1 | I am comfortable using digital financial platforms for investment decisions. | |||||

| DL2 | I can independently evaluate and understand online investment tools. | ||||||

| DL3 | I have the digital skills necessary to use robo-advisory platforms effectively. | ||||||

| Robo-Advisor Adoption & Personalisation | RAP1 | I am willing to adopt robo-advisory services for my investment decisions. | |||||

| RAP2 | I prefer investment advice that is personalised based on my financial profile. | ||||||

| RAP3 | I intend to rely on robo-advisors for personalised portfolio recommendations in the future. |

REFERENCES

Abbas, S. K. (2024). AI meets finance: the rise of AI-powered Robo-advisors. Journal of Electrical Systems, 20(11), 1011-1016. https://doi.org/10.52783/jes.7359

Adegbenro, A., Madueke, A., Ojo, A., & Alabi, C. (2022). AI-Driven Wealth Advisory: Machine Learning Models for Personalized Investment Portfolios and Risk Optimization. Communication In Physical Sciences, 8(4), 779-807. Available from: https://journalcps.com/index.php/volumes/article/view/739

Adewale, T. (2025). The Rise of Algorithmic Financial Advice: Robo-Advisors, Fintech Synergies, and Investment Theory in Practice. International Journal of Research Publication and Reviews, 6(1), 4832-4848. https://doi.org/10.55248/gengpi.6.0125.0640

Afifah, S., Mudzakir, A., & Nandiyanto, A. B. D. (2022). How to calculate paired sample t-test using SPSS software: From step-by-step processing for users to the practical examples in the analysis of the effect of application anti-fire bamboo teaching materials on student learning outcomes. Indonesian Journal of Teaching in Science, 2(1), 81-92. https://doi.org/10.17509/ijotis.v2i1.45895

Ajouz, M., Abu-AlSondos, I. A., Yaseen, S. G., Alkhwaldi, A. F., Al Moghrabi, A., & Al-Qaisi, N. (2025). Portfolio Management Through Financial Robo-advisors: Key Drivers of Potential Investor Adoption. In Applied Artificial Intelligence in Business: Systems, Tools and Techniques (pp. 283-294). Cham: Springer Nature Switzerland. https://doi.org/10.1007/978-3-031-90271-0_21

Akhtar, F., Akhtar, S., & Laeeq, M. (2025). Evolution of Robo‐Advisors: A Literature Review and Future Research Agenda. International Journal of Consumer Studies, 49(6), e70131. https://doi.org/10.1111/ijcs.70131

Ali, A., Salleh, M. A. M., & Mustaffa, N. (2022). Digital inheritance exploration (DIE) through digital inheritance model (DIM)—A guideline for digital assets planning after death. APS proceedings. Academica Press Solution. Available from: https://www.researchgate.net/publication/365315619 (Accessed on: May 12, 2025).

Aw, E. C. X., Leong, L. Y., Hew, J. J., Rana, N. P., Tan, T. M., & Jee, T. W. (2024). Counteracting dark sides of robo-advisors: justice, privacy and intrusion considerations. International Journal of Bank Marketing, 42(1), 133-151. https://doi.org/10.1108/IJBM-10-2022-0439

Ballance, O. J. (2024). Sampling and randomisation in experimental and quasi-experimental CALL studies: Issues and recommendations for design, reporting, review, and interpretation. ReCALL, 36(1), 58-71. https://doi.org/10.1017/S0958344023000162

Bhattacharjee, J., Singh, R., Pandey, S., & Sharma, R. (2025). Factors impacting stress in financial investment due to the use of artificial intelligence: a social networking analysis approach. AI & SOCIETY, 1-14. https://doi.org/10.1007/s00146-025-02754-4

Boreiko, D., & Massarotti, F. (2020). How risk profiles of investors affect robo-advised portfolios. Frontiers in Artificial Intelligence, 3, 60. https://doi.org/10.3389/frai.2020.00060

Capponi, A., Olafsson, S., & Zariphopoulou, T. (2022). Personalized robo-advising: Enhancing investment through client interaction. Management Science, 68(4), 2485-2512. https://doi.org/10.1287/mnsc.2021.4014

Chan, S. C., Liew, X. W., Lim, J. Y., & Man, S. K. (2023). Determinants of the intention to use financial robo-advisory in Malaysia. UTAR Institutional Repository. http://eprints.utar.edu.my/6059/1/fyp_FN_2023_CSC.pdf

Chen, A., Wang, S., Mehta, A. M., Asif, M., Xu, S., & Shahzad, M. F. (2025). FinTech adoption for ESG integration through robo advisors, personalization, and perceived trust. Scientific Reports, 15(1), 31125. https://doi.org/10.1038/s41598-025-17046-6

Derbali, A., & Lamouchi, A. (2020). Global financial crisis, foreign portfolio investment and volatility: Impact analysis on select Southeast Asian markets. Pacific Accounting Review, 32(2), 177-195. https://doi.org/10.1108/PAR-07-2019-0090

Dias, F. S. (2025). An Introduction to Robo-Advisors, Notable Fintech Implementations, and Underlying Theory. In Fintech and the Emerging Ecosystems: Exploring Centralised and Decentralised Financial Technologies (pp. 285-300). Cham: Springer Nature Switzerland. https://doi.org/10.1007/978-3-031-83402-8_11

Fantazy, K., & Tipu, S. A. A. (2024). Linking big data analytics capability and sustainable supply chain performance: mediating role of knowledge development. Management Research Review, 47(4), 512-536. https://doi.org/10.1108/MRR-01-2023-0018

George, A. S. (2024). Robo-revolution: Exploring the rise of automated financial advising systems and their impacts on management practices. Partners Universal Multidisciplinary Research Journal, 1(4), 1-6.

Haji-Othman, Y., & Yusuff, M. S. S. (2022). Assessing reliability and validity of attitude construct using partial least squares structural equation modeling. Int J Acad Res Bus Soc Sci, 12(5), 378-385. https://doi.org/10.6007/IJARBSS/v12-i5/13289

Jailani, M. N. A., & Adenan, F. (2023). Shariah Risk Management In Islamic Digital Banking In Malaysia: A Study At KAF Investment Bank: Pengurusan Risiko Syariah Dalam Perbankan Digital Islam Di Malaysia: Kajian Di KAF Investment Bank. al-Qanatir: International Journal of Islamic Studies, 30(2), 188-197. Available from: https://al-qanatir.com/aq/article/view/678

Kapur, G., & Shrivastava, S. (2025). Evaluating the Role of Conversational AI in Financial Investment Decision Making in NCR. International Journal of Economic Practices and Theories, 247-262. https://doi.org/10.52783/ijept.35

Khosravi, F. (2024). Transforming Investment Advisory Services Through Artificial Intelligence: A Study on Robo-Advisors and Algorithmic Portfolio Management. Nuvern Applied Science Reviews, 8(9), 1-8. https://nuvern.com/index.php/nasr/article/view/2024-09-04

Koneti, S. B. (2025). Artificial intelligence Applications in Retail and Investment Banking: Personalization, Robo-Advisory and Behavioral Analytics. Artificial Intelligence-Powered Finance: Algorithms, Analytics, and Automation for the Next Financial Revolution, 4, 72. https://doi.org/10.70593/978-93-7185-613-3

Kulkarni, M. S., Patil, K. P., & Pramod, D. (2025). The role of robo-advisors in behavioural finance, shaping investment decisions. Cogent Economics & Finance, 13(1), 2571403. https://doi.org/10.1080/23322039.2025.2571403

Kumar, K. R., Balaji, C., Suresh, M., Nagaraju, E., Natarajan, S., & Kumar, R. (2024). Study The Impact Of Ai Driven Rob Advisors on Wealth Management Services. Evaluate Their Effectiveness in Portfolio Management, Risk Assessment, And Personalized Investment Strategies, 30(5), 5819. https://doi.org/10.53555/kuey.v30i5.5819

Mahdzan, N. S., Zainudin, R., & Yoong, S. C. (2020). Investment literacy, risk tolerance and mutual fund investments: An exploratory study of working adults in Kuala Lumpur. International journal of Business and Society, 21(1), 111-133. https://doi.org/10.33736/ijbs.3230.2020

Mathur, P., & Sharma, A. M. (2024). Robo-advisors in investment management. In Risks and challenges of AI-driven finance: Bias, ethics, and security (pp. 121-145). IGI Global Scientific Publishing. https://doi.org/10.4018/979-8-3693-2185-0.ch006

MDEC. (2025). Available from: https://mdec.my/media-release/news-press-release/375/malaysia%E2%80%99s-digital-investments-hit-record–rm163.6-billion-in-2024 (Accessed on: November 11, 2025).

Memon, M. A., Ramayah, T., Cheah, J. H., Ting, H., Chuah, F., & Cham, T. H. (2021). PLS-SEM statistical programs: a review. Journal of Applied Structural Equation Modeling, 5(1), 1-14. https://doi.org/10.47263/JASEM.5(1)06

Mohd Dzin, N. H., & Lay, Y. F. (2021). Validity and reliability of adapted self-efficacy scales in Malaysian context using PLS-SEM approach. Education Sciences, 11(11), 676. https://doi.org/10.3390/educsci11110676

Puspaningtyas, M. (2022). The Role of Technology and Investment in Digitalization and The Economy in Malaysia. Tamansiswa Management Journal International, 4(1), 35-35. https://doi.org/10.54204/TMJI/Vol412022006

Qing, S., & Valliant, R. (2025). Extending Cochran’s sample size rule to stratified simple random sampling with applications to audit sampling. Journal of Official Statistics, 41(1), 309-328. https://doi.org/10.1177/0282423X241277054

Roh, T., Park, B. I., & Xiao, S. S. (2023). Adoption of AI-enabled Robo-advisors in Fintech: Simultaneous Employment of UTAUT and the Theory of Reasoned Action. Journal of Electronic Commerce Research, 24(1), 29-47.

Russo, G. M., Tomei, P. A., Serra, B., & Mello, S. (2021). Differences in the use of 5-or 7-point likert scale: an application in food safety culture. Organizational Cultures, 21(2), 1. https://doi.org/10.18848/2327-8013/CGP/v21i02/1-17

Securities Commission Malaysia. (2025). Available from: https://www.sc.com.my/resources/media/media-release/malaysian-capital-market-hits-record-rm42-trillion-in-2024-stays-resilient-amid-earnings-growth (Accessed on: November 11, 2025).

Singh, S., & Kumar, A. (2025). Investing in the future: an integrated model for analysing user attitudes towards Robo-advisory services with AI integration. Vilakshan-XIMB Journal of Management, 22(1), 158-175. https://doi.org/10.1108/XJM-03-2024-0046

Syed, W. K., & Janamolla, K. R. (2024). How AI-driven robo-advisors impact investment decision-making and portfolio performance in the financial sector: A comprehensive analysis. Int. Res. J. Eng. Technol, 11, 138-145.

Tahvildari, M. (2025). Analysis of investor profiling and portfolio recommendations by Robo-Advisors in Germany. Global Business & Finance Review, 30(8), 19. https://doi.org/10.17549/gbfr.2025.30.8.19

Yang, Q., & Lee, Y. C. (2024). Enhancing financial advisory services with GenAI: Consumer perceptions and attitudes through service-dominant logic and artificial intelligence device use acceptance perspectives. Journal of Risk and Financial Management, 17(10), 470. https://doi.org/10.3390/jrfm17100470

Yi, T. Z., Rom, N. A. M., Hassan, N. M., Samsurijan, M. S., & Ebekozien, A. (2023). The adoption of robo-advisory among millennials in the 21st century: trust, usability and knowledge perception. Sustainability, 15(7), 6016. https://doi.org/10.3390/su15076016