- ABSTRACT:

- 1. INTRODUCTION

- 2. LITERATURE REVIEW

- 3. METHODOLOGY

- 4. RESULTS AND ANALYSIS

- 5. DISCUSSION AND HYPOTHESES ASSESSMENT

- CONCLUSION

- FUTURE IMPLICATIONS

- POLICY IMPLICATIONS

- LIST OF ABBREVIATIONS

- AUTHOR'S CONTRIBUTION

- ETHICAL STATEMENT & INFORMED CONSENT

- AVAILABILITY OF DATA AND MATERIALS

- FUNDING

- CONFLICT OF INTEREST

- ACKNOWLEDGEMENTS

- DECLARATION OF AI

- APPENDIX A

- REFERENCES

AI-Powered Smart Ledgers and Hassle-Free Bookkeeping in SMES: Effects on Automation, Error Reduction, and Real-Time Compliance

PDF

PDF

1Jubail Industrial College, Jubail, Kingdom of Saudi Arabia

Received: 09 February, 2026

Accepted: 08 April, 2026

Revised: 08 April, 2026

Published: 08 May, 2026

ABSTRACT:

Introduction: This study aimed to analyse how the integration of AI-enabled smart ledgers impacts three major dimensions of bookkeeping, such as error reduction, automation, and real-time compliance monitoring in the case of UK SMEs.

Methodology: The current study used structured surveys and statistical data analysis to apply a primary quantitative research design. The study used a 5-point structured survey questionnaire with 383 SME representatives to collect a dataset. Further, the data were analysed using Partial Least Squares-Structural Equation Modelling (PLS-SEM).

Results: The findings showed a significant, positive predictive association between Smart Ledger adoption and Automation (β = 0.555; p = 0.001), Error Reduction (β = 0.479; p = 0.001), and Real-Time Compliance and Monitoring (β = 0.459; p = 0.001). In terms of mediation, Hassle-Free Bookkeeping was positively related with Smart Ledger adoption (β = 0.245; p = 0.001) and partially mediated its relationship with Automation (β = 0.307; p = 0.001) and Error Reduction (β = 0.174; p = 0.002); on the other hand, partially mediating the association with Real-Time Compliance and Monitoring (β = 0.321; p = 0.001).

Conclusion: The findings imply that the adoption of smart ledgers substantially reduces accounting errors, enables automated, hassle-free bookkeeping, and guarantees real-time compliance and monitoring of the financial reporting process in UK SMEs. The partial mediating role of hassle-free bookkeeping also underscores its substantiality in streamlining accounting and reporting processes, reducing complexity, and enhancing decision-making, which can guide policymakers and SMEs.

Keywords: Smart ledgers, hassle-free bookkeeping, error reduction, automation, real-time compliance, AI-powered.

1. INTRODUCTION

In contemporary times, where business sustainability is defined by financial and accounting agility, small and micro business enterprises (SMEs) continue to face the constraints of conventional bookkeeping and accounting practices. Notwithstanding the wider adoption and implementation of digital tools in large organizations, almost 81.30% of SMEs globally still rely on manual or traditional accounting systems, thereby increasing their susceptibility to lapses in regulatory compliance, human errors in recording transactions, and financial opacity (Darma et al., 2021). During the times when AI-enabled smart ledgers are reshaping industries, accounting processes, it’s potential to revolutionise bookkeeping in SMEs remains underexplored and underutilised (Pan & Lee, 2020). In the UK, (Mouka, 2025) notes that only 44% of SMEs use accounting software or an AI-driven ledger system, while 66% still rely on outdated systems. It leads to SMEs struggling to maintain accurate financial records and, thus, their tax returns. On the other hand, 82% of UK SMEs failed due to ineffective cash flow management driven by outdated ledger systems and financial reporting processes (Sanay, 2025).

In addition, the reason for specifically conducting this study among UK SMEs is a progressive focus on digitalization in response to surging regulatory complexities and requirements, as well as competitive market demands (Mouka, 2025). As the UK government has promoted digital transformation in reporting through initiatives such as Making Tax Digital (MTD), it has become a necessity for SMEs to adopt advanced financial reporting and recording technologies to improve financial transparency and efficiency (Bloom Financials, 2025). Therefore, by analysing and generating empirical evidence on the impact of AI-powered smart ledgers on improved, hassle-free bookkeeping, the study addresses a substantial need to automate accounting procedures and enhance financial transparency across SMEs in the UK. The findings of the current study will be beneficial to owners, accountants, and finance managers of SMEs in the UK, enabling them to adopt AI-powered smart ledgers to improve accounting processes, accuracy, and compliance with regulatory requirements in the UK business environment.

The process of bookkeeping is usually subject to administrative tasks and has now developed into a dynamic procedure that demands accuracy, speed, error detection, and compliance (Bawamohiddin et al., 2023). (Malik & Hussain, 2024) note that conventional tools, such as manual preparation of general ledgers and T-accounts, lack intelligence, adaptability, and scalability, which are required for error-free, hassle-free financial reporting and regulatory compliance. The evolution of AI-enabled, Smart or automated ledgers integrated with Machine Learning (ML) and distributed ledger systems provides a revolutionary, transformative alternative (Singh, 2025).

Smart Ledger in this study is operationally defined as an AI-based digital bookkeeping platform that combines automated data processing, error-detection algorithms, and real-time compliance monitoring features, and can be supported by underlying technologies like cloud computing, as well as blockchain-based verification where applicable (Noori Doabi, 2024; Weigel & Hiebl, 2023). Compared to conventional accounting solutions, Smart Ledgers allows for the recording, validation, and reporting of transactions autonomously with minimal human intervention. Although Smart Ledger involves blockchain, distributed ledger technology (DLT), big data analytics, or IoT integrations, this study conceptualizes Smart Ledger as an accounting application powered by AI, specifically, rather than an interchangeable construct, as suggested by (Kabir et al., 2025) as well.

At the time, the market for accounting technology was developing swiftly, with international spending on AI in accounting processes expected to surpass $6,389 billion by 2025 (Aarti, 2025), while the inclusion of SMEs in this digital revolution remains underexplored. In addition, Darma et al. (2021) also evidenced that practices of manual accounting, based on manual bookkeeping, not only burden SMEs with increased overhead costs and risks of error, but also inhibit their access to regulatory compliance, real-time access to accounting data, and the reduction of reporting errors. Therefore, the current article aims to fill this gap by empirically analysing how the integration of AI-enabled smart ledgers tends to impact three core aspects of bookkeeping, namely error reduction, automation, and real-time compliance monitoring. Unlike existing studies such as (Nofel et al., 2024; and Adekunle et al., 2023), which evaluated these variables in isolation or in a large-company context, this study investigates the relationships among the variables in the context of SMEs operating in the UK.

The proposed study has several major contributions, comprising theoretical, empirical, and practical contributions. In practical terms, the study is based on the Technology Acceptance Model (TAM) and associated accounting models, demonstrating how hassle-free bookkeeping mediates the relationships among smart ledger adoption, automation, error reduction, and real-time compliance monitoring. It provides valuable empirical evidence that the efficiency of the bookkeeping process increases significantly with the implementation of a smart ledger enabled by AI. This study contributes to the literature by jointly co-analysing the associations among smart ledger adoption, automation, reduced errors, and real-time compliance in UK SMEs, and by proposing a new mediating variable: hassle-free bookkeeping. The research provides context-specific insights into the role of AI-enabled accounting systems in streamlining processes and enhancing operational efficiency, with practical applicability for SME managers, accountants, and policymakers.

2. LITERATURE REVIEW

Theoretical Framework

The current study relies on both the Technology Acceptance Model (TAM) and the Resource-Based View (RBV) as theoretical rather than empirically tested prisms. According to (Noori Doabi, 2024), TAM clarifies the perceived usefulness and perceived ease of use, and how they influence users’ adoption of new technologies. The current study does not directly quantify these constructs; however, TAM provides an informative interpretative background for why accounting professionals in SMEs are willing to embrace AI-enabled smart ledger systems, especially when such systems maximize automation, accuracy, and compliance efficiency. Therefore, the use of TAM is to conceptualise the potential of technology acceptance behind adopting smart ledgers.

In a similar vein, the RBV, as presented by (Weigel & Hiebl, 2023), holds that competitive advantage is achieved when firms possess valuable, rare, and inimitable resources and capabilities. Although this research does not operationalize or measure specific RBV constructs, the theory provides an auxiliary insight into how smart ledgers powered by AI can be used as strategic organizational resources. Integration into bookkeeping processes can help increase operational efficiency, minimize errors, and improve compliance, contributing to better firm performance. Thus, both TAM and RBV are applied as explanatory frameworks to put the study’s findings in perspective, but not as tested theoretical frameworks.

Empirical Review

Due to rising concerns and limitations in traditional or manual accounting practices regarding the accuracy of accounting figures, error, and fraud detection, several studies have examined the benefits of automated procedures or smart ledgers in mitigating these risks (Elumilade et al., 2021). In coherence with these arguments, (Nofel et al., 2024) conducted the study to suggest a novel accounting system that is integrated with Internet of Things IoT, XBRL, and Blockchain. The researcher carried out interviews with 13 industry experts from IT, engineering, and financial systems. To analyse the data, NVivo software was used, which enabled transcribing interviews and developing relevant, codified themes aligned with the research objectives. As per findings of the study, the suggested system allows for automating the process of ledger preparation and accounting through IoT to collect accounting data, which is sent to blockchain-enabled ledgers, and acts as a database to develop automated journal entries using smart contracts XBRL, which was also reflected in the arguments made by (Sanad, 2024). The results of the study imply that Smart-contacts-based ledgers enable real-time capture of accounting data, enhance data accuracy, and ensure reliable recording of transactions and figures.

The above findings are consistent with (Roszkowska, 2021), who also stressed that IoT sensors and smart-contract-based ledgers enable the timely recording of accounting data, such as inventory, cash inflows and outflows, production, and depreciation, as journal entries. Similar findings were reported by (Kabir et al., 2025) in the United States, where the authors collected data from 194 professionals in the accounting domain using a structured survey questionnaire. The collected data were analyzed using Structural Equation Modeling (SEM) in SmartPLS. As per the study’s findings, IT adoption in the bookkeeping process, such as AI-enabled Smart ledgers, enhances the reliability, accuracy, and effectiveness of accounting data.

The above literature points out the potential of smart ledger to overcome the shortcomings of manual accounting, but also highlights certain weaknesses. (Nofel et al., 2024) proposed an IoT-XBRL-Blockchain framework based on a qualitative approach, collecting data through interviews and analyzing it using thematic analysis. The findings revealed the appropriateness of real-time information accuracy, but the proposed framework is not intended for use in the UK SME context, as the study focused on large firms, limiting the generalisability of the findings. Similarly, (Roszkowska, 2021) emphasized the use of IoT and smart contracts to enhance financial accounting procedures; however, the question of their real implementation was not addressed. The survey-based SEM by (Kabir et al., 2025) validated that the use of smart ledgers improves trustworthiness, but the sample (US) is limited to the generalisability to the UK SMEs. Considering these studies in the context of TAM, it can be inferred that perceived usefulness is the foundation of adoption, whereas RBV emphasises smart ledgers as strategic assets that develop accounting capacity. However, the insufficient exploration of intermediating processes, as well as the limitations peculiar to SMEs, suggests that it still requires additional empirical validation in many business settings.

Both studies, (Nofel et al., 2024; and Kabir et al., 2025), underscored the important role of AI-enabled Smart ledgers in improving the bookkeeping process through real-time data capture, enhanced accuracy, and automation. Both studies support the efficiency and dependability of the bookkeeping process driven by AI-enabled smart ledgers, but the main difference lies in the industrial context: industrial maturity and high adoption rates in the US lead to more consistent validation of the impacts of AI-enabled smart ledgers in improving the bookkeeping process across SMEs. The study by (Nofel et al., 2024) examines sector-specific hurdles and hesitancy to digital transformation, often due to financial constraints and the shortage of skilled workers, which affect the adoption of Smart ledgers in SMEs. Hence, similar findings can be expected in the UK SME sector; thus, following the hypothesis, H1 is formulated.

H1: There is a statistically significant predictive relationship of smart ledgers with the error reduction bookkeeping in small and medium-sized business organisations.

According to (Arabi, 2024), a blockchain-based Smart Ledger can be a potential substitute for the traditional accounting information recording system. For accounting purposes, transactions were recorded using three main mechanisms: double-entry accounting, judgment accounting, and ERP systems. However, it is important to note that every mechanism has limitations and weaknesses (Demirkan et al., 2020; Zhang et al., 2021). (Azman et al., 2021; Sharma et al., 2022) also reported similar results: the embracement of blockchain technology is mostly driven by features such as increased security and privacy, enhanced transparency and auditability, inalterability of records, greater cost-effectiveness, real-time transaction processing, and flexibility.

Furthermore, (Shalhoob et al., 2024) outline those big data analytics (BDA) helps to advance error identification and avert fraud in accounting processes. Conducting a desk study using a secondary data-collection method, the findings revealed that BDA improves fraud detection by combining data from diverse sources and employing advanced algorithms to detect anomalies. Eliminates false positives and enhances accuracy, which leads to the formation of hypothesis H2. In addition, (Musiliu et al., 2024) conducted an empirical investigation of Nigerian Banks. The researcher collected data from 300 employees of 14 banks in the region using a survey design. Analysing data using inferential statistics such as correlation and regression analysis techniques, the findings revealed that Smart Ledger with distributed ledger technology (DLT) positively and significantly impacts error reduction in accounting data and enhances its reliability and accuracy.The findings imply that, practically, big data analytics (BDA) in smart ledgers and DLTs guides for enhancing financial precision, fraud prevention, compliance with regulations, data-driven decision-making, and professional training for accountants.

(Arabi, 2024) maintained that Smart Ledgers based on blockchain technology can replace traditional accounting systems because they overcome the weaknesses of double-entry accounting, judgment accounting, and ERP systems. This was reiterated by (Sharma et al., 2022) who added security, transparency, and auditability to the framework of adoption drivers. These characteristics improve perceived usefulness TAM wise; hence provides incentive to use in the case where accuracy and reliability is relevant. (Shalhoob et al., 2024) provided a conceptual framework for how big data analytics (BDA) can enhance fraud detection by detecting anomalies across a variety of datasets. Nevertheless, their desk-based method has not been empirically validated and cannot therefore be used in practice. Conversely, (Musiliu et al., 2024) empirically showed using primary survey data gathered on Nigerian banks that distributed ledger technology (DLT) minimises accounting errors and increases the accuracy of the data. However, due to the high degree of digitisation and the presence of stringent banking regulation, the findings cannot be transferred to SMEs. Smart ledgers and BDA are strategic resources from an RBV perspective; however, their value depends on sectoral and contextual differences.

(Shalhoob et al., 2024) use a desk-based secondary analysis approach to provide a broader conceptual overview of how BDA improves fraud detection in accounting data; however, the lack of primary data limits its empirical validation and specificity to the context. In contrast, (Musiliu et al., 2024) provide primary data and statistical validation indicating that DLT-integrated smart ledgers tend to decrease accounting errors in Nigeria. Though the higher digitisation levels of the financial sector and regulatory requirements in banking tend to expand perceived effectiveness, likened to less regulated industries such as SMEs. The primary restraint in both studies is the lack of industry-wide diversity, as the results are derived from the banking industry or conceptual models, which limits their applicability to SMEs with lower digital maturity and integration. Therefore, a similar relationship can be tested in the context of UK SMEs, which leads to the formation of H2;

H2: Smart ledger automation has a statistically significant association with error reduction in the processes of accounting and bookkeeping across SMEs.

Moreover, with regard to the relationship amid real-time compliance monitoring through AI-integrated ledgers on regulatory adherence, several studies hold conclusive findings. For instance, according to (Xu et al., 2021), the blockchain network integrated into automated ledgers enables the secure, real-time retrieval of accounting data.In this perspective, (Grigg, 2024; Sarwar et al., 2023) unveiled that smart ledgers enabled with blockchain technology allow for the storage of data in incontrovertible, changeable, and transparent ledgers, which cannot be altered deprived of authorisation, which ensures the integrity of accounting data fed into journal entries.

On the other hand, (Chou et al., 2021) revealed that the smart contracts-based ledgers through blockchain allow for to update or change of accounting records on a timely basis, grounded on predefined policies established using financial reporting frameworks like IFRS and GAAP. The journal ledgers and entries are automatically updated in response to changes in accounting figures, transactions, inventories, or specific cost heads in the accounting system (Bawamohiddin et al., 2023). As a result of this automated procedure, (Elumilade et al., 2021) found that manual intervention is reduced, thereby ensuring the maintenance and accuracy of accounting records in line with financial reporting standards, leading to regulatory compliance and the avoidance of misrepresentation in accounts. This further reduces manual intervention, ensuring the maintenance and updating of accounting records ensuring real-time monitoring and compliance with financial reporting standards.

Several studies confirm that AI-integrated ledgers play an important role in real-time compliance monitoring. (Xu et al., 2021) mentioned the possibility of blockchain to provide and ensure real-time accounting information, and (Grigg, 2024) highlighted the advantages of transparency and immutability, which ensure the integrity of the information. In contrast, (Chou et al., 2021; and Bawamohiddin et al., 2023) confirmed that smart contracts can be updated in line with the IFRS and GAAP to reduce the likelihood of misrepresentation. However, these results are context-dependent, and most of the evidence is based on large companies rather than SMEs. Grounded in the Technology Acceptance Model (TAM), the perceived usefulness of smart ledgers underpins the development of hypothesis H3. Hence, similar results can be observed in the context of UK SMEs; based on these findings, the following hypothesis (H3) has been developed.

H3: There is a statistically significant relationship of the adoption of Smart ledgers enabled with blockchain technology on real-time compliance monitoring in SMEs.

Task-Technology Fit (TTF) Theory, according to which technology has a positive impact on performance when it aligns well effectively the tasks it is envisioned to support. Smart Ledgers, also supported by blockchain and AI, that perform data entry and validation (blockchain) and accuracy-based bookkeeping (Elumilade et al., 2021). Process efficiency and decreased complexity manifest through the mediating construct of hassle-free bookkeeping, which helps reduce accounting errors (Narang & Jain, 2024). The mediating role is explained by the fact that Smart Ledgers are not designed to avoid errors but guarantee automated, streamlined processes that reduce manual interference (Musiliu et al., 2024). In a similar vein, (Dashkevich et al., 2024; and Grigg, 2024) found that distributed ledger technologies also increase information accuracy by eliminating redundancy and human error. Therefore, hypothesis H4 is formulated to investigate how the pragmatic advantages of Smart Ledgers support effective bookkeeping to minimize accounting errors.

H4: There is a statistically significant mediating role of hassle-free bookkeeping in the relationship between Smart Ledgers and Error Reduction.

In addition, the Technology Acceptance Model (TAM) cites two factors, perceived usefulness and ease of use, as important motivational factors to adopt the technology. It is the perception of the usefulness of Smart Ledgers, specifically their automation, because when the process of bookkeeping becomes hassle-free (Bawamohiddin et al., 2023), the effects of using Smart Ledgers are manifold. According to (Elumilade et al., 2021), a comprehensible and hassle-free bookkeeping system improves users’ perceptions of ease of use and inclines them to fully embrace technology. This convenience enables automating tasks that involve ordinary accounting practices, such as real-time ledger updates and transaction records (Musiliu et al., 2024). Therefore, it can be stated that hassle-free bookkeeping is the attribute that establishes a rapport between Smart Ledgers and automation. Consequently, H5 is developed, which echoes the fundamental claim of TAM that the decision to utilize technology, such as smart AI-enabled or distributed ledger technology, improves automation by enabling hassle-free bookkeeping.

H5: There is a statistically significant mediating role of hassle-free bookkeeping in the relationship between Smart Ledgers and automation.

The Contingency Theory of Management Accounting presupposes that the form of accounting systems and their effectiveness depend on technological development, organizational requirements, and regulatory conditions (Bawamohiddin et al., 2023). Smart Ledgers (including DLTs) are stated to provide technological support for compliance and real-time monitoring when implemented by SMEs (Elumilade et al., 2021). However, in bookkeeping, this can only be realized when the process is effective and less complex (Narang & Jain, 2024). It can also be stated that bookkeeping facilitates this relationship by enabling an organization to process data smoothly, make timely updates, and archive documents in a well-organized fashion, which are key components of compliance in rapidly evolving regulatory environments (Pan & Lee, 2020). In this way, the H6 hypothesis is developed to suggest that Smart Ledgers do not directly contribute to real-time compliance but rather help streamline internal accounting workflows. This is in line with contingency theory, which mentions that effectiveness comes about when technologies get correspondingly aligned to organisational processes and environment.

H6: There is a statistically significant mediating role of hassle-free bookkeeping in the relationship between Smart Ledgers and real-time monitoring and compliance.

Research Gaps

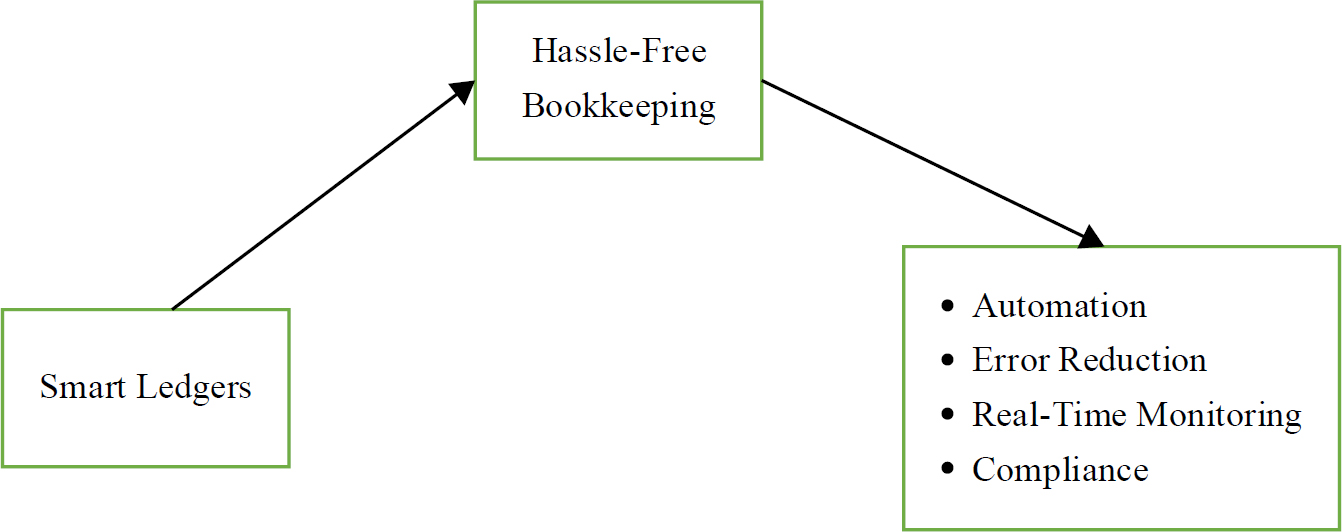

Notwithstanding the growing interest in integrating IoT, blockchain, and AI into the bookkeeping process and accounting systems, substantial research gaps persist that the current research aims to address. At first, while (Nofel et al., 2024) explore automation using smart contracts and blockchain-enabled ledgers, empirical evidence on the causal effects of smart ledgers on bookkeeping reliability and accuracy in the SME context is scarce. Secondly, while (Zhang et al., 2021) explore the significance and effect of big data analytics and XBRL on real-time updates of accounting data, ensuring accuracy and monitoring, there is a lack of amalgamated frameworks that empirically and critically assess the impact of smart ledgers on error detection, automation, and regulatory compliance. Thirdly, none of the studies above, have integrated and analysed the mediating effect of hassle-free bookkeeping driven by smart ledger adoption, resulting in error reduction, automation, and real-time monitoring, and compliance. Therefore, this study aims to bridge these research gaps by developing empirical evidence on the effectiveness of integrating smart ledgers for hassle-free bookkeeping and to drive error detection, accuracy, and compliance in the accounting process across SMEs. The study’s conceptual framework is shown in Fig. (1).

Fig. (1). Conceptual framework.

3. METHODOLOGY

The current study applied a primary data collection method by employing a survey questionnaire that contained closed-ended, structured statements to examine the integration of smart ledgers to attain error-reduction, monitoring, compliance, and automation across SMEs. According to the arguments of (Taherdoost et al., 2021), surveys are considered an effective approach to collect data on a large scale, cost-effectively, and in a timely manner.

The questionnaire (Appendix A) was designed systematically and divided into four sections. The first section contains questions related to demographic characteristics of the participants, such as age, gender, occupation, industry experience, and designation. It is followed by a second section, which assesses the implementation of smart ledger functionalities such as automated data entry, AI categorisation, and blockchain. The third section collects data related to dependent variables like error reduction, automation, and real-time compliance and monitoring. Lastly, the fourth section collects data related to the mediating variable, which is hassle-free accounting. There are three statements under every construct, which are measured on a 5-point LIKERT scaling system from strongly disagree to strongly agree as suggested by (Nofel et al., 2024; Sharma et al., 2022; and Wang et al., 2021). As indicated in the study of (Tate et al., 2023), the pilot test was done before the actual data collection and included 30 SME representatives filling out the initial version of the questionnaire. This was crucial to evaluate and improve the survey items’ clarity, validity, and reliability. Pilot test feedback guided the modification of uncertain questions. Subsequent to this, Cronbach’s alpha and composite reliability tests validated internal consistency for all constructs, as all were above the minimum acceptable value of 0.7 as suggested by (Kennedy, 2022).

The purposive sampling method is applied to target representatives of SMEs who are owners, finance, and accounts managers with experience and understanding related to digital accounting systems in the UK SMEs. This sampling technique is appraised by (Thomas, 2022) as specifically suitable for studies where insights related to a specific domain are essential. Even though the purposive sampling helped the study focus on respondents with appropriate expertise in digital accounting systems, it is associated with selection bias, whereby a purposive sampling approach does not include selecting respondents at random. As a result, the results are not likely to be completely applicable to the whole UK SME population. The method is though deemed to suit exploratory and technology-oriented research where respective knowledge of the domain is needed. In order to make the sample more relevant, the survey included screening criteria, whereby respondents had to identify themselves as owners, finance managers, or accounting professionals working in the SMEs that operated in the UK. However, the research recognises that self-reported responses were taken and they did not qualify verifying organisational affiliation on their own which could be a constraint as well as respondent authenticity. Non-probability purposive sampling restricts the extrapolation of the results and creates the possibility of selection bias. Also, since, the data were gathered by way of online self-reported responses the study was not able to confirm, by itself, that all respondents were solely associated with UK SMEs, thus, compromising the external validity of the findings.

However, aligned with the purpose sampling approach, the sample size was established by using the G*Power 3.1 software with parameters such as a 5% alpha value at a 95% confidence interval level, 5% margin of error, and 0.5 variability as mentioned by the study of (Kang, 2021). The sample size was calculated using the formula;

Where:

N = sample size

Zα/2 = Z value for the chosen confidence level (typically 1.96 for 95% confidence)

p = estimated proportion (here assumed as 0.5 for maximum variability)

E = margin of error (desired precision)

![]()

= 383

An aggregate of 700 individuals was approached on different professional networking platforms like LinkedIn and official social media pages of SMEs operating in the UK, which produced 425 initial responses with a response rate of 60.7%. Out of 425 responses, 42 responses were omitted due to missing values and outliers. Eventually, the data cleaning process led to a final sample size of 383 participants.

The survey was created in a manner that participants remained anonymous and that reverse-coded items were used for a few variables, making the results more genuine which (Venta et al., 2022) also suggested. The participants were approached using an informed consent and debrief form. They were approached through professional networks like LinkedIn, where official email addresses of the participants were obtained. Upon informed consent, the survey questionnaire link created using Google Forms was shared on their email addresses for filling out the questionnaires online. The issue of selection bias has also been addressed in the study. For instance, the professionals were contacted on professional networking platforms such as LinkedIn using its networking features, which allowed them to approach SME owners and representatives across different industrial sectors. In addition, colleagues and personal connections shared the survey within their networks, ensuring data collection of participants across different industrial sectors of SMEs.

Furthermore, the issue of non-response bias is also mitigated. Applying the approach of (Malik & Hussain, 2024), an independent sample T-test was performed to evaluate non-response bias by likening early respondents (S1 = 35) with late respondents (S2 = 35). Aligning with the findings of (Chavez et al., 2022), no statistically significant difference was unveiled across constructs, which signified comparability between early and late respondents. This signifies that non-response bias is improbable to impact the validity of collected data. An analysis using Harman’s single-factor test was performed, and the variance was found to be less than 50%; this suggests there was no major issue with common method variance.

The issue of collinearity and CMB is tested using VIF in line with its standard threshold of 3.3. As the results stated in Table 1 specifies that VIF in the context of all associations is found to be below 3.3 which articulates that there is no issue of collinearity and CMB in the model.

Table 1. Multicollinearity -VIF.

| – | VIF |

| Hassle Free Book Keeping -> Automation | 1.064 |

| Hassle Free Book Keeping -> Error Reduction | 1.064 |

| Hassle Free Book Keeping -> Real-Time Compliance and Monitoring | 1.064 |

| Smart Ledger Adoption -> Automation | 1.064 |

| Smart Ledger Adoption -> Error Reduction | 1.064 |

| Smart Ledger Adoption -> Hassle Free Book Keeping | 1.000 |

| Smart Ledger Adoption -> Real-Time Compliance and Monitoring | 1.064 |

A PLS-SEM approach was taken through SmartPLS 4.0 for the analysis of the data used in this study. Analysis was carried out in two ways: initially, a measurement model was used to assess reliability, convergent validity, internal consistency, and discriminant validity, and next, the structural model was used to determine which relationships between smart ledger adoption and bookkeeping outcomes exist. Moreover, analysis was performed starting with the measurement model to test for reliability and validity based on key indicators like Cronbach’s Alpha, Composite Reliability, Average Variance Extracted (AVE), and factor loadings. Discriminant validity was tested with the help of the HTMT ratio. All values met the standard thresholds, such as 0.7 for Cronbach’s alpha, Composite reliability, and 0.5 for AVE. Affirming the adequacy of the model. Later, path analysis was performed to examine the hypotheses introduced earlier.

4. RESULTS AND ANALYSIS

4.1. Demographic Analysis

The demographic profile of participants of the current study is presented in Table 2. As can be observed from the statistical results that out of (n = 383) participants, (55.73%) are male participants and (44.27%) are female participants, Table 2. On the other hand, with regards to the age of the participants, (33.33%) are between 26.-35 years of age, and (28.31%) of the participants are amid 36-45 years of age, Table 2. Moreover, most of the participants, that is, 25.78%, and 27.08%, were Senior Managers and Executives, respectively, Table 1. Lastly, with respect to industry experience, the maximum participants, that is (20.89%) were 3-6 years experienced, 34.99% were 7-10 years experienced, while (26.37%) of the participants held above 10 years of experience in the industry.

Table 2. Demographic analysis.

| Demographic Category | – | Frequency (n) | Percentage (%) |

| Gender | Male | 213 | 55.73% |

| Female | 170 | 44.27% | |

| Age Range | 18-25 | 70 | 18.23% |

| 26-35 | 128 | 33.33% | |

| 36-45 | 108 | 28.13% | |

| 46-55 | 77 | 20.05% | |

| Job Title/Position | Entry-Level | 100 | 26.04% |

| Middle Management | 80 | 20.83% | |

| Senior Management | 99 | 25.78% | |

| Executive | 104 | 27.08% | |

| Department | Finance | 72 | 18.75% |

| Accounting | 126 | 32.81% | |

| IT | 92 | 23.96% | |

| Operations | 93 | 24.22% | |

| Industry Experience | 1-2 years | 68 | 17.75% |

| 3-6 years | 80 | 20.89% | |

| 7-10 years | 134 | 34.99% | |

| Above 10 years | 101 | 26.37% |

4.2. Measurement Model Using Confirmatory Factor Analysis (CFA)

Reliability and validity of the measurement model were evaluated with several indicators that include Cronbach’s Alpha, Composite Reliability, and Average Variance Extracted (AVE), Table 3. The findings exhibited satisfactory internal consistency and construct reliability with all the measures above the predefined threshold values, thus establishing the adequacy and strength of the measurement model for additional structural analysis.

Table 3. Measurement model.

| Latent Variables | Indicators | Factor Loadings | Cronbach’s Alpha | Composite Reliability | Average Variance Extracted (AVE) |

| Automation | A1 | 0.900 | 0.883 | 0.892 | 0.811 |

| A2 | 0.930 | ||||

| A3 | 0.870 | ||||

| Error Reduction | ER1 | 0.791 | 0.812 | 0.826 | 0.727 |

| ER2 | 0.902 | ||||

| ER3 | 0.863 | ||||

| Hassle Free Book Keeping | HFBK1 | 0.906 | 0.894 | 0.901 | 0.826 |

| HFBK2 | 0.931 | ||||

| HFBK3 | 0.888 | ||||

| Real-Time Compliance and Monitoring | RTCM1 | 0.911 | 0.901 | 0.902 | 0.835 |

| RTCM2 | 0.928 | ||||

| RTCM3 | 0.902 | ||||

| Smart Ledger Adoption | SLA1 | 0.876 | 0.852 | 0.853 | 0.772 |

| SLA2 | 0.902 | ||||

| SLA3 | 0.857 |

The validity and reliability of the construct and data collection instruments used in the research depend on the measurement model, which applies Confirmatory Factor Analysis (CFA), which is comprised of factor loadings, composite reliability, Cronbach’s alpha, and average variance extracted (AVE). From the results established in Table 3, it can be observed that the construct Automation depicts greater strength in terms of factor loading, which varies from 0.870-0.930, the Cronbach’s alpha (0.883), and the Composite Reliability value (0.892) also surpasses threshold of 0.7 which specifies a good reliability score. Also, AVE is 0.811, exceeding the threshold of 0.5, which shows good convergent validity.

Similarly, in the case of another construct that is Error Reduction, higher factor loading is observed (0.902) among its dimensions, with a range (0.791-0.902). The variable validity and reliability have also been attained with Cronbach’s Alpha value found to be (0.812) and Composite Reliability Value observed to be (0.826). The construct is also found with strong convergent validity with AVE value (0.7270 surpassing the threshold value of 0.5. Furthermore, Hassle Free Book Keeping collects data points amid 0.888 and 0.931, which depicts significant internal consistency (Cronbach’s Alpha = 0.894) and Composite Reliability (0.901). The AVE of (0.826) provisions sturdy convergent validity.

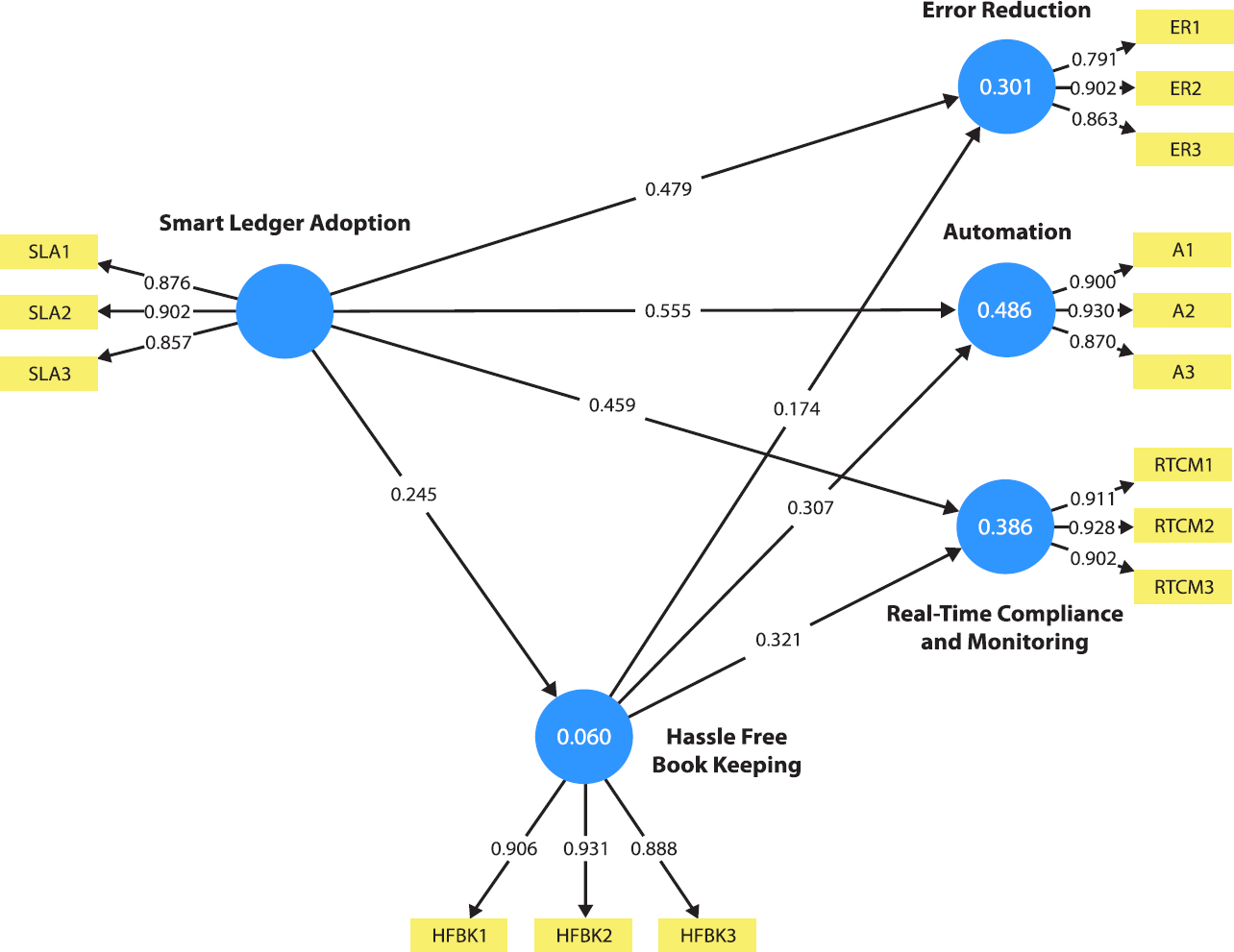

Real-Time Compliance and Monitoring exhibits measurements amid 0.902 to 0.928, and it evidences robust internal consistency (Cronbach’s Alpha = 0.901) and Composite Reliability (0.902). The AVE value of (0.835) also specifies robust convergent validity. The factor loadings of Smart Ledger Adoption range from 0.857 to 0.902, at the same time depicting both Cronbach’s Alpha (0.852) and Composite Reliability (0.853), which shows robust internal consistency. The AVE of (0.772) exhibits greater convergent validity in the research. (Fig. 2) offers the pictorial representation of the measurement model of the research.

Fig. (2). Measurement model.

4.3. Discriminant Validity

Heterotrait-Monotrait Ratio (HTMT) was applied to evaluate discriminant validity as stressed in the arguments of (Rönkkö & Cho, 2022). The values of HMT are discussed in Table 4, which identifies separability and distinctiveness between variables.

Table 4. Discriminant validity.

| – | Automation | Error Reduction | Hassle Free Book Keeping | Real-Time Compliance and Monitoring |

| Error Reduction | 0.550 | – | – | – |

| Hassle Free Book Keeping | 0.494 | 0.343 | – | – |

| Real-Time Compliance and Monitoring | 0.734 | 0.468 | 0.478 | – |

| Smart Ledger Adoption | 0.720 | 0.621 | 0.278 | 0.613 |

The highest value is identified amid Automation and Real-Time Compliance and Monitoring with an HMT value of (0.734), and amid Smart Ledger Adoption and Automation with an HMT value of (0.720), which is still lower than 0.85 indicating presence of discriminant validity in Table 4. The lowest value observed is 0.278 amid Smart Ledger Adoption and Hassle-Free Bookkeeping in Table 3 which depicts the least overlap and robust independence in the conceptual model. From these results of discriminant validity is indicated that the variables which are comprised of Smart Ledger Adoption, Automation, Error Reduction, Real-Time Compliance and Monitoring, and Hassle-Free Bookkeeping are distinct conceptually and are suitably different within the model of the study, hence, it provisions that the structural model is valid for further analysis of causality amid identified variables.

4.4. Path Analysis

The statistical results of path coefficient analysis signify positive as well as statistically significant causality among primary constructs of the current study, which also provisions the hypothesised conceptual model. As the results presented in Table 5, the construct Smart Ledger Adoption is observed to show a direct effect on all three target variables. For instance, the results of path analysis exhibit a statistically significant relationship among Smart Ledger Adoption and Automation, strongest (β = 0.555; p = 0.001), which also highlights that the integration of Smart Ledgers increases automation in the bookkeeping process within SMEs. In a similar vein, Error Reduction and Real-Time Compliance and Monitoring are also revealed to be statistically significantly related with Smart Ledger integration at SMEs β = 0.479; p = 0.001) and (β = 0.459; p = 0.001). These results indicate that Smart Ledger, integrated with blockchain technologies, plays a crucial role in decreasing human error and allows for regulatory and monitoring while bookkeeping within SMEs.

Table 5. Structural model-cause and effect analysis.

| – | Path coefficients | T-Statistics | P-Values | f-Square |

| Hassle Free Book Keeping -> Automation | 0.307*** | 6.537 | 0.000 | 0.173 |

| Hassle Free Book Keeping -> Error Reduction | 0.174*** | 3.027 | 0.002 | 0.041 |

| Hassle Free Book Keeping -> Real-Time Compliance and Monitoring | 0.321*** | 4.961 | 0.000 | 0.158 |

| Smart Ledger Adoption -> Automation | 0.555*** | 14.017 | 0.000 | 0.562 |

| Smart Ledger Adoption -> Error Reduction | 0.479*** | 10.932 | 0.000 | 0.308 |

| Smart Ledger Adoption -> Hassle-Free Bookkeeping | 0.245*** | 4.063 | 0.000 | 0.064 |

| Smart Ledger Adoption -> Real-Time Compliance and Monitoring | 0.459*** | 9.748 | 0.000 | 0.323 |

| Specific Indirect Effects | ||||

| Smart Ledger Adoption -> Hassle Free Book Keeping -> Automation | 0.075*** | 3.245 | 0.001 | |

| Smart Ledger Adoption -> Hassle Free Book Keeping -> Error Reduction | 0.043** | 2.303 | 0.021 | |

| Smart Ledger Adoption -> Hassle Free Book Keeping -> Real-Time Compliance and Monitoring | 0.079*** | 2.89 | 0.004 | |

Note: **: Significance at 5%; ***: Significance at 1%

In addition, it has also been indicated by the results that integration of Smart Ledgers positively and statistically significantly associated with the mediating construct that is Hassle-Free Bookkeeping (β = 0.245; p = 0.001). These results stress that through the integration of Smart Ledgers at SMEs, accounting and bookkeeping processes are facilitated and simplified. Moreover, in terms mediating effect, Hassle-Free Bookkeeping positively and significantly relates with all three target constructs. The results indicate that the path towards Automation and β = 0.307; p = 0.001) and Real-Time Compliance and Monitoring (β = 0.321; p = 0.001) is significant, where the path towards Error Detection is observed to be moderate (β = 0.174; p = 0.002). Hence, it can be said that these results provide the mediating role of Hassle-Free accounting and Bookkeeping in the association amongst integrated Smart Ledgers, Error Reduction, Automation, and Monitoring and Compliance within SMEs.

The results in Table 4 also depict that Hassle-Free Bookkeeping partially mediates the association among Smart Ledger Adoption, Automation, Error Reduction, and Real-time Monitoring and Compliance. All indirect effects are statistically significant, where the P-values are found below 0.05, which confirms the mediating role of Hassle-free bookkeeping. On the other hand, it has also been unveiled by the results that the direct path from Smart Ledger Adoption to Error Reduction, Automation, and Real-time Compliance also remains significant, which indicates that mediation is partial instead of full, indicating both direct and indirect effects of Smart Ledger Adoption, through Hassle-free Bookkeeping on Error Reduction, Automation, and Real-time Compliance in the case of UK SME context. Finally, the result of the f-square (f2) suggests that the relationships in the model have different levels of significance. Smart Ledger Adoption has a high impact on the Automation (f2 = 0.562) and a moderate impact on the Error Reduction (f2 = 0.308) and the Real-Time Compliance and Monitoring (f2 = 0.323). Hassle-Free Bookkeeping indicates a modest impact on Automation (f2 = 0.173) and Real-Time Compliance (f2 = 0.158) and a weak impact on Error Reduction (f2 = 0.041). Also, the impact of Smart Ledger Adoption on Hassle-Free Bookkeeping is a minor effect (f2 = 0.064).

4.5. Model Explanatory Power

R-squared and adjusted R-squared values were both examined against each of the dependent constructs in making the evaluations of the explanatory power of the model Table 6. R-squared shows the percentage of the variance in the dependent variable that is described by its predictors, whereas adjusted R-squared takes into consideration the model complexity and the size of the sample (Ozili, 2023). The greater the value of R-squared, the greater is the explanatory power (Hayes, 2021). The findings of Table 6 could present an understanding of the predictive adequacy of the model, as summarising the results of R-squared of Automation, Error Reduction, Hassle-Free Bookkeeping, and Real-Time Compliance and Monitoring variables. The value of R-squared depicted in Fig. (2) and Table 4, which signifies that 6% of the variation in hassle-free bookkeeping is explained by Smart Ledgers. While Smart Ledgers explains (30.1%) of the variation in Error Reduction, (48.6%) in Automation, and (38.6%) in Real-Time Compliance and Monitoring in SMEs.

Table 6. R-square table.

| – | R-Square | R-Square Adjusted |

| Automation | 0.486 | 0.483 |

| Error Reduction | 0.301 | 0.297 |

| Hassle Free Book Keeping | 0.060 | 0.057 |

| Real-Time Compliance and Monitoring | 0.386 | 0.383 |

5. DISCUSSION AND HYPOTHESES ASSESSMENT

The study investigated how the adoption of Smart Ledger can influence bookkeeping functions of SMEs, especially in terms of improving automation, reducing errors, and ensuring real-time monitoring and compliance, while considering hassle-free bookkeeping as a mediating variable. Empirical evidence proves that four hypotheses are accepted, which evidence that smart ledger systems play a key role in the digital shift of SME accounting operations and making it efficient. Smart ledgers are evidenced as significant in making bookkeeping hassle-free and reliable. This result agrees with the arguments of (Bawamohiddin et al., 2023) that smart ledgers are precise in keeping digital records of accounting and financial data. The results reveal that smart ledgers are effective in improving the bookkeeping accuracy, minimization of errors, automation, and real-time compliance.

Considered through the perspective of the Resource-Based View (RBV), smart ledgers are a powerful organisational asset, as they help SMEs to streamline their resources and enhance reporting quality and compliance efficiency. On the other hand, the Technology Acceptance Model (TAM) also supports these findings as perceived usefulness and ease of the using AI-powered smart ledgers impacts the willingness of accountants to implement these systems. Therefore, the combined theoretical viewpoints illustrate why smart ledgers leads to efficiency and reliability in the accounting practices of UK SMEs. However, some of the previous studies, such as those carried out by (Elumilade et al., 2021; and Narang & Jain, 2024) signified feeble impacts, usually due to reasons of contextual industrial factors which are comprised of compliance pressures specific to industries, admittance to digital infrastructures particularly in the developing economies unlike UK, lack of financial resources and the complexity of financial transactions.

On the other hand, unlike larger firms or heavily regulated firms, several SMEs in the UK face a lack of advanced IT systems due to financial constraints, which tends to impact the implementation of Smart AI-enabled ledgers (Malik & Hussain, 2024). Therefore, these findings imply for UK SMEs that to fully advantage from AI-enabled bookkeeping technologies, a supportive framework and available digital tools should be prioritised. These findings signify that SMEs operating in the UK, unlike larger commercial enterprises usually lack the financial capacity to make investments in advanced IT systems which restricts the implementation of AI-enabled Smart ledgers. From the viewpoint of RBV theory, constraints related to resources deteriorates ability of the SMEs to construct digital capabilities. On the other hand, TAM specifies that restricted perceived ease of using Smart ledgers deprived of adequate infrastructure. Therefore, maximise advantages of AI-enabled Smart ledgers, policy support, subsidised digital tools and customised frameworks are mandator for allowing SMEs to embrace the adoption of smart ledger technologies in their accounting systems to enhance error reduction and ensuring real-time monitoring and compliance.

In addition, Smart Ledger is considered a key factor in the reduction of manual accounting errors, which is also supported in the study of (Musiliu et al., 2024) about the benefits of blockchain. Furthermore, indicating that smart ledgers make real-time reporting and complete transparency possible, in line with conclusions drawn by (Dashkevich et al., 2024). It has also been affirmed by this study that the adoption of Smart AI-enabled ledgers substantially decreases accounting errors and improves transparency, along with real-time monitoring. However, different results, in the context of other regions highlighted in (Arabi, 2024) originate from the readiness of the industries, regulatory environment, financial pressures, and digital capabilities. In the context of UK SMEs, restricted access to blockchain infrastructure to SMEs and reduced technological amalgamation tend to hinder the complete adoption of Smart AI-enabled ledgers, which signifies the need for supportive digital transformation policies and adequate financial resources to bridge this technological adoption gap.

Moreover, the study results have also unveiled a statistically significant and partial mediating impact of hassle-free bookkeeping in the relationship amid smart ledgers, error reduction, automation, and real-time compliance and monitoring. These findings also support the articulations made by (Azman et al., 2021) that less complicated processes of bookkeeping obtained through smart ledgers allow better data distribution and decision-making in SMEs, which makes the accounting process error-free, accurate, and compliant with regulatory standards. The results signify that hassle-free bookkeeping partially mediates the association amid Smart ledgers, automation, error reduction and real-time and monitoring and compliance. These findings align with the arguments of (Musiliu et al., 2024) who also stressed that simplified procedures enhance regulatory compliance and accuracy of financial records. From the TAM viewpoint, ease of use improves user acceptance of Smart ledgers, which leads to reliable financial transparency outcome in terms of automation, error reduction and compliance with reporting requirements. Likewise, the RBV theory also signifies efficiency of bookkeeping as strategic capability that enhance competitiveness of SME by allowing accurate financial reporting, regulatory compliance and automation. Thus, mediation depicts ways that streamlined procedures act as important mechanisms connecting adoption of technology to enhanced accounting transparency outcomes.

CONCLUSION

The study analysed the integration and use of AI-driven smart ledgers in small and medium-sized companies (SMEs) in the UK, paying specific focus to its influences on automation, error reduction, and real-time compliance checks, where hassle-free bookkeeping served as a significant mediator. It was confirmed by the findings that smart ledger technology boosts automation, slashes accounting errors, and allows for meeting monitoring and compliance requirements in real-time. Likewise, hassle-free bookkeeping processes were found to boost and help to develop accounting process automated and convenient accounting process. It appears that, in addition to making bookkeeping more efficient, smart ledgers play a key role in SMEs’ digital transformation of financial reporting processes.

Blockchain-driven accounting systems are trusted since the evidence shows they can make business procedures more efficient and transparent. This study fills a gap in the research by proving how smart ledger technology helps small and medium businesses in making their bookkeeping process hassle-free and reducing accounting errors. As a result, it gives helpful information to businesses and companies that aim to advance their financial management. Automated and user-friendly ledger systems should be given priority to avoid errors and follow all the regulatory rules. All in all, adopting smart ledgers paves the way for the UK SMEs to challenge traditional accounting methods, become more sustainable, flexible, and strong and efficient.

FUTURE IMPLICATIONS

This study has vital implications for SMEs who aim to update their accounting and bookkeeping practices in the future. Since smart ledgers are proven to help with automation, fewer mistakes in accounting, and real-time tracking of compliance, companies can use smart ledgers to make their bookkeeping operations more efficient. Due to the constant changes in taxes and financial reporting, up-to-date compliance given by smart ledgers allows SMEs to ensure regulatory compliance. Moreover, user-friendliness in bookkeeping demonstrates how SMEs can devote their efforts to major development and planning. These findings imply that AI-based ledger technologies ought to be part of the main plans for transforming businesses digitally. Besides, SME-oriented ledger systems are needed that can be adjusted and scaled by developers and vendors of financial technologies for different SME sectors. They can also use them to offer bookkeeping training and technical support to encourage more digital adoption in the function of bookkeeping. It is also possible that future studies could look into the unique effects of smart ledgers on specific industries or over time, which would benefit discussions about digital accounting processes and effective and efficient financial reporting within SMEs.

POLICY IMPLICATIONS

The findings indicate that AI-based smart ledger is linked with automation, reduction of errors, and real time compliance among the UK SMEs. Relying on these findings, policymakers can consider of gradual adoption of digital accounting technologies by making awareness and access to suitable infrastructure availability. Instead of general prescriptions of massive changes in regulations, the study suggests the possible benefits of promoting best practices in the processes of digital bookkeeping and compliance. This is measured support that would assist SMEs to increase operational efficiency and transparency besides adapting to the changing needs of digital accounting.

LIST OF ABBREVIATIONS

AVE | = | Average Variance Extracted |

DLT | = | Distributed Ledger Technology |

MTD | = | Making Tax Digital |

RBV | = | Resource-Based View |

SEM | = | Structural Equation Modeling |

SMEs | = | Small and Micro Business Enterprises |

TAM | = | Technology Acceptance Model |

AUTHOR’S CONTRIBUTION

A.S. has contributed to conceptualization, idea generation, problem statement, methodology, results analysis, results interpretation.

ETHICAL STATEMENT & INFORMED CONSENT

All procedures were conducted in compliance with the guidelines of the institutional research ethics committee and adhered to the principles outlined in the Declaration of Helsinki. Informed consent was obtained from all participants prior to their inclusion in the study. To protect participant confidentiality, all data were anonymized at the time of collection, and no personally identifiable information was recorded.

AVAILABILITY OF DATA AND MATERIALS

The data will be made available on reasonable request by contacting the corresponding author [A.S.].

FUNDING

None.

CONFLICT OF INTEREST

The author declares no conflicts of interest, financial or otherwise.

ACKNOWLEDGEMENTS

Declared none.

DECLARATION OF AI

During the preparation of this manuscript, the author used ChatGPT for language polishing. After utilizing this tool, the author carefully reviewed and refined the content as necessary and accept full responsibility for the accuracy and integrity of the published work.

APPENDIX A

Item | Response |

Age | ☐ 18–25 ☐ 26–35 ☐ 36–45 ☐ 46–55 |

Gender | ☐ Male ☐ Female ☐ Other ☐ Prefer not to say |

Job Position | ☐ Entry-level ☐ Middle Management ☐ Senior Management ☐ Executive |

Department | ☐ Finance ☐ Accounting ☐ IT ☐ Operations |

Years of Experience in Industry | ☐ 1–2 years ☐ 2–6 years ☐ 7–10 years ☐ Above 10 years |

Five-point Likert Scale from Strongly Disagree (1) to Strongly Agree (5).

Section B: Smart Ledger Adoption (Independent Variable) | |||||

Statement | 1 | 2 | 3 | 4 | 5 |

1. Our firm uses AI or smart technologies to automate ledger preparation. | ☐ | ☐ | ☐ | ☐ | ☐ |

2. Smart ledger systems in our firm integrate technologies like blockchain and machine learning. | ☐ | ☐ | ☐ | ☐ | ☐ |

3. The smart ledger we use supports real-time synchronisation of financial records. | ☐ | ☐ | ☐ | ☐ | ☐ |

Section C: Error Reduction (Dependent Variable) | 1 | 2 | 3 | 4 | 5 |

Statement | |||||

4. The use of smart ledgers has significantly reduced manual errors in our bookkeeping. | ☐ | ☐ | ☐ | ☐ | ☐ |

5. Ledger automation helps in early detection of anomalies and financial inconsistencies. | ☐ | ☐ | ☐ | ☐ | ☐ |

6. Our accounting records are more accurate since adopting smart ledger systems. | ☐ | ☐ | ☐ | ☐ | ☐ |

Section D: Automation (Dependent Variable) | 1 | 2 | 3 | 4 | 5 |

Statement | |||||

7. Our routine accounting tasks are largely automated using AI-led ledger systems. | ☐ | ☐ | ☐ | ☐ | ☐ |

8. Smart ledgers have minimised the need for repetitive manual entries. | ☐ | ☐ | ☐ | ☐ | ☐ |

9. Automation has improved operational speed in generating financial reports. | ☐ | ☐ | ☐ | ☐ | ☐ |

Section E: Real-Time Compliance Monitoring (Dependent Variable) | 1 | 2 | 3 | 4 | 5 |

Statement | |||||

10. Our system allows for real-time monitoring of compliance with accounting standards. | ☐ | ☐ | ☐ | ☐ | ☐ |

11. Smart ledgers assist us in meeting regulatory requirements timely. | ☐ | ☐ | ☐ | ☐ | ☐ |

12. Real-time alerts and updates enhance our compliance capabilities. | ☐ | ☐ | ☐ | ☐ | ☐ |

Section F: Hassle-Free Bookkeeping (Mediator Variable) | 1 | 2 | 3 | 4 | 5 |

Statement | |||||

13. Bookkeeping has become simpler and less time-consuming with smart ledger integration. | ☐ | ☐ | ☐ | ☐ | ☐ |

14. Our accounting staff experience less stress and burden during bookkeeping tasks. | ☐ | ☐ | ☐ | ☐ | ☐ |

15. Smart ledger systems have streamlined our bookkeeping processes. | ☐ | ☐ | ☐ | ☐ | ☐ |

REFERENCES

Aarti, D., (2025). AI in Accounting Market Size, Share Report, Growth 2034| MRFR. Available from: https://www.marketresearchfuture.com/reports/ai-in-accounting-market-22351.

Adekunle, B. I., Chukwuma-Eke, E. C., Balogun, E. D., & Ogunsola, K. O. (2023). Developing a digital operations dashboard for real-time financial compliance monitoring in multinational corporations. International Journal of Scientific Research in Computer Science, Engineering and Information Technology, 9(3), 728-746. Available from: https://ijsrcseit.com/paper/CSEIT23112546.pdf.

Arabi, N. (2024). The technological metamorphosis of accounting and auditing: From automation to the metaverse. International Journal of Engineering Technology Research & Management (IJETRM), 8(11), 432-440. Available from: https://ijetrm.com/issues/files/Apr-2024-29-1745901578-NOV202458.pdf.

Azman, N. A., Mohamed, A., & Jamil, A. M. (2021). Artificial intelligence in automated bookkeeping: a value-added function for small and medium enterprises. JOIV: International Journal on Informatics Visualization, 5(3), 224-230. https://dx.doi.org/10.30630/joiv.5.3.669.

Bawamohiddin, A. B., Mohamad, H., & Muhamad, A. N. (2023). Digitize the eCommerce Bookkeeping–An Automation Bookkeeping Prototype Development. Malaysian Journal of Information and Communication Technology (MyJICT), 8(2) 100-111. https://doi.org/10.53840/myjict8-2-100.

Bloom Financials (2025). MTD for UK SMEs in 2025: Compliance, Deadlines & Tools. Bloom Financials. Available from: https://bloomfinancials.com/making-tax-digital-smes-2025/#:~:text=Making%20Tax%20Digital%20(MTD)%20works,declaration%20through%20MTD%2Dcompatible%20software.

Chou, C. C., Hwang, N. C. R., Schneider, G. P., Wang, T., Li, C. W., & Wei, W. (2021). Using smart contracts to establish decentralized accounting contracts: An example of revenue recognition. Journal of Information Systems, 35(3), 17-52. https://doi.org/10.2308/ISYS-19-009.

Chavez, R., Malik, M., Ghaderi, H., & Yu, W. (2023). Environmental collaboration with suppliers and cost performance: Exploring the contingency role of digital orientation from a circular economy perspective. International Journal of Operations & Production Management, 43(4), 651-675. https://doi.org/10.1108/IJOPM-01-2022-0072.

Darma, J., Hidayat, T., Sitompul, H. P., Syah, D. H., & Sagala, G. H. (2021). Small-Medium Enterprises Stickiness on the Traditional Accounting Systems. Proceedings of the International Conference on Strategic Issues of Economics, Business and, Education (ICoSIEBE 2020) (pp. 40-44). Atlantis Press. https://doi.org/10.2991/aebmr.k.210220.008.

Dashkevich, N., Counsell, S., & Destefanis, G. (2024). Blockchain financial statements: Innovating financial reporting, accounting, and liquidity management. Future Internet, 16(7), 244. https://doi.org/10.3390/fi16070244.

Demirkan, S., Demirkan, I., & McKee, A. (2020). Blockchain technology in the future of business cyber security and accounting. Journal of Management Analytics (Vol. 7, Issue 2, pp. 189–208). Taylor and Francis Ltd. https://doi.org/10.1080/23270012.2020.1731721.

Elumilade, O. O., Ogundeji, I. A., Achumie, G. O., Omokhoa, H. E., & Omowole, B. M. (2021). Enhancing fraud detection and forensic auditing through data-driven techniques for financial integrity and security. Journal of Advanced Education and Sciences, 1(2), 55-63. https://doi.org/10.54660/.JAES.2021.1.2.55-63.

Grigg, I. (2024). Triple entry accounting. Journal of Risk and Financial Management, 17(2), 76. https://doi.org/10.3390/jrfm17020076.

Hayes, T. (2021). R-squared change in structural equation models with latent variables and missing data. Behavior Research Methods, 53(5), 2127-2157. https://doi.org/10.3758/s13428-020-01532-y.

Kabir, M. F., Rana, M. I. C., & Rahman, M. A. (2025). The role of information technology in improving the accuracy and efficiency of accounting data. International Journal on Science and Technology (IJSAT), 16(1), 1. https://doi.org/10.71097/IJSAT.v16.i1.2045.

Kang, H. (2021). Sample size determination and power analysis using the G* Power software. Journal of educational evaluation for health professions, 18. https://doi.org/10.3352/jeehp.2021.18.17.

Kennedy, I. (2022). Sample size determination in test-retest and Cronbach alpha reliability estimates. British Journal of Contemporary Education, 2(1), 17-29. http://dx.doi.org/10.52589/BJCE-FY266HK9.

Malik, A., & Hussain, T. (2024). AIS Digital Accounting Systems and their Impact on Audit Quality and Tax Regulation Compliance. Asian American Research Letters Journal, 1(6). https://doi.org/10.5281/r8abae85.

Mouka, M. (2025) The hidden struggles of UK SMEs during tax season, Accountancy Age. Available from https://www.accountancyage.com/2025/01/27/the-hidden-struggles-of-uk-smes-during-tax-season/.

Musiliu, S. B., Mlanga, S., & Oriakpono, A. E. (2024). Distributed Ledger Technology and Financial Reporting Integrity in Nigerian Quoted Banks: A Study on Error Reduction and Enhanced Transparency. African Journal of Accounting and Financial Research, 7(4), 16-35. https://www.doi.org/10.52589/AJAFR-D4MTG09N.

Narang, S., & Jain, M. K. (2024). Revolutionizing Accounting: Financial Reporting Transformation with Automation and AI. MAHARAJA SURAJMAL INSTITUTE, 7(1), 33. Available from: https://msijr.msi-ggsip.org/papers/vol7issue1/7_1_7.pdf.

Nofel, M., Marzouk, M., Elbardan, H., Saleh, R., & Mogahed, A. (2024). From sensors to standardized financial reports: A proposed automated accounting system integrating IoT, Blockchain, and XBRL. Journal of Risk and Financial Management, 17(10), 445. https://doi.org/10.3390/jrfm17100445.

Noori Doabi, P. (2024). A Scientific Framework of Automated Accounting and Auditing on the Blockchain Technology Platform. Available at SSRN 5064655. https://dx.doi.org/10.2139/ssrn.5064655.

Ozili, P. K. (2023). The acceptable R-square in empirical modelling for social science research. Social research methodology and publishing results, Available at SSRN 5064655. https://dx.doi.org/10.2139/ssrn.4128165.

Pan, G., & Lee, B. (2020). Leveraging digital technology to transform accounting function: case study of a SME. International Journal of Accounting and Financial Reporting, 10(2), 24. https://doi.org/10.5296/ijafr.v10i2.17052.

Rönkkö, M., & Cho, E. (2022). An updated guideline for assessing discriminant validity. Organizational research methods, 25(1), 6-14. https://doi.org/10.1177/1094428120968614.

Roszkowska, P. (2021). Fintech in financial reporting and audit for fraud prevention and safeguarding equity investments. Journal of Accounting & Organizational Change, 17(2), 164-196. https://doi.org/10.1108/JAOC-09-2019-0098.

Sanad, Z. (2024). Does XBRL adoption eliminate misclassification of income statement items? Journal of Financial Reporting and Accounting, 22(2), 433-449. https://doi.org/10.1108/JFRA-03-2023-0147.

Sanay (2025). 9 Common SME Accounting Mistakes?9 Common SME Accounting Mistakes. Jonathan Carling, Sanay Ltd. Available from: https://www.sanaybpo.com/blog/are-you-making-these-9-common-sme-accounting-mistakes.

Sarwar, M. I., Khan, I., & Alyas, T. (2023). Triple-Entry Accounting (TEA) and Blockchain Implementation in Accounting and Finance-A Survey. http://dx.doi.org/10.13140/RG.2.2.25359.36003.

Shalhoob, H., Halawani, B., Alharbi, M., & Babiker, I. (2024). The impact of big data analytics on the detection of errors and fraud in accounting processes. RGSA: Revista de Gestão Social e Ambiental, 18(1), 121. https://doi.org/10.24857/rgsa.v18n1-121.

Sharma, A., Bhanawat, S. S., & Sharma, R. B. (2022). Adoption of Blockchain Technology Based Accounting Platform. Academic Journal of Interdisciplinary Studies, 11(2), 155–162. https://doi.org/10.36941/ajis-2022-0042.

Singh, A. (2025) The Future of Accounting: How AI and Automation are Changing the Profession. International Journal for Multidisciplinary Research, 7(2), 39838. https://doi.org/10.36948/ijfmr.2025.v07i02.39838.

Taherdoost, H. (2021). Data collection methods and tools for research; a step-by-step guide to choose data collection technique for academic and business research projects. International Journal of Academic Research in Management (IJARM), 10(1), 10-38. Available from: https://hal.science/hal-03741847v1.

Tate, R., Beauregard, F., Peter, C., & Marotta, L. (2023). Pilot Testing as a Strategy to Develop Interview and Questionnaire Skills for Scholar Practitioners. Impacting Education: Journal on Transforming Professional Practice, 8(4), 20–25. https://doi.org/10.5195/ie.2023.333.

Thomas, F. B. (2022). The role of purposive sampling technique as a tool for informal choices in a social Sciences in research methods. Just Agriculture, 2(5), 1-8. Available from: https://justagriculture.in/files/newsletter/2022/january/47.%20The%20Role%20of%20Purposive%20Sampling%20Technique%20as%20a%20Tool%20for%20Informal%20Choices%20in%20a%20Social%20Sciences%20in%20Research%20Methods.pdf.

Venta, A., Bailey, C. A., Walker, J., Mercado, A., Colunga-Rodriguez, C., Ángel-González, M., & Dávalos-Picazo, G. (2022). Reverse-coded items do not work in Spanish: Data from four samples using established measures. Frontiers in Psychology, 13, 828037. https://doi.org/10.3389/fpsyg.2022.828037.

Wang, X., Bu, L., & Peng, X. (2021). Internet of things adoption, earnings management, and resource allocation efficiency. China Journal of Accounting Studies, 9(3), 333-359. https://doi.org/10.1080/21697213.2021.2009180.

Weigel, C., & Hiebl, M. R. (2023). Accountants and small businesses: toward a resource-based view. Journal of Accounting & Organizational Change, 19(5), 642-666. https://doi.org/10.1108/JAOC-03-2022-0044.

Xu, R., Hang, L., Jin, W., & Kim, D. (2021). Distributed secure edge computing architecture based on blockchain for real-time data integrity in IoT environments. Actuators, 10(8), 197. https://doi.org/10.3390/act10080197.

Zhang, Y., Pourroostaei Ardakani, S., & Han, W. (2021). Smart ledger: The blockchain‐based accounting information recording protocol. Journal of Corporate Accounting & Finance, 32(4), 147-157. https://doi.org/10.1002/jcaf.22515.

Latest Articles

Author Ishaq Kalanther1 ,* 1Jubail Industrial College, Jubail Industrial City, Jubail, Kingdom of Saudi Arabia Article History: Received: 09 February,...

Author Abu-Shariq1 ,* 1Jubail Industrial College, Jubail, Kingdom of Saudi Arabia Article History: Received: 09 February, 2026 Accepted: 08 April,...