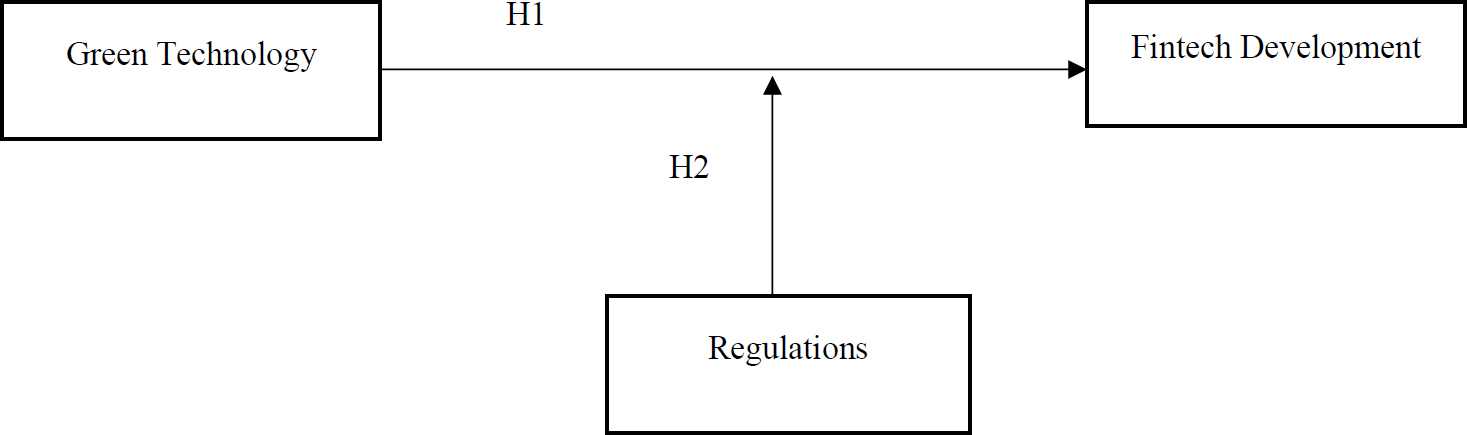

Impact of Green Technology on Fintech Development: Moderating Role of Regulations

PDF

PDF

3. RESEARCH METHODOLOGY

3.1. Sample and Data Collection

This research explores the effect of green technology on fintech development, with an emphasis on the moderating role of regulations in developing Asian nations, using a quantitative approach. The quantitative technique was utilised consistently with previous studies, such as (Li et al., 2024; Xue et al., 2022; and Zhe et al., 2024), to verify the hypothesis using scientific methods. The sample consists of 25 countries categorised by the Australian Government’s Department of Foreign Affairs and Trade (DFAT) as developing in the Asian region. The data is collected from 2010 to 2024 to cover more than a decade of Fintech and green technology development. The period is reasonable, as it covers major global and regional milestones, such as the emergence of mobile financial services, increased awareness of climate change, and the enactment of significant green technology policies and the Sustainable Development Goals (SDGs). The post-2010 period also signifies the wave of digitalisation and rule-making innovations in developing economies (Abbas & Najam, 2024). Data were drawn from the World Bank’s World Development Indicators (WDI) and the IEA Energy Technology Patents Data Explorer, which provide a sound, unidimensional dataset.

3.2. Variable Measurement

3.2.1. Dependent Variable: Fintech Development

Fintech Development in this research is quantified using a composite Fintech Index (FI) constructed via a two-stage Principal Component Analysis (PCA) approach, as described by (Zheng et al., 2024). The index reflects three essential dimensions: Access, Usage, and Digital Infrastructure as shown in Table 1. The Access dimension captures people’s ability to access digital financial services; Usage captures how intensively they use such services; and Digital Infrastructure captures the technological landscape that facilitates Fintech adoption. All indicators are normalised on a 0–1 scale to avoid scale differences between countries and over time. PCA is subsequently used within each dimension and then across dimensions to provide objective weights based on variance explained (Tram et al., 2023). This method avoids the subjectivity inherent in indiscriminate weighting and provides a balanced, data-driven measure of Fintech progress. The dimensions considered in this study followed those of (Zheng et al., 2024), and the PCA analysis yielded three dimensions with eigenvalues greater than 1; hence, three dimensions have been used to develop the index.

Table 1. Financial development index dimensions.

| Dimension | Indicators | Reference | Source |

| Access | Mobile Money Account | (Tram et al., 2023; and Zheng et al., 2024) | World Bank Findex |

| Own a Mobile Money Account | |||

| Internet Access | |||

| Usage | Saving from mobile money | ||

| Borrowed Money from Mobile Money | |||

| Made Digital Payment | |||

| Received digital payment | |||

| Made digital payment for instore purchase | |||

| Digital Infrastructure | Use of Internet for purchases | ||

| Internet use for accessing account |

3.2.2. Other Variables

Table 2 below provides descriptions of the key variables. Green Technology is quantified by the total number of patents awarded for energy technologies, reflecting innovation in green energy solutions. The variable adopts the methodology of (Li et al., 2024) and is derived from the IEA Energy Technology Patents Data Explorer. Energy Consumption is a measure of renewable energy consumption as a proportion of GDP, indicating the extent to which green energy contributes to the economy. This is adopted from (Hou et al., 2024) and sourced from the World Development Indicators. Economic Growth is measured by annual GDP growth (%) to capture macroeconomic performance. The moderating variable, regulation, was measured using the CPIA policy and institutional rating for environmental sustainability, as adopted from (Xia & Liu, 2024). The data for this is obtained from the World Development Indicators.

Table 2. Variable description.

| Variable | Description | Reference | Source |

| Green Technology | Number of Patents for Energy Technology | (Li et al., 2024) | IEA Energy Technology Patents Data Explorer |

| Energy Consumption | Energy use (kg of oil equivalent per capita) | (Hou et al., 2024) | World Development Indicators |

| Economic growth | GDP Growth (%) | (Hou et al., 2024) | |

| Regulation | CPIA policy and institutions for environmental sustainability rating (1 = low to 6 = high) | (Xia & Liu, 2024) |

3.2.3. Data Analysis

The data for this study were analysed using panel data regression. The study first conducted random and fixed-effect models. The model’s suitability was assessed using the Hausman test. Furthermore, the chosen model was evaluated for potential issues, including heteroscedasticity and autocorrelation. Given these issues, the final robust model considered was Generalised Least Squares (GLS), which addresses them by providing robust standard errors. The following are the equations: the first is the equation without any interaction effect, and the second contains the interaction effect.

![]() (1)

(1)

![]() (2)

(2)

In these equations;

FD = Fintech Development, GT = Green Technology, EC = Energy Consumption, GDP = GDP growth, R= Regulation, ‘u’ = error term, ‘i’ indicates cross section, β,0,1,2,3,4,5 are the coefficients and ‘t’ indicates time series

4. RESULTS AND DISCUSSION

4.1. Descriptive Statistics

Table 3 shows that green technology (number of patents) has a high mean of 733.24 and a very large standard deviation of 9,932.52, reflecting wide variations in patent levels across countries, with some showing very high levels of innovation while others account for very little. Regulation has a mean score of 3.166 and a relatively low standard deviation of 0.424, indicating moderate regulatory quality and very low variation across countries. GDP Growth has a mean of 3.171%, indicating modest average economic growth during the period, but a large standard deviation of 5.174%, indicating significant fluctuations, including both economic contractions and expansions. Energy Consumption has a mean of 2,358.4 kg and a high standard deviation of 2,412.34 kg, indicating substantial variation in renewable energy consumption across nations. Lastly, Fintech development has a mean score of 0.135 and a small standard deviation of 0.0219, suggesting relatively low but fairly consistent Fintech development across the sample.

Table 3. Descriptive statistics.

| Variable | Obs | Mean | Std. Dev. | Min | Max |

| Green Technology (number of patents) | 375 | 733.240 | 9932.524 | 0.11 | 189952 |

| Regulation (CPIA score) | 375 | 3.166 | 0.424 | 1.5 | 4 |

| GDP Growth (%) | 375 | 3.171 | 5.174 | -32.9 | 37.5 |

| Energy Consumption (kg) | 375 | 2358.4 | 2412.34 | 0 | 10832.9 |

| Fintech Development (score) | 375 | 0.135 | 0.0219 | 0.067 | 0.313 |

4.2. Correlation Analysis

Table 4 shows the correlation analysis of the variables. Green Technology shows extremely weak correlations with other variables, such as Fintech development (0.007), suggesting a minimal direct relationship between green innovation and Fintech development. Regulation also shows little correlation with Fintech development (r = 0.008), suggesting that regulatory quality may not have a significant independent effect on Fintech. GDP Growth is weakly positively related to Fintech development (0.047), and there is some indication that stronger economic performance is slightly linked to better Fintech performance. Energy Consumption is weakly negatively related to both Regulation (-0.116) and GDP Growth (-0.125), both of which are statistically significant, indicating that greater use of renewable energy is linked to reduced regulatory quality and slower economic growth in certain situations.

Table 4. Correlation analysis.

| – | Green Technology | Regulation | GDP Growth | Energy Consumption | Fintech Development |

| Green Technology | 1 | – | – | – | – |

| Regulation | -0.012 | 1 | – | – | – |

| GDP Growth | 0.014 | -0.067 | 1 | – | – |

| Energy Consumption | -0.045 | -0.116** | -0.125** | 1 | – |

| Fintech Development | 0.007 | 0.008 | 0.047 | -0.002 | 1 |

Note: ** indicates significance at 5% level

4.3. Panel Regression

Table 5 presents a panel data regression to evaluate the impact of green technology on Fintech development, with regulation as a moderating variable. Green Technology has a positive (B = 0.002) and significant (p = 0.000) impact on Fintech development, suggesting that green technology innovation is positively associated with higher Fintech development. It indicates a complementary relationship in which eco-innovation promotes digital financial advancement. Energy Consumption also has a positive, statistically significant impact (B = 0.008, p = 0.000), suggesting that increased energy consumption, possibly driven by digital infrastructure and industry activities, is associated with greater Fintech development.

Table 5. Panel regression.

| – | Random Effect Model | Fixed Effect Model | GLS | |||

| Fintech Development | Coefficient | P-Value | Coefficient | P-Value | Coefficient | P-Value |

| Green Technology | 0.001*** | 0.006 | 0.001*** | 0.003 | 0.002*** | 0.000 |

| Energy Consumption | 0.000 | 0.625 | 0.000 | 0.575 | 0.008*** | 0.000 |

| Regulation | -0.044*** | 0.000 | -0.043*** | 0.000 | 0.017*** | 0.001 |

| GDP Growth | 0.010 | 0.509 | 0.008 | 0.603 | 0.061*** | 0.001 |

| Reg X Fintech | 0.196*** | 0.000 | 0.190*** | 0.000 | 0.191*** | 0.000 |

| R-Squared | 0.7731 | – | 0.769 | – | – | – |

| Hausman | 3.03 | – | – | – | – | – |

| Heteroscedasticity | 109437.4 | – | – | – | – | – |

| Autocorrelation | 30.007 | – | – | – | – | – |

Note: *** indicates significance at 1%, ** indicates significance at 5%, * indicates significance at 10%

Regulation, interestingly, has a positive impact (B= 0.017, p = 0.001) in GLS, contrary to its negative influence in Random and Fixed Effects models. This implies that in controlling heteroscedasticity and autocorrelation, regulatory frameworks facilitate the growth of Fintech by instilling clarity and minimising market uncertainty. GDP Growth shows a positive and significant correlation (B = 0.061, p = 0.001), suggesting that economic growth underpins Fintech development. The interaction term RegXFintech is also positive (B = 0.191) and significant (p = 0.000), indicating that regulation complements the effect of Fintech development, perhaps by fostering a more stable and innovative financial environment.

5. DISCUSSION

The purpose of this study is to evaluate the impact of green technology on Fintech development, with regulations as a moderating factor. The findings of this study corroborate and extend earlier studies on the nexus between green technology and Fintech development. In line with the findings by (Li et al., 2024; and Xue et al., 2022), green technology illustrates a positive and significant relationship with Fintech development B = 0.002, p = 0.000), corroborating the hypothesis that eco-innovation drives digital financial progress. This connection is especially apt for Asian developing nations, where environmental concerns and digital transformation initiatives intersect with increasing calls for sustainable financial solutions. The complementary dynamics between green technology and Fintech indicate that environmentally motivated innovation can foster the development of new financial instruments, including carbon trading platforms and green investment tools.

In contrast to earlier research, which found either a direct negative effect or that regulation was not of prime importance (Hussain et al., 2024), the current study finds that regulation significantly and positively influences Fintech development (B = 0.017, p = 0.001). This result confirms Institutional Theory, which holds that regulatory clarity and institutional quality can foster innovation (Mertzanis, 2023). In Asian developing economies, efficient regulation can reduce investor uncertainty and promote innovation to advance Fintech solutions that are aligned with environmental protection. Additionally, the significant and positive interaction term (RegXFintech, B = 0.191, p = 0.000) supports the proposition that regulation enhances the impact of green technology on Fintech growth. This complementarity likely arises from growing government interest in spearheading sustainable finance as part of domestic digital and green agendas. Lastly, the substantial role of GDP growth and energy consumption demonstrates that overall economic growth and infrastructural development also favour Fintech growth, a trend found in fast-industrialising Asian economies.

Asian developing country policymakers should incentivise the adoption of green technology as a driver of Fintech growth, incorporating eco-innovation into national digital finance plans. Transparent and accommodating regulatory environments will be needed to lessen investor uncertainty and promote financially sustainable innovation. Governments ought to harmonise regulations with environmental and technological targets, promoting developments such as carbon trading exchanges and green financial instruments. Digital infrastructure investment and pro-GDP growth policies will further solidify Fintech expansion. By harmonising financial technology with environmental sustainability, policymakers can fuel inclusive, innovative, and sustainable economic development aligned with international sustainability goals.

CONCLUSION AND RECOMMENDATION

Building on the established influence of green technology on financial innovation, this study highlighted that regulatory frameworks significantly increase its effect on Fintech development, emphasising the importance of integrating supportive policies with sustainable technological initiatives. This research finds that green technology contributes substantively to Fintech development, particularly when supported by efficient regulations in Asia’s developing economies. Regulations not only directly contribute to Fintech development but also reinforce the role of green innovation towards digital finance.

POLICY RECOMMENDATION

Based on the empirical evidence, there are several significant policy implications for governments, regulators, and development agencies. Enhancing regulatory frameworks is the priority, with a focus on clear, transparent, and uniform policies that facilitate the innovation of Fintech and the adoption of green technologies. Regulatory consistency will minimise regulatory uncertainty, increase investor confidence, and provide an enabling environment of sustainable digital finance, and regulatory sandboxes can promote innovation without jeopardising financial stability. Governments, too, ought to proactively encourage eco-innovation in the financial sector by providing specific incentives, including tax incentives, subsidies, and special financing for Fintech companies that incorporate environmentally sustainable technologies, and by encouraging cooperation between providers of green technologies and financial innovators. Moreover, increased investment in digital infrastructure, such as broadband networks, data centres, cybersecurity, and renewable energy and energy-efficient technologies, is required to facilitate scalable and environmentally friendly Fintech ecosystems. Policy effectiveness can also be reinforced by strengthening institutional capacity, including regulatory expertise, inter-agency coordination, and regional cooperation among Asian economies. Lastly, it is important to promote sustainable financial behaviour and speed up the implementation of green Fintech solutions through public awareness and financial literacy campaigns.

LIMITATIONS AND FUTURE RESEARCH DIRECTION

This research is limited by its sample of Asian developing economies, which may limit the generalisability of its findings to other geographies with varying regulatory and technological landscapes. Moreover, reliance on quantitative data might miss subtle socio-political considerations affecting Fintech and green technology uptake. Qualitative research needs to be integrated in the future to yield deeper insights and examine the influence of institutional culture and stakeholder conduct. Regional and income comparisons may provide a wider insight into the green technology–Fintech intersection. Longitudinal analysis is also suggested to evaluate the dynamic influence of regulations and environmental innovations over time.

ETHICAL APPROVAL & INFORMED CONSENT

Not applicable.

AVAILABILITY OF DATA AND MATERIALS

The data will be made available on reasonable request by contacting the corresponding author.

FUNDING

None.

CONFLICT OF INTEREST

The author declares no conflicts of interest.

ACKNOWLEDGEMENTS

Declared none.

DECLARATION OF AI

During the preparation of this work, the author utilized ChatGPT to enhance the readability and improve grammar. Following the use of this tool the author carefully reviewed and revised the content as necessary and takes full responsibility for the final version of the publication.